manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

The path to home ownership lay before him, smooth and attainable as never before. All Eric Powell had to do was secure a small loan. He had a steady job, a decent credit score and a wife who happened to work for a bank: What could possibly go wrong?

By Jan Hollingsworth

for MHLivingNews.com

Christmas came a week early for the Powells last December, when the Louisiana family moved into a cozy manufactured home in West Monroe.

After 10 years of marriage, most of it spent in apartment complexes, Eric Powell finally had the opportunity to give his three young sons – ages 3, 7 and 8 — the rural childhood he cherished, and the future he’d always envisioned for his family.

“I would love for my wife and I to live the upper range of the middle income, and see my kids accomplish whatever they want to do,” says the soft-spoken sales rep who grew up in bayou country, 90 minutes east of Shreveport.

Set on seven wooded acres that have been in Eric’s family for more than half a century, the 16×80 single section manufactured home built in 1996, is a dwelling as modest as his dreams – three bedrooms, a porch, a pond and plenty of room for three active boys to roam.

Best of all, it represented a sturdy foundation upon which to build a new life, where the family could put down roots in generations of Powell soil.

They hadn’t counted on slamming head-first into the reality of good intentions gone awry.

To Protect and Serve

Five years ago, the nation began to emerge from the greatest economic crisis since The Great Depression.

Congress passed a law meant to avoid a repeat of the 2008 financial services meltdown that cost countless Americans their homes, their livelihoods, their savings and – in some extreme cases – their lives.

The Dodd-Frank Wall Street Reform and Consumer Protection Act was a sweeping 2000-page collection of rules aimed at addressing the subprime mortgage crisis that was created by lowered lending standards and higher-risk mortgage products — loans that were handed out like party favors, then bundled and traded on Wall Street, while housing prices bubbled and finally burst.

For the most part, manufactured housing sat on the sidelines, having learned some hard lessons from the industry’s own implosion some years before.

Dodd-Frank and the lending issues it was supposed to address had nothing to do with factory-built homes – until it became apparent that it did.

Former Congressman Barney Frank, who co-sponsored the legislation, said he was “regretful to realize” its negative impact not long after Dodd-Frank became the law of the land.

In a 2011 letter to a constituent, Frank wrote:

“I do not think it is necessary to include manufactured housing as part of our effort to prevent abusive mortgage practices, and I am now working with my staff to see if we can find a way to make a change that would deal with the problem you correctly point out… “

Yet, it would not have taken an act of Congress to address the issues that effectively blocked the route to affordable housing for many low- and moderate-income consumers.

The Dodd-Frank Act had created a new federal agency – the Consumer Finance Protection Bureau (CFPB) – and imbued it with unprecedented powers to set rules and regulations governing residential loans.

The CFPB’s stated mandate, implicit in its name, was to ensure that financial products and services “work for consumers.”

They surely did not work for Eric Powell and thousands of prospective buyers and sellers who discovered that the post Dodd-Frank world offered few options for financing a manufactured home priced under $20,000.

But Eric didn’t know that, so down the rabbit hole he went.

A Simple Plan

The house belonged to Eric’s father, who was in the midst of laying his own foundation for retirement on 11 acres in nearby Farmerville. The elder Powell had his eye on a newer 2013 manufactured home.

Eric was delighted when his dad offered to sell him the older one for $7500, which his father would then use as a down payment on his Farmerville retirement home.

The path to home ownership lay before him, smooth and attainable as never before. All Eric had to do was secure a small loan. He had a steady job, a decent credit score and a wife who happened to work for a bank: What could possibly go wrong?

Two Options

The Powells may have qualified for a regular mortgage to finance the purchase of their factory-built home. But that would have meant putting up as collateral the land that had been in Eric’s family for four generations.

He wasn’t about to encumber his grandpa’s seven hard-earned acres — the one thing the family truly owned — to secure a simple $7500 loan.

So, like two out of three consumers looking to finance a comparable factory-built home, Eric wanted a personal property loan — the same as a car or a boat or an RV.

