manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

The following are the comments as prepared for the Federal Housing Finance Agency (FHFA) virtual listening session scheduled for Wednesday 12.11.2019.

—

FHFA Listening Session Comments by L. A. ‘Tony’ Kovach, Publisher of MHLivingNews.com, MHProNews.com, Award-Winning Manufactured Home Industry Expert and Consultant (LATonyKovach.com and http://www.linkedin.com/in/latonykovach)

Speakers addressed the Washington, D.C. Federal Housing Finance Agency (FHFA) Duty to Serve (DTS) listening sessions on December 2, 2019. DTS mandates the Government Sponsored Enterprises (GSEs) of Fannie Mae and Freddie Mac support affordable housing.

Those speakers could be broken into 3 broad groups.

- Those praising FHFA and the GSEs for a ‘transparent process’ and ‘progress’ being made.

- Those that were polite toward FHFA, Fannie and Freddie, but clearly stated that more needed to be done to make DTS a reality.

- Those who were blunt or caustic that asserted DTS wasn’t working. Instead, the law had been perverted to benefit the more well-to-do instead of those of lesser means.

I know this because I was among those invited to present. I listened to some 40 people sound off, plus FHFA and GSE officials.

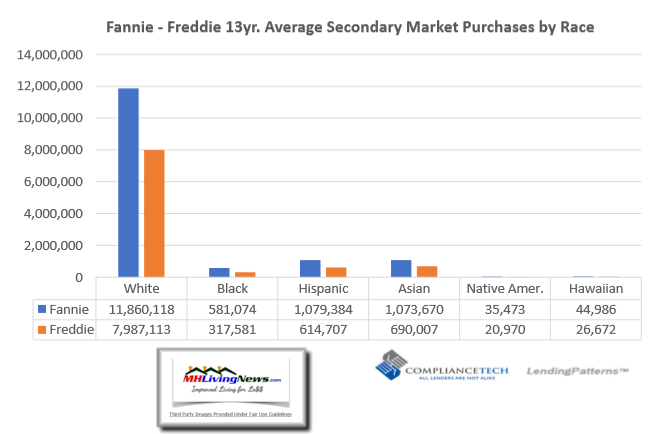

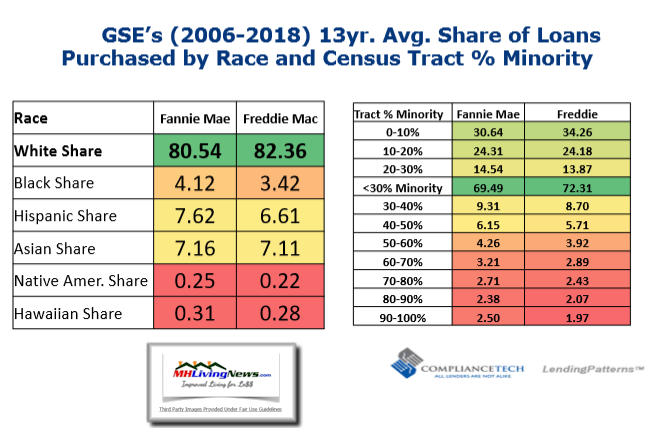

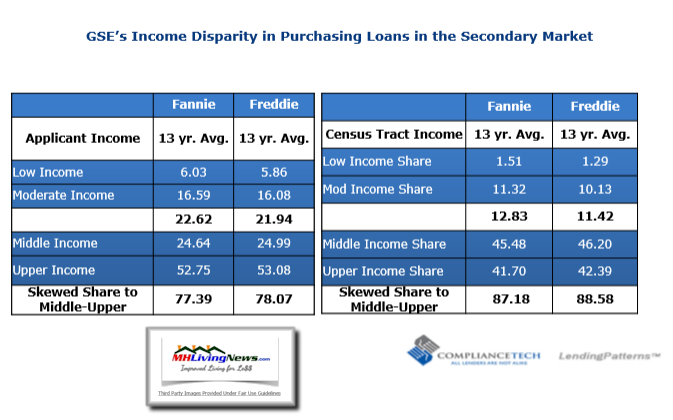

For example, there were black nonprofit and businesses leaders. They pointed out the wide disparity of lending reaching minorities vs. whites in mortgages purchased for the secondary market by Fannie and Freddie. Data shown was provided by Maurice Jourdain-Earl of ComplianceTech, based on HMDA data.

