manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

To understand the importance of the cautionary comments from award-winning attorney Marty Lavin to Mobile and Manufactured Home Living News (MHLivingNews), it is useful to understand some basics that influence all forms of conventional and manufactured homes. Access to lending plays an important role in all resale home valuations. The law of supply and demand, along with proper support by lending options, are important in determining the resale value of housing. “Credit is the lifeblood of housing,” said Eric Belsky, then with Harvard’s Joint Center for Housing Studies (JCHS). For instance, when conventional housing lending dried up in the 2008 housing-finance crisis, the value of conventional housing dropped sharply. The Washington Post said that conventional housing “Prices across the U.S., which fell 33 percent” during that housing-credit crisis.

When housing lending returned, and demand rose, conventional housing prices recovered. Today, because of high demand and favorable financing, record high prices are on the market. That should be good for manufactured homes. So why is that not carrying over as it should? That will be explored in the backdrop via linked reports.

A similar set of principles that applies to conventional housing applies to manufactured home lending and resale values too. Who says?

The Urban Institute and the FHFA both established the point that modern manufactured homes can and do appreciate. Beyond factors like proper maintenance, curb appeal, or the local economy, important factors like supply, demand, plus the quality and availability of lending options influences a given home’s resale value or potential selling price. These are hardly doubted elements of economics 101.

Some previous reports linked above and below shed light on these points.

Within that context, in an exclusive message to MHLivingNews, Lavin delivered a sharp shot across the bow of several key players in the manufactured housing profession. That in turn matters to manufactured home owners or those pondering the purchase of a manufactured home.

It is worthwhile to note that Lavin has often made pro-consumer comments to MHLivingNews and our professional sister publication. Lavin’s insights and commentary included decrying predatory tactics used in the manufactured home community sector. This is interesting because Lavin’s background includes manufactured home finance. He reportedly sold a manufactured home community he owned to the residents to become a resident owned community (ROC). Lavin has been more than an attorney – he has been a businessman who has often spoken out against bad business practices while advocating for pro-consumer stances. He himself says that he is for sustainable lending.

That noted, the subject Lavin addressed is the arguably scandal plagued Clayton Homes backed and Manufactured Housing Institute branded CrossModTM homes. Longtime readers here may recall that Modular Home Builders Association (MHBA) Executive Director Tom Hardiman called it a “deceptive” scheme. Hardiman called for MHI to end CrossModTM.

Clayton and MHI have instead pressed ahead. More recently, they have been joined by ManufacturedHomes.com in promoting this ‘politically’ problem-plagued program.

- Lending giant Fannie Mae (FNMA) has called their version of the CrossModTM homes finance program MHAdvantage®.

- Freddie Mac has called their version of CrossModTM homes financing program CHOICEhomes®.

- Manufactured Home Pro News (MHProNews) warned readers over 3 years ago that this program was a possible “Trojan Horse.” That caution, based on insider tips and keen professional insights, has increasingly been born out.

Lavin’s warning is the most recent. Here is what he said.

“I was working with FNMA [Fannie Mae] around 2007-8 when they offered the industry the “Select Home” program, featuring low rates for upscale placements, appearance, and constructed homes. I was very involved in this.”

The Appraisers Forum has a post that is dated October 30, 2007 which said that “In January ’08 (I believe) Fannie Mae will be rolling out a new program tentatively called the MH Select program.” Other sources broadly confirm Lavin’s stated facts too.

Lavin went on to say that “While the [manufactured home] industry had been busting for a low rate program, I knew they wanted low rates but not the various loan guidelines to make these home loans survivable. Virtually no loans were transacted. Wonder of wonders.” Other sources have likewise said that few loans were made under the MH Select land-home package mortgage option.

Lavin continued. “This new [CrossModTM homes/MHAdvantage®] program is [MH] Select Two. I am prepared to predict that the volume will be underwhelming. The industry will say loan underwriting and conditions are far too steep and the GSEs will say that the rates offered require stringent loan terms to protect themselves.”