The interest rate for these so-called “chattel” (home-only) loans is considerably higher than a regular mortgage, but they anchor the manufactured housing market.

Many manufactured homes are in land-lease communities, where the buyer doesn’t own the land — thus a standard mortgage isn’t an option for them.

Others, like Eric, own a few rural acres that they’d just as soon keep free and clear title to.

So he sent an online query to Lending Tree, a network of banks, credit unions and other lenders who compete for all kinds of financial business.

Eric was pleased when his email inbox was flooded with “pre-qualified” offers — until he discovered that the sum he wished to borrow was too small for the curious circumstances of the post-Dodd-Frank world of finance.

Eric was pleased when his email inbox was flooded with “pre-qualified” offers — until he discovered that the sum he wished to borrow was too small for the curious circumstances of the post-Dodd-Frank world of finance.

Unintended Consequences

Under Dodd-Frank, the CFPB created a new “residential mortgage loan” definition that covers all consumer loans secured by a dwelling.

This unleashed a cascade of new regulations that have little to do with manufactured homes, yet resulted in a profound impact on people seeking to finance one — most notably the chattel loans nearly 70 percent of borrowers rely on.

Community banks, regional credit unions and other lenders that once helped low- to moderate-income families buy affordable manufactured housing began to leave the market.

U.S. Bank was one of the larger players to fold its tent, citing the high cost of making these loans under the new Dodd-Frank rules — rules that Barney Frank, the co-architect of the law, said were never meant to be applied to manufactured homes.

Ironically, CFPB – the federal agency that made the rules — and the various consumer advocates whose mission it is to protect the very people who can no longer buy or sell their homes under Dodd-Frank, have turned a deaf ear to the industry’s call for reforms.

“It’s been a three-year battle with CFPB, because they have the discretion to change things. It’s been very discouraging, because they have a certain mindset,” says Dick Ernst, a consultant with four decades in manufactured housing finance.

That mindset appears to be centered on the traditional mortgage model for single family homes — a model that spawned the unfettered lending orgy that led to the crisis Dodd-Frank was meant to fix, and which now boasts ultra-low interest rates propped up by federal supports.

“The consumer groups are so focused on the interest rate, itself, that they don’t think how interest rates are determined,” says Ernst.

The manufactured housing chattel market enjoys no comparable assistance in the form of a rate structure established by the federal government, he says.

Single sectional manufactured homes like the one above weigh about 30 tons.

Photo credit: Welcome Home Ohio.

There are no Fannies or Freddies or FHA to ensure a secondary market, where the loans can be sold instead of carried on the lender’s books for years or decades.

There is the high cost of compliance and servicing a loan that requires frequent letters and phone calls to keep payments on track, and the risks inherent in making loans to families who may be one paycheck away from default — all of which sets manufactured housing finance a world apart from traditional home mortgages, Ernst says.

The very largest chattel lender probably does no more than 10,000 to 12,000 loans per year, compared to the far greater numbers of traditional mortgages originated by the Wells Fargos and Chases, he added.

“Those banks are spreading the costs of compliance — audits and other expenses — out over hundreds of thousands of loans.”

That drives up the cost per loan in manufactured housing considerably, he says.

But the rules under Dodd-Frank don’t recognize these realities, and it not only hurts the industry — which can’t sell homes it can’t get financing for, says Ernst.

“At the same time, it’s cutting off a route to home ownership for low- to moderate-income families around the nation — especially in rural areas.”

The U.S. Census Bureau indicates that a modern manufactured home can be half the price or less of a comparable conventional house, thus the growing appeal.

The Corporation for Enterprise Development (CFED), a non-profit consumer-oriented think tank, is one of the supporters of manufactured housing, yet is one of the biggest opponents of industry efforts to tweak what Barney Frank acknowledged were the unintended consequences of Dodd-Frank.

“We think the homes themselves are a really good option for home ownership, but we disagree with (the industry’s) financing model,” says Doug Ryan, the organization’s director of affordable home ownership.

