manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

Samuel “Sam” Strommen from Knudson Law forged an evidence-based and systematic case that points the finger of monopolization at Clayton Homes, 21st Mortgage Corporation, Warren Buffett’s Berkshire Hathaway, and several specific members of the Manufactured Housing Institute (MHI). Minneapolis Federal Reserve professional researchers James A. Schmitz Jr and David Fettig have made their own evidence-based argument that “Monopolies Inflict Great Harm on Low- and Middle-Income Americans” a harm that monopolistic practices “in all its forms” creates. Among their reports, Schmitz and Fettig specifically cite affordable manufactured housing. These would-be trust busters are hardly alone in the growing numbers from across the left-center-right who are denouncing the contemporary Robber Barons of modern monopolization. The 45th President Donald J. Trump and current White House resident Joe Biden have also decried the harms caused by market manipulating monopolists.

Besides making the case against Clayton, 21st and other brands named herein, Strommen said below that he “submits that the MHI’s conduct in obfuscation judicious decision-making by the [FHFA and HUD] constitutes a conspiracy to restrain trade under Section 1 of the Sherman Act, and by virtue of the misrepresentative nature of the conduct, should not be afforded Noerr protection.”

Additionally, an FTC documented dated July 7, 2016 says that, “The FTC also has jurisdiction over non-profit organizations that operate for the profit of their for-profit members, including by providing substantial economic benefits to those members.5 In some instances, the FTC’s jurisdiction is concurrent with that of other law enforcement agencies.”

There have been requests that we publish a fresh version of the report linked below which was an exclusive to MHProNews from Strommen at Knudson Law. That report has its own rich context and added details is found at this link here below. Each stands on its own merit, and each provides useful insights for those motivated to understand and stop the harms caused by the apparently illegal tactics described.

That report above has routinely stayed in the top 1 percent of all reports since shortly after it was published on our MHProNews sister site. That said, this report will dive right into Strommen’s heavily-documented case that claims “felony” monopolization, possible RICO and other questionable and unethical activities occurring in manufactured housing. Following the footnotes further below, there will be a critique of this document provided by Strommen by a would-be defender of MHI and several of their dominating brands. Additional information at the end of this report about how Berkshire Hathaway, Clayton Homes, MHI and others have responded to these charges will be added too. With that introduction, here is Strommen’s legal ‘case.’

The Monopolization of the American Manufactured Home Industry

and the Formation of REITs:

a Rube Goldberg Machine of Human Suffering

Samuel Strommen

Antitrust & Consumer Protection

Research Paper

- Introduction

The American manufactured home, known colloquially as a mobile home, a prefab, or, most commonly, a trailer, stands alone as the most widely looked over and denigrated form of residence offered in this country today. In fact, it is the only form of residence in the United States that carries its own pejorative connotation, “trailer trash.” An apartment, on the other hand, carries no such connotation, and the utterance of the word allows the reader to envisage a full gamut of possibilities, from rundown urban projects to a posh Fifth Avenue penthouse. Likewise, a house, without context, likely inspires images of the average single-family home, with contextual connotations ranging from a squalid shanty to an opulent mansion.

The manufactured home…for tens of millions of Americans today—a great many of whom hail from the lowest socioeconomic stratum, it is a way of life, the only affordable living situation available, and the only means of achieving home ownership.

Here, in the midst of what could be declared without the merest hint of shame or irony one of the most comprehensive affordable housing gluts in American history, pernicious forces are skulking in the (backdrop): consolidating power, subsuming an industry rife with lack of oversight, and preying upon the vulnerability of the impoverished in a gross, incestuous symbiosis.

Manufacturers and financiers (oftentimes a single streamlined, vertically integrated entity) have taken advantage of, if not sold outright to their customers, a conflation of home ownership and owning a manufactured home. There is, however, a striking distinction between the two: home ownership, in the traditional sense, is to possess real property, along with all of the rights and privileges that are afforded with it. Manufactured homes, on the other hand (for reasons that will be explored later), are by and large personal property—chattels—and come with few of those same rights and protections one would find in a traditional home.