Lavin, known for his dry wit and sarcasm, is more plainly saying that the CrossModTM homes/MHAdvantage® program – under whatever name – will not succeed. More on that thought shortly.

The GSEs is an acronym for Government Sponsored Enterprises (GSEs). GSE is a shorthand used to say Fannie Mae and Freddie Mac. As MHLivingNews previously reported, the GSEs – which are under conservatorship by the Federal Housing Finance Agency (FHFA) have been under fire for years for not providing the type of lending support that the Housing and Economic Recovery Act of 2008 (HERA) required. A report on that and how that impacts manufactured home owners and consumers is linked below

Lavin drew to a conclusion on his insights on CrossModTM homes/MHAdvantage® by saying the following.

“Bottom line: Loans the GSEs will transact will not work for the industry and loans the industry wants will be most unpalatable for the GSEs. Question; has anything changed in the last 20+ years?

Uh…”

Again, Lavin is known for sarcasm and dry humor. Lavin, though retired, is already correct.

The industry is down from where it was in new home sales 20 years ago. Financing is one of the reasons for the vexing reality, despite the growing affordable housing crisis. Duty to Serve (DTS) manufactured housing under the FHFA oversight of Fannie Mae and Freddie Mac was supposed to help address that concern. But over a dozen years after Congress passed DTS into law as part of the Housing and Economic Recovery Act (HERA) of 2008, it is still more mirage than reality.

Indeed, following a public pummeling by this author, our publication, the Manufactured Housing Association for Regulatory Reform (MHARR) and others – the Duty to Serve (DTS) program manager who departed the FHFA in 2020, Jim Gray, said this.

That is an understatement. MHI members have told MHProNews that they never saw any logic to the program. That warning from industry insiders to our publications, like the Trojan Horse warning, well before the program apparently failed. That warning came before Tim Williams, President and CEO of Berkshire Hathaway owned 21st Mortgage Corporation said he was glad that the DTS pilot program failed.

Additional Information, More MHLivingNews Analysis and Commentary

With all due respect to any white hat independents that may have to some degree bought into this purported charade called CrossModTM, it is arguably one more tactic by manufactured housing’s corrupting powers that be. Williams’ own statement – linked above – should make it clear to objective thinkers that Clayton/21st/Vanderbilt Mortgage and Finance (VMF) had no desire to provide lower cost lending options to the manufactured home industry. Doug Ryan at CFED-turned Prosperity Now made that argument to American Banker.

CrossModTM homes/MHAdvantage®, CHOICEHomes®, the “new class of manufactured homes” or any other name or term has been or will be used to promote this flawed-from-its-inception plan should be avoided or rejected. Why?

Warren Buffett said it himself. You cannot make a good deal with a bad person.

It is important to note that MHLivingNews has and remains pro-manufactured homes, but pro-ethical business practices. For that reason, we have spotlighted good practices, but denounced those that appear to be problematic, predatory, or possibly illegal.

We have, among other education/information services, done in depth videos and reports on how to shop for a manufactured home, and how to spot possible problems before a purchase is made.

MHLivingNews and our sister site get a steady set of contacts from those who have seen this report below.

A common question is, how can I sue them? Or a caller may ask in their own words, how can I join a class action suit against Clayton Homes and/or one of their affiliated lending units?

Part of the problem hobbling manufactured housing has long been proper financing. While Lavin is correct that lending must be sustainable, Doug Ryan then with the CFED nonprofit which has since been renamed Prosperity Now said this to American Banker.

“For too long we have ignored a segment of our housing system that offers an affordable path to homeownership: manufactured housing.

A manufactured home is the only option for many low-income families to own a piece of the American dream. But those families often have limited access to competitive loan-pricing that is available to more conventional home buyers, thanks in part to low participation by Fannie Mae and Freddie Mac in the manufactured housing market.”