“Why would you want to buy a home at a 13 percent interest rate?” he wonders.

Eric Powell gladly would. That’s almost three times cheaper than the loan he ultimately was forced to secure, rather than give up his fight to own a home.

No Magic Wand

Eric’s father “was quite disheartened” to find that his son’s inbox full of “pre-qualified offers” through Lending Tree had turned into a vast rejection file.

When Eric put in an application to follow up on each offer, company after company declined to make the loan — not because of his credit worthiness, but because the amount he wanted to borrow was too small — even when he applied for an extra $2000 to clean up and consolidate some other bills.

What the rejection letters did not explain was that industry lenders estimate it costs roughly $3000 in points and fees to originate a chattel loan, regardless of the size of the loan.

Under the rules the CFPB had created, lenders could not charge Eric more than $760 — or 8 percent of the amount borrowed — without the loan being labeled “high-cost,” a polite euphemism for a predatory loan.

“It’s like waving a red flag in front of customers,” says Ernst. “And it triggers all kinds of things, like HUD-approved counseling and myriad expenses that someone has to eat before or if the loan closes.”

Nor does Dodd-Frank take into account the fees that chattel lenders do not charge — private mortgage insurance, underwriting fees, application fees and any number of add-ons that regular mortgage lenders can and do charge.

“We don’t, because we know our customers can’t afford that,” he says.

Thus, the Powell family’s simple plan was more complicated than any of them imagined.

Eric saw his dream of home ownership begin to slip away, along with his father’s down payment for his own retirement home.

When Eric discussed it with his dad, “He said, ultimately, I had two options: ‘You will have to rent an apartment and I’ll use the house as a trade-in, or I’ll wait for a buyer who can pay cash.'”

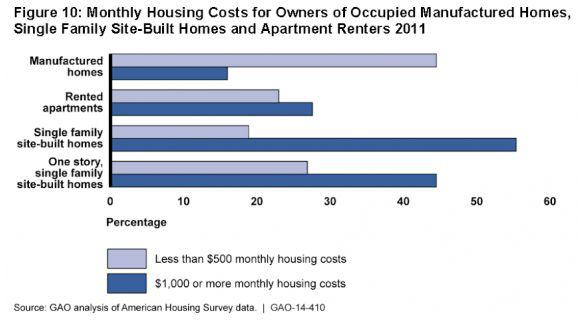

A 2014 GAO report which included this graphic demonstrates that even with higher interest rates,

the monthly costs of a manufactured home are more affordable than other housing options.