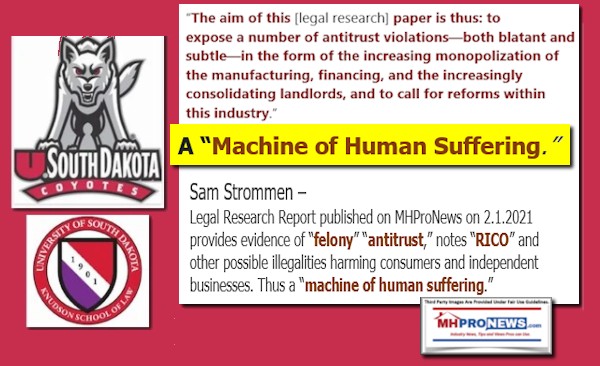

The aim of this paper is thus: to expose a number of antitrust violations—both blatant and subtle—in the form of the increasing monopolization of the manufacturing, financing, and the increasingly consolidating landlords, and to call for reforms within this industry.

Data on the manufactured home industry is scarce—very few studies that would pass any sort of academic muster have been published, and to make matters worse, much of the data appears to be obfuscated, both by the alleged bad actors as well as their critics.

Part of the problem is that manufactured homes go by a number of different aliases: colloquially, they are known as trailers or mobile homes. This is a misnomer. In 1976, the United States Department of Housing and Urban Development (HUD) released the Manufactured Home Construction and Safety Standards Code.[1] As a result, a “mobile home” is any home of the same variety manufactured before the codes were released, and a “manufactured home” is any home manufactured after.

It is unclear if modern publications, when referring to “manufactured homes” and “mobile homes” (oftentimes synonymously) are proffering data applicable to both types of homes, or just the former.

Furthermore, search results for each of the two terms tends to produce radically different results, with searches for “manufactured homes” tending to reveal more accurate, less biased data. To complicate matters, the last rigorous study of the industry by the federal government comes from a 2014 report published by the Consumer Financial Protection Bureau (hereafter CFPB),[2] an independent agency of the United States Federal Government that endeavored to gather as much information as possible about the industry: the geography, demographics, and financial data of the typical manufactured home owner and resident; and the market-share and business practices of the manufacturers. To illustrate the previous point, this report is only available by searching specifically for manufactured housing information; searching for mobile home data does not include this among its higher-ranking search results. While this CFPB report promised in its introduction to continue monitoring the industry, unfortunately, either no new report has been produced, or, if it has, is exceedingly difficult to locate. The data compiled herein is the most readily accessible and up-to-date as is available.

To fully understand the industry, it would be wise to first look towards the demographic data provided in the CFPB report. As of the time that report was published, manufactured housing accounted for some six percent of all occupied housing in the United States,[3] with some 22 million American residing in manufactured homes as their principal place of residence.4

Contrary to what major credible publications such as the Guardian5 or the Financial Times 6 state in think-pieces about the industry, the majority of manufactured home owners own both the home and the land, with about 62% of all manufactured home owners owning both the house and the land. This accounts for 48% of all manufactured home residents,7 with 30% owning just the home but not the underlying land, and another 18% renting both.8 Somewhere between 25-30% of all manufactured homes are situated in manufactured home communities9 (commonly referred to…as “trailer parks”). Manufactured homes are concentrated largely in Western and Southern States,10 and residents skew older,11 less wealthy,12 and generally less educated when compared to site-built homeowners.13

It is prudent to note, however, that simply because one owns both the home and the underlying land, that does not make the majority of manufactured homes real property, as is the case with site-built homes.14 The distinction comes from how the home itself is titled, which affects every aspect of the transaction, from the interest rates on the financing, the availability and types of financing, and the eventual appreciation and resale value.15

Even if the home owner owns both the land and the home, the likelihood that the home itself is titled as real property and not personal property is relatively slim: in 2013, the most recent year from which data is readily available, only 14% of new homes of this variety were titled as real property.16 In fact, the treatment of manufactured homes as personal—and not real—property is the default rule, with the encumbrance of additional documentation being required for it to be considered otherwise.17

The differences between real and personal property are myriad, but for the purposes of this paper, we will restrict the difference to that which is most relevant: the type of financing available. Real property, like a traditional home, qualifies for a more traditional form of financing, like a home mortgage. When a manufactured home sits on property owned by purchaser, generally both the land and the home qualify for a traditional mortgage.18 The average interest rate on a 30-year fixed-rate mortgage usually hovers around 3%, although this number can fluctuate.19