Ryan also said: “That means borrowers of manufactured home loans often must turn to an uncompetitive market, dominated by Clayton Homes, which does not have to rely on the secondary market for capital.”

Ryan and Lavin express themselves entirely differently. But a common point is that there is a desire for more competitive interest rate lending.

Triad Financial Services, now part of publicly traded ECN, has a program for lower rate loans. It has been praised by lenders who participate in that plan.

The case has been made years ago that lower rate lending in manufactured housing is proven to be sustainable. It is not only by Triad, but also from the research report linked below.

It is with a measure of sorrow that MHProNews recently did a deeper dive into supposedly pro-industry bloggers and media, including but not limited to ManufacturedHomes.com, that have arguably failed to blow the whistle on what is undermining manufactured home owners valuations while harming manufactured housing industry independents.

Lavin, some years back, joined MHLivingNews and MHProNews and others in pushing for more and better access to financing. A redux on that is linked below.

Among those who have saddled up with MHI connected brands is apparently ManufacturedHomes.com. They have in the past made claims that MHProNews fact checked. Brad Nelms, nor others with ManufacturedHomes.com attempted to rebut any of those allegations.

It is with that backdrop of cautionary notes that MHLivingNews shows this next video. It is NOT to endorse either CrossModTM homes, MHAdvantage®, CHOICEHomes®, or anything like it. Quite the opposite is true – this is a warning. Nice video, but arguably a problematic pitch for reasons elaborated on in this report.

It was an MHI member manager who told MHProNews that the entire CrossModTM was flawed at the outset. Many manufactured home builders can produce a modular home as well as a HUD Code manufactured home. The homes can look and live much the same. The photos below are all of manufactured homes, long before CrossModTM became a Clayton and MHI backed thing.

It is an advantage to have entry level manufactured homes, as well as more upscale ones. There is NO NEED to go to a CrossModTM homes, MHAdvantage®, CHOICEHomes®, etc.

As MHLivingNews previously reported, ground sets or other items featured touted for CrossModTM homes have long been available in mainstream manufactured homes.

As MHProNews has reported, and Clayton Homes has never publicly denied to our digital publications, the earlier iteration of more costly manufactured homes Clayton tested did not sell well. That too fits with what Lavin said above.

The Case for a Consumer Alert…

As a consumer alert, the bottom lines are as follows. Mainstream HUD Code manufactured homes by law have qualities, safety features, and consumer protections not found in often far more costly conventional housing. MHLivingNews has made that point using evidence and comparison for years.

The case has been made, and stands publicly unchallenged at this point, that for their own motivations, Warren Buffett led Berkshire Hathaway, their related brands in manufactured housing, plus several billionaires have arguably weaponized large portions of the American Dream.

No less a figure than Robert F. Kennedy Jr. (RFK Jr.) and the nonprofit publication he leads, The Defender, has been making a similar argument about Bill Gates. With Gates and Buffett so interlaced in the Gates Foundation and other investments, it is fair to say where one is, the other is likely involved too.

Gates, as a report linked further above and others have demonstrated, is closely allied with Buffett.

RFK Jr. is the son of the late, popular assassinated Senator Robert F. “Bobby” Kennedy.’ He is also the nephew of the assassinated President John F. “Jack” Kennedy. RJK Jr. is a consumer advocate, a successful attorney in fighting for the rights of the common man against big corporate polluters. He is involved in children’s causes too.

The case can be made that modern manufactured homes are the most proven form of permeant affordable housing in America today. Millionaires and even billionaires own a mainstream manufactured home. CrossModTM homes, MHAdvantage®, CHOICEHomes®, etc. has too many red-flags. There are too many prudent people in or out of our industry, as some of the links above and below reflect, that make it clear that this program does far more harm than good.