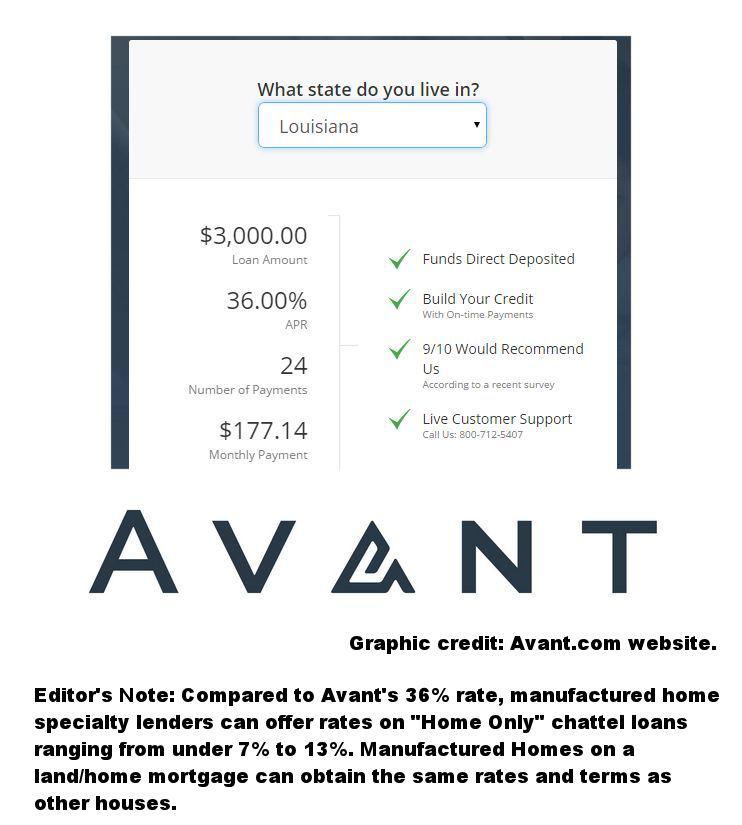

The Powells swallowed hard and went back to the Lending Tree, this time looking for an unsecured personal loan for $9500, which Avant was happy to provide at 35.91 percent interest.

In less than 72 hours, it was a done deal.

Consumer Protection?

Ernst is beginning to wonder if these kinds of consequences are really unintended.

“I was part of a group of four or five people who sat down with CFPB to try to educate them on the differences in manufactured housing finance,” he says. “They don’t want to hear any justification for it, whether logical or not. It doesn’t fit their narrative.”

Barry Noffsinger, a regional manager for CU Factory-Built Lending, was among the lenders who met with both the federal agency and consumer advocates to explain the intricacies of manufactured housing finance.

His company, a division of Texas-based San Antonio Credit Union, is one of three national lenders who still make chattel loans under $20,000, as well as regular mortgage loans for manufactured homes.

Noffsinger says he doesn’t really have a dog in this fight. His company makes tightly underwritten loans to people with good credit and a down payment.

As a non-profit that serves its members, the credit union is able to offer loans with interest rates and origination costs well below the current high-cost triggers of Dodd-Frank.

“Our basic market is trying to find people of modest means who will actually pay us back,” he says.

San Antonio’s mission as a credit union is not-for-profit, says Noffsinger. “But we also have to be sustainable. You just can’t make loans if you can’t make money.”

Irresistible Forces and Immovable Objects

The other two national lenders — 21st Mortgage Corporation and Vanderbilt Mortgage and Finance, Inc. (VMF) — became part of billionaire Warren Buffett’s Berkshire Hathaway 2003 entry into manufactured housing. VMF and 21st are the undisputed industry leaders.

“They’ve made a niche market in lending to customers that have less than 650 FICO scores,” says Ernst. “A fair amount of their business is people who have had a hiccup in life.”

Some in the industry may not like the fact that one or two companies have a huge market share, but they are loaning money to people no one else will — and that helps both consumers and the industry, says Ernst.

“Under Dodd-Frank we have one lender who has declined to make any loan under $20,000,” Ernst says.

CFED’s Ryan doesn’t buy it. “If they can prove that they’re unable to make these loans, they should show that.”

Ernst has written an article deconstructing the costs involved in originating a chattel loan under Dodd-Frank and has met with Ryan to explain it in detail.

“Does it make any sense that we want to charge higher rates?” he says, noting that the industry “would sell a whole lot more” manufactured homes if the loans were cheaper.

“I get his argument and he’s given me numbers,” Ryan says of Ernst. “I’m not convinced by his figures, but he knows more about this stuff.”

Ryan suggests that chattel lenders like 21st Mortgage and Vanderbilt — part of a Berkshire Hathaway/Clayton Homes conglomerate that manufactures, retails and finances manufactured homes — are little more than loan sharks masquerading as home builders.

“They make their money on selling loans, not on repayment,” says Ryan, citing the high rate of defaults. “That’s why it’s so awful, when you allow $3000 in fees on a $10,000 loan.”

“It makes all kinds of sense that when you serve that (high-risk) marketplace, you’re going to have more defaults,” says Ernst.

And when homeowners can’t sell their homes to prospective buyers who can’t find financing, you’re going to have even more, he added.

Defaults lead to repossession, which is another costly aspect of the chattel business.