However, if the consumer wishes to place their manufactured home in a land-lease community, other land they do not own, or wish to title the home separately from the land as personal property or a “chattel,” they are only eligible for a chattel loan, the average interest rate for which is between 50 and 500 basis-points higher (around .5%-5%), depending on factors that usually affect interest rates.20 Moreover, many consumer protection laws such as the Real Estate Settlement Procedures Act (RESPA) apply only to traditional real property home loans, and not to chattel loans.21 The same is true for many state foreclosure and repossession protection laws.22 This becomes particularly injurious when it is taken into account that, despite some 48% of all manufactured home owners feasibly qualify for a traditional mortgage, only about 14% of new manufactured homes are titled accordingly.23

The United States today faces one of its greatest affordable housing crises in decades. Consumers looking for lower cost alternatives to site-built housing, particularly the thousands of retirees that are selling their site-built homes, have found, at face, manufactured housing to be an attractive, lower-cost alternative.24

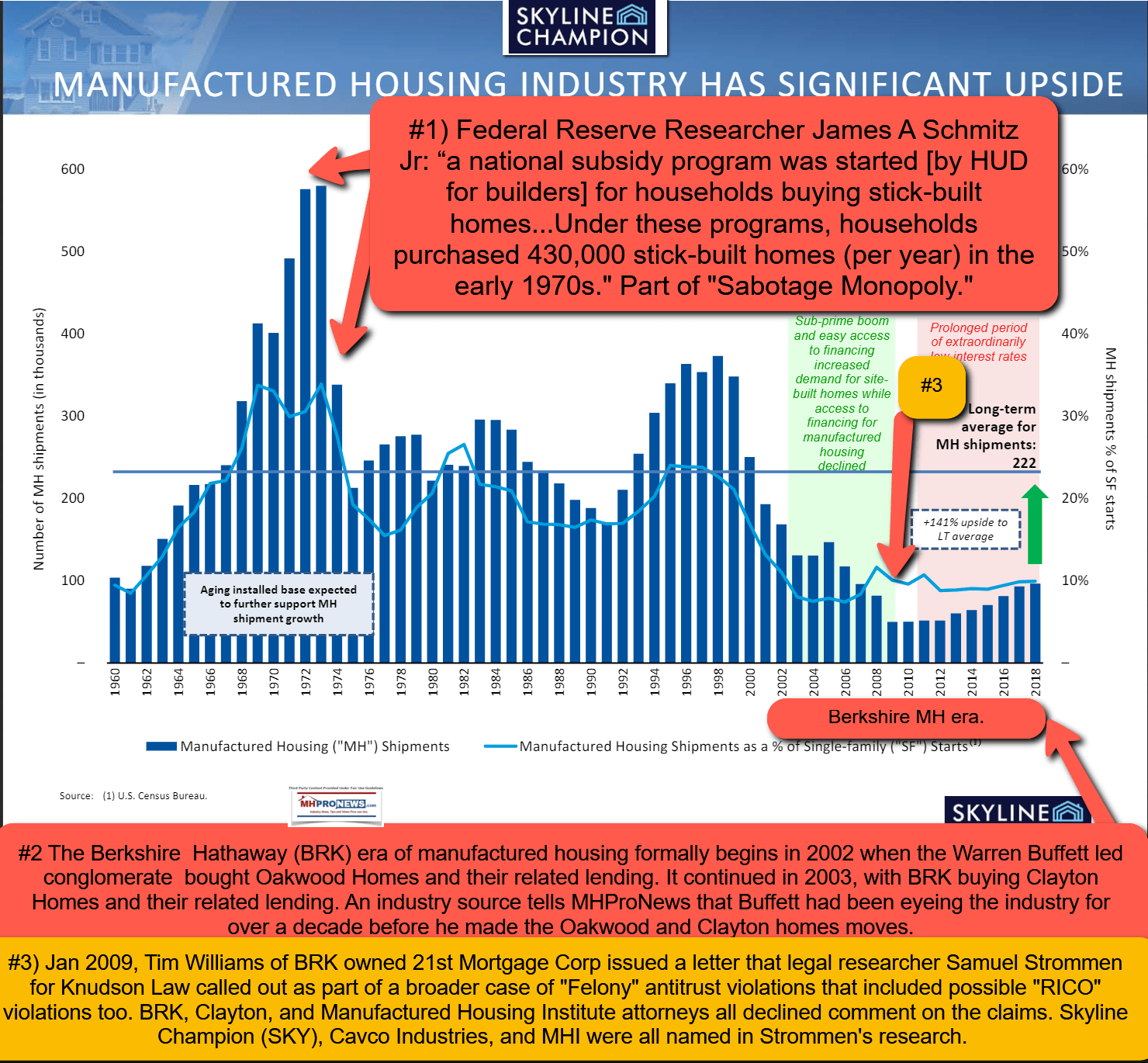

However, production of manufactured homes hit its apex over twenty years ago, with a maximum production of some 375,000 units in 1998.25 For much of the past two decades, the average production has dwindled to less than 100,000 new units produced annually, in the midst of an affordable housing crisis.26 This is directly correlated to how manufactured homes are financed and securitized: in the 