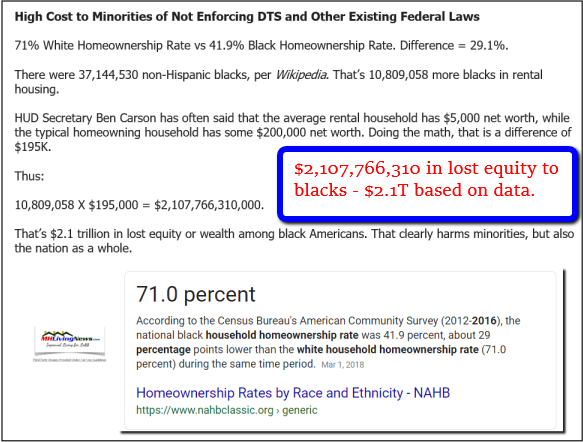

NAREB said “The homeownership rate for black households ended 2016 at 41.7 percent.” They’ve made the point that discrimination is being tolerated by FHFA.

Doing the math, the economic harm to blacks may be imputed to exceed a staggering $2.1 trillion dollars.

Several manufactured home community residents from different states said commercial real estate loans made under DTS to community operators who purchased or refinanced communities at low rates. Because of a lack of resident safeguards, they named companies like Havenpark Capital and RV Horizons/Impact Communities – both of which are Manufactured Housing Institute (MHI) members – that aggressively raised site fees (lot rents). Economic evictions had or will occur, those residents said.

DTS had been perverted, diverted and turned on its head.

A program designed to provide more affordable housing for lower income Americans was instead fueling less affordable housing by making loans to wealthy consolidators and others.

David Dworkin spent 11 years at Fannie Mae, nearly 10 years at the U.S. Treasury, and for almost 2 years has been the President and CEO of the National Housing Conference. Dworkin’s recent comments letter to FHFA said: “Manufactured housing is critical to ensuring access to affordable housing for both rural and underserved urban communities. Challenges in achieving what were arguably modest goals should prompt redoubled efforts rather than changes in goals targets. We have full confidence in both Enterprises ability to reach the existing benchmarks.”

Dworkin knows the system from the inside. But there’s more.

The Duty to Serve (DTS) Rural, Underserved, and Manufactured Housing Markets was enacted as part of the Housing and Economic Recovery Act (HERA) of 2008. The law passed by a widely bipartisan margin.

FHFA’s website says: “The Duty to Serve (DTS) requires Fannie Mae and Freddie Mac (Enterprises) to facilitate a secondary market for mortgages on housing for very low-, low-, and moderate-income families in: Manufactured housing, Affordable housing preservation, and Rural housing.”

Over a decade later, little to no discernible support for the vast majority of HUD Code manufactured homeowners, those seeking affordable housing, retailers and others selling manufactured homes exists.

Data supplied by the GSEs prove that point.

As a trade journalist who publishes the runaway largest and most-read professional media in our industry with a companion public site and as someone who is a multiple award-winner in history and manufactured housing, those opening facts beg several questions.

But let’s pivot to statements instead.

- No person or organization is supposed to be above the law.

- We’ve spoken with lenders that entered the manufactured home market after DTS passed. They’re successfully making sustainable loans.

- We’ve spoken with lenders who’ve made manufactured home loans – including personal property or ‘chattel loans’ – sustainably for a decade or more.

- Given federal law and that others made such loans successfully, why has FHFA tolerated obvious foot-dragging by Fannie and Freddie to fully enforce and comply with federal law?

Years of research and reports could be boiled down to this claim.

Good federal laws are on the books that support manufactured housing on paper but are going under-enforced, are ignored and/or perverted. DTS is among them.

A decade after HERA and DTS passed, where is that secondary financing market for manufactured homes?