Caveat emptor. Let the buyer beware. And while good companies may well offer this option, the intelligent thing to do is this. When you can get a similar home for less money and they look and live the same, why pay the significantly higher price? Even if the system has arguably been wrongfully rigged to favor CrossModTM homes, an MHI member producer told MHProNews this. By the time you factor in the higher costs, there is no effective savings.

MHLivingNews urges caution against those who have direct ties to MHI. It is not without reason that Doug Ryan, Marty Lavin, Mark Weiss, Danny Ghorbani, and a range of others in and out of MHI have urged caution against trusting them. ManufacturedHomes.com struck a deal with MHI’s prior general counsel. Why? Why is ManufacturedHomes.com – which as a disclosure we used to work with in days gone by – is pushing a loan program and housing product that arguably works against the interest of consumers and white hat independents, that is a cautionary flag.

When they or any other trade publication or blogger is cozying up to MHI, that should be a warning flag. They may have pretty videos. But as two year over year declines in new manufactured home sales during an affordable housing crisis has demonstrated, pretty videos, 3D tech, or sharp websites alone are not going to restore the manufactured home market to its potential.

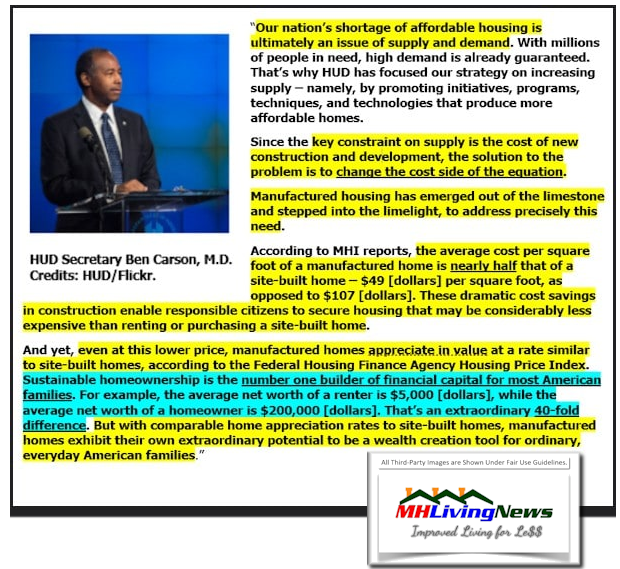

Whatever someone’s politics, those statements by former HUD Secretary Ben Carson are demonstrably true. That potential matters to savvy manufactured homeowners. Because as was noted at the top, it is economics 101. Supply, demand, and appropriate financing are among the reasons that more manufactured home resales are not occurring at higher prices.

Buffett is right about some things, including the fact that the rearview mirror is clearer than the windshield. Based on the evidence, based on the history, the prudent home seeker should think twice before doing business with certain brands that have a history of attracting negative media for years.

If you do decide to buy a Clayton or get financing from a Berkshire owned lender like 21st Mortgage Corporation or Vanderbilt Mortgage and Finance (VMF), why not consider buying it from an independent retailer that has a good reputation for service after the sale? But in our expert view, look for other options whenever you can. We disagree with Doug Ryan on several things, but Ryan had an interesting point “The system currently discourages Fannie and Freddie from investing in manufactured housing.” It is a tangled web. But Ryan said it: “firms such as Clayton Homes, which dominates the market for building, marketing and financing of manufactured homes. The company has no need for Fannie and Freddie since it accesses the capital markets through its parent Berkshire Hathaway.”

It does not have to be this way. Exposing the problems are how the solutions can be implemented.

Ryan’s headline summed it up it is “Time to End the Monopoly Over Manufactured Housing.” Once the lightbulb went off, that is a theme that MHLivingNews and our sister site have advocated now for several years.

Our advice? Until the legal system fixes this mess, avoid the monopolists whenever you can.

That’s a wrap on this installment of “News through the lens of affordable housing and manufactured homes” where “We Provide, You Decide.” © ## (Affordable housing, manufactured homes, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.) (See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHLivingNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com. This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Recent and Related Reports:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.