1990s, standards for lending in the industry were tempered, and, as a result, the quality of the loans decreased.27 As sales of manufactured homes spiked, so did their value, with financiers over-appraising the values of homes and doing whatever they could—including filing fraudulent (or at the very least misrepresentative) credit applications on behalf of consumers.28

Housing giants Freddie Mac and Fannie Mae, two Government Sponsored Entities (GSEs), were once actively involved in securitizing these loans, with Fannie Mae securitizing some 24% of all manufactured home loans in order to meet its Duty-to-Serve mandate.29 With relaxed standards, however, these loans were far from investment grade and would, by today’s standards, be considered subprime.30 And despite a once Pollyannaish outlook towards the sector, today, the GSEs today maintain minimal involvement, securitizing few loans for manufactured homes and are arguably more involved in land-lease communities. They have a very limited number of home only or chattel loans, while more are classified as real property.31

By the early 2000s, lending in the industry had gone well-beyond its event horizon, with GSEs promptly exiting after losing billions in what could in no uncertain terms be described as a subprime lending crisis.32 If the aforementioned events sound familiar, it was an almost foreshadowing of sorts to the mid-to-late 2000s subprime mortgage lending crisis, precipitated by the same factors, and reaching a similar conclusion, albeit on a significantly smaller scale. Suffice it to say, that which fails the lowest cantons of society does not augur well for America as a whole.