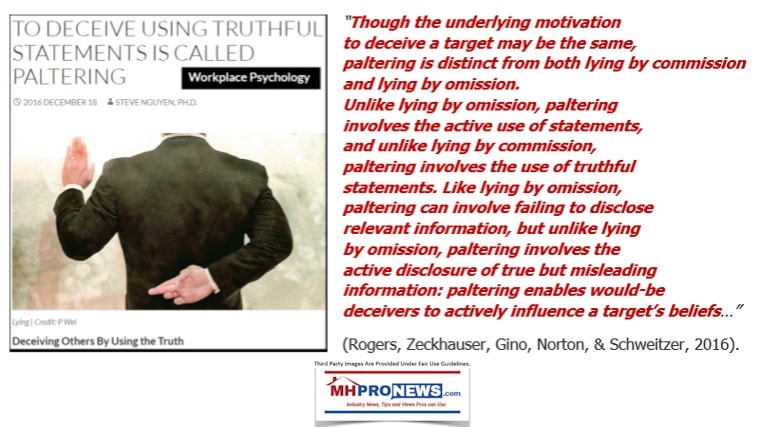

Interested parties should read various letters submitted to FHFA about the current plans and proposed modifications requested by the Enterprises. The MHI letter by EVP and CEO-elect Lesli Gooch makes some interesting and accurate statements, but pivots to items that are arguably paltering.

Instead of Gooch making a case for robust support for all HUD Code manufactured homes – which is what one might reasonably expect of the trade association claiming to represent all segments of manufactured housing – instead MHI promoted their so-called ‘new class of homes’ recently dubbed “CrossModTM homes.”

Why didn’t MHI pursue robust lending for all manufactured homes, instead for only select “CrossModTM homes” backed by Clayton Homes, Skyline-Champion, Cavco Industries and some MHI member producers?

How did Fannie and Freddie magically establish a special program with specs for those so-called “CrossModTM homes,” reportedly developed in closed doors meetings with MHI?

Why haven’t the minutes for secretive meetings between the GSEs and MHI been released?

MHI member-producers told MHLivingNews that there’s long been lending on modular housing on par with conventional housing.

It was illogical and insulting, said those sources, to create a so-called new class of manufactured housing when those same factories already built modular-coded units.

We have no problem with what products builders produce that comply with regulations. But we do have a problem with special lending extended to favored MHI firms by the GSEs with the FHFA’s consent.

HUD Code builders have always had the ability to build manufactured homes to minimum federal construction, energy and safety standards providing durable, safe housing with consumer protections. Those entry-level homes are affordable for people with lower incomes. Builders can also offer more residential style-homes with more features at a higher cost.

There was therefore no logical reason to create a new class blurring lines between modular and HUD Code, including via the name of the product.

I’ve personally spoken with people at the GSEs and/or who performed contract work for the Enterprises. Some said the Freddie Mac Choice and MH Advantage by Fannie Mae plans are not how such lending programs are traditionally developed.

Of course not.

Do the GSEs tell site builders how to build their housing units?

Richard Genz did research for the Fannie Mae Foundation published some 2 decades ago. He made the case that manufactured homes were unfairly stigmatized.

So why implement a scheme splitting higher cost ‘new class’ HUD Code homes MHI and the GSEs are pushing? Doesn’t that de facto stigmatize anew the millions of existing manufactured homes?

This ploy purportedly fuels stigma, arguably benefiting lenders like 21st Mortgage or Vanderbilt Mortgage and Finance, owned by Berkshire Hathaway that along with Clayton Homes have been credibly accused of predatory and racist behavior.

MHI and the GSEs vaguely admit that ‘CrossModTM homes’ are off to a poor start. Only some 10 total loans made in 2018 and 2019, per a statement at the St. Louis FHFA listening session. New HUD Code production is also down year-over-year. Coincidence?

Given that FHFA as well as the NAR both reported in 2018 manufactured homes appreciate, the lack of logic for plans developed by MHI, Fannie and Freddie behind closed doors is stunning.