Unlike a car or a boat or RV, where repossession is as simple as driving the vehicle back to the lot, modern manufactured homes are not the trailers of old and are decidedly not mobile.

In fact, a mobile home hasn’t been built in the United States since June 15, 1976, when these kinds of factory-built homes became subject to the federal HUD building code for manufactured housing.

Today’s manufactured homes are meant to stay where they are sited for the home buyer, with various foundation systems, such as stem walls, anchors and concrete or steel supports plus possible add-ons like garages, porches and decks.

Multi-sectional manufactured homes can weigh 70+ tons, multi-level homes like the

home shown above, even more. Photo credit Wyngate Farms, Kalamazoo, MI.

The logistics and expense of repossessing a 30- to 70-ton structure is not something lenders say they are anxious to do and is another cost that has kept the pool of options for consumers very shallow.

Industry insiders suggest that if there was so much money to be made from chattel loans under the current regulations, lenders would be lining up to make them.

“If they’re portfolioing a risky loan, they’ve got to be able to make money. That’s basic economics,” says Noffsinger. “Is it wildly profitable? That’s debatable.”

There are real world consequences to these policies, says Ernst. “And whether it’s unwillingness to open their eyes and see the truth, or being overzealous of their position irrespective of reality — either way it’s hurting people.”

Living in the Real World

When the CFPB refused to use its broad powers to revise the rules that have driven lenders from the chattel market, the industry turned to Congress.

HR 650, The Preserving Access to Manufactured Housing Act, passed the House of Representatives last month with bi-partisan support by a margin of 100 votes.

The bill revises high-cost loan triggers to reflect the realities of origination costs for manufactured homes, and addresses other anomalies in Dodd-Frank.

The Senate companion bill, S 682, is now making its way through the banking committee and is expected to come up for a vote next week.

CFED is S 682’s most vocal opponent, marshaling the forces of the consumer advocate community to defeat it.

The Congressional record reflects Barney Frank’s assertion that the law that bears his name was not meant to encompass manufactured housing, or to pave the path to affordable home ownership with unexpected land mines.

CFED’s Ryan remains convinced the measure is “very dangerous to consumers” and is going to make the loans more expensive.

But what could be more expensive than the loan Eric Powell was forced to acquire if he wanted to buy a home for his family?

First, says Ryan, he believes 21st Mortgage could have made the loan if it wanted to.

“I wouldn’t be at all surprised if they didn’t turn him down just to make a point that they can’t make loans under $20,000,” he says. “I wouldn’t put it past them.”

But 21st was only one of many companies that declined Eric’s loan on the basis of its small size.

Second, says Ryan, the loan Eric ended up with is a personal, unsecured loan, which is high risk — and unregulated.

The logic escapes Eric, but he refuses to be bitter about the price he ultimately will pay.

According to his loan agreement, the $9500 loan at 36 percent interest will cost him $20,561.23 at the end of five years. The up-front closing fees added $1500 to the amount financed.

Had he been able to find a lender willing to make such a small chattel loan under current Dodd-Frank rules, the origination fees would have been half that, the interest rate about a third.

But his payments are only $350 a month, compared to the $800 a month it cost to rent an apartment all those years.

Even at 36 percent, it was the best way to go, he says. “We’ll pay it off that much sooner.”

“Our desire to buy the home outweighed our desire to not pay 36 percent interest,” says Eric.

But, still, when he thinks of the law that was supposed to fix the financial world order to benefit people like him, he can’t help but wonder: “What were they thinking when they did that?” ##

Jan Hollingsworth is an award-winning journalist who has been widely recognized for depth reporting on consumer issues.

Jan Hollingsworth is an award-winning journalist who has been widely recognized for depth reporting on consumer issues.

Copyright (c) 2015, Lifestyle Factory Homes, LLC. Publisher grants permission to reprint unedited story in its entirety, with the link back and proper credit to MHLivingNews.com. https://manufacturedhomelivingnews.com/dodd-frank-and-manufactured-home-financing-the-place-where-good-intentions-and-unintended-consequences-collide/