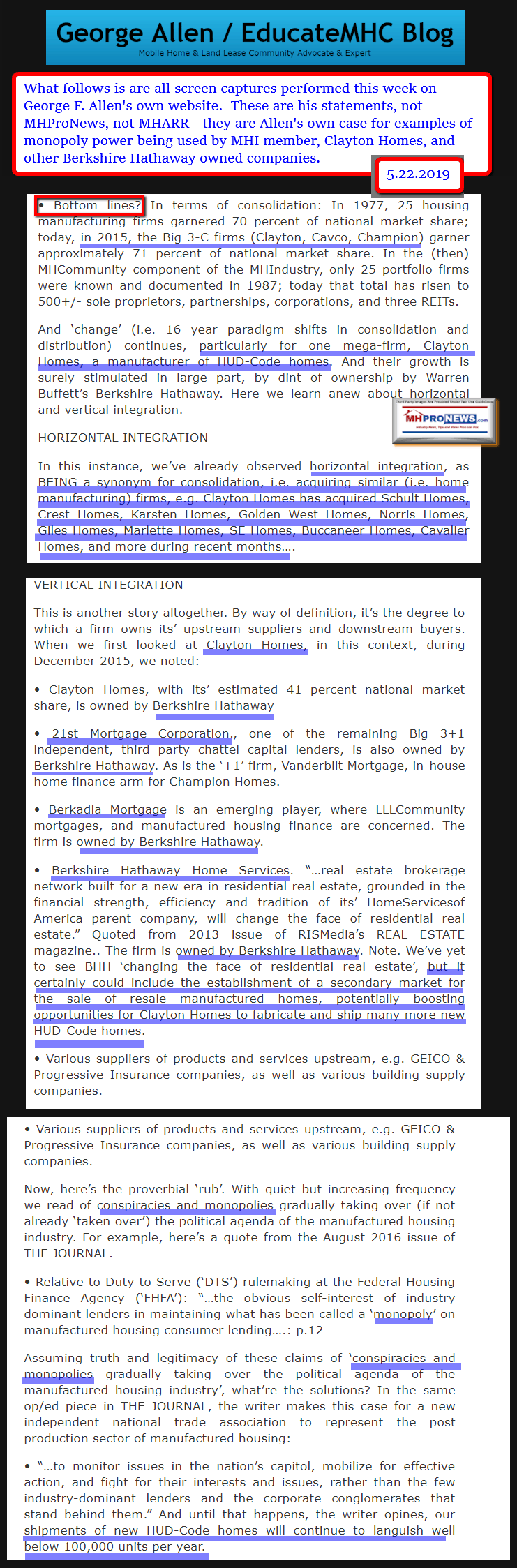

While the stories of how exactly Berkshire Hathaway came to acquire Clayton Homes vary depending on source, a few things remain certain: in 2003, Berkshire Hathaway purchased Clayton homes for $1.7 billion in cash.33 Today, there is perhaps no company more vertically integrated than Berkshire Hathaway and Clayton: Clayton uses almost exclusively materials that have been purchased from other Berkshire Hathaway subsidiaries.34 The paint is supplied by Benjamin Moore, the insulation is supplied by Johns Manville.35 The two predominant lenders in the industry, 21st Mortgage Corporation and Vanderbilt Mortgage and Finance are themselves both wholly-owned subsidiaries of Berkshire Hathaway as well. So, when a consumer purchases a manufactured home from Clayton Homes, Berkshire Hathaway routinely profits in some form or another at several stages.36

While claims that Berkshire Hathaway vis-à-vis Clayton Homes have violated American antitrust law have not been litigated in court, ample evidence that violations are taking place are myriad.

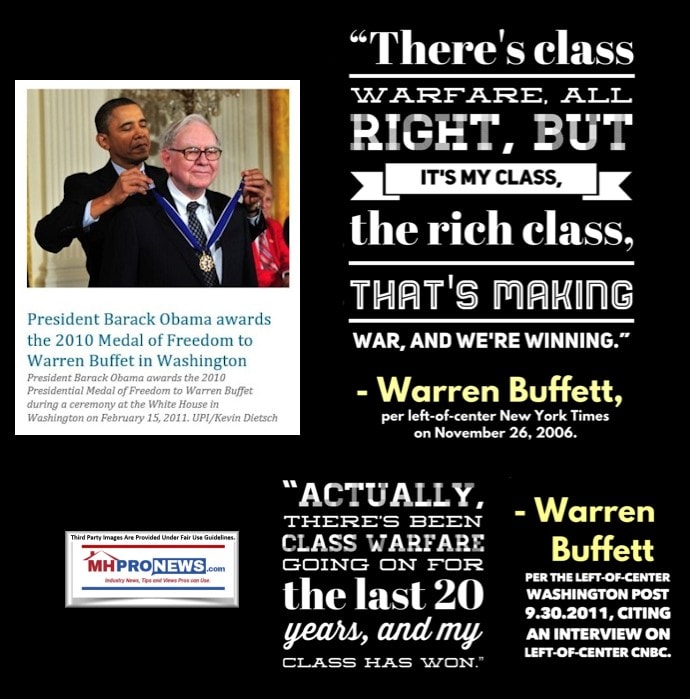

Buffett’s own words on his business strategy provide valuable insight into Clayton Homes’ strategy in this sector: “A good business is like a strong castle with a deep moat around it,” Buffett said on a CNBC broadcast, “I want sharks in the moat. I want it to be untouchable.”37 In this analogy, the castle would be the business he has invested in, fortified and standing safe from outside attack. The shark-filled moat is representative of the litany of additional deterrents Buffett-led Berkshire Hathaway has at its disposal to ward off nascent competitors as well as regulators.

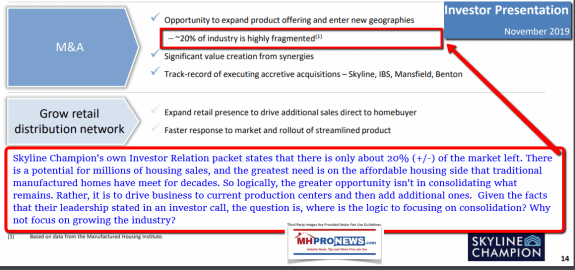

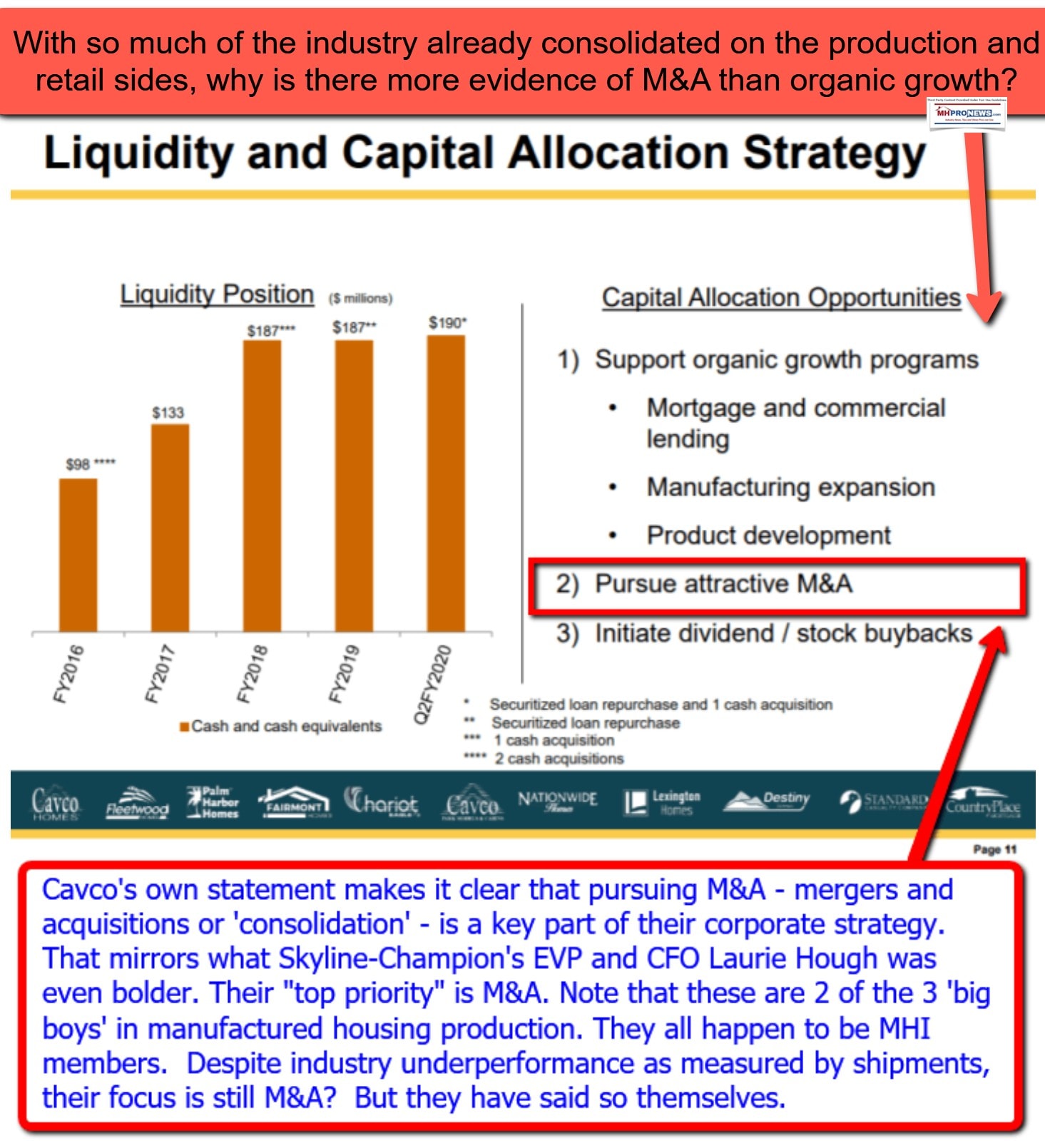