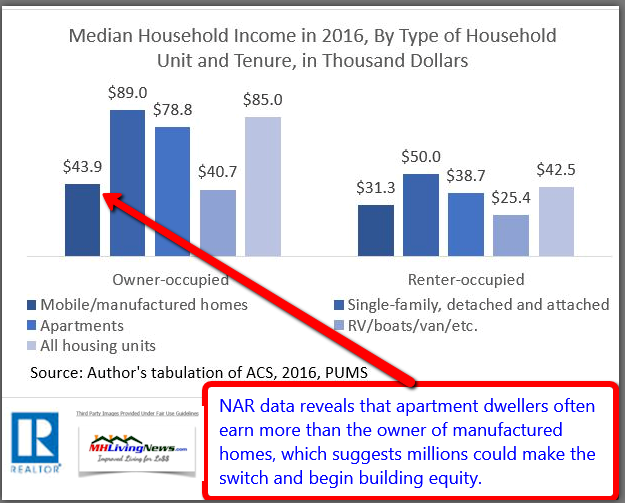

Rephrased, the status quo unduly punishes millions who currently own a manufactured home. They could enjoy higher equity and resale values if DTS were fully enforced. It’s also punishing renters who could pay less monthly to own a manufactured home, per the NAR.

That’s tens of billions of collectively lost wealth for current and potential manufactured homeowners. When more people of all backgrounds realize that, there are voters among those 22 million Americans in manufactured homes and 111 million U.S. renters.

We’ve published an online version of this comments letter on Manufactured Home Living News (MHLivingNews.com). It includes illustrations, videos, links to comments, plus historic information.

We believe evidence and reason suggest that one or more at FHFA actively or tacitly allowed the law to be twisted in a manner benefiting a few at high cost to millions.

That implies incompetence, collusion, conflicts of interest and/or corruption.

Therefore, the FHFA has no legal or logical choice but to reject currently promoted plans and call upon Fannie and Freddie to immediately follow the DTS law, no matter whose deep pockets that may upset.

The appropriate oversight parties at FHFA and Congress should independently investigate how a decade after DTS became law that it’s still thwarted from providing affordable lending to potentially millions during an affordable housing crisis.

The status quo is a scandalous disgrace.

“There is nothing wrong with America that cannot be cured with what is right in America.” So said former President William J. ‘Bill’ Clinton, who signed the widely bipartisan Manufactured Housing Improvement Act (MHIA) of 2000 into law.

This isn’t a partisan issue, its an issue of right and wrong, and people of good will must do all that is necessary to expose the treachery harming tens of millions of Americans, independent businesses, while enriching a few consolidators and their cronies in government.

Thank you.

L. A. ‘Tony’ Kovach

Managing Member

Lifestyle Factory Homes, LLC

Parent Company to DBAs MHProNews.com, MHLivingNews.com, LATonyKovach.com, MHC-MD.com et al.

## End of 12.11.2019 Virtual Listening Session Comments as Prepared ##

A shorter version of the talk above was delivered in Washington D.C. to a mix of shock and applause. Following the address, Tony Kovach contacted officials at the FHFA, Fannie and Freddie involved with DTS, plus key MHI, Clayton Homes, and 21st Mortgage and Finance officials, inviting them to publicly discuss, defend, explain or debate the concerns raised. The invitation was confirmed, but there were no takers.

That Washington, D.C. version of Tony’s address, along with a step-by-step plan for exposing the purported corruption harmfully impacting manufactured housing are among the items linked below under the ‘related reports’ after the byline and notices. There’s work to be done to fix what’s wrong. But that doesn’t take away from the strong evidence that manufactured homes are good, even though there are so-called black hat operations within the industry that have sadly given the industry overall a black eye. That’s why we believe that one must separate the wheat – the good – from the chaff – what’s problematic.

We’ve said for years, nothing is changed until it is challenged.

To learn more, see the related reports below. “We Provide, You Decide.” © ## (Lifestyle news, commentary, fact-checks and analysis. Note that any third party images, citations or other content are provided under fair use guidelines for media.

Soheyla Kovach is the co-founder of MHLivingNews, (pronounced like Co-Vatch like a watch with a V) and is a managing member of LifeStyle Factory Homes, LLC – the parent company to this platform, MHProNews and other manufactured housing related ‘white hat’ professional services.

Soheyla Kovach is the co-founder of MHLivingNews, (pronounced like Co-Vatch like a watch with a V) and is a managing member of LifeStyle Factory Homes, LLC – the parent company to this platform, MHProNews and other manufactured housing related ‘white hat’ professional services.

Related Reports:

Clicking on text-image graphics will take you to that report.

{kind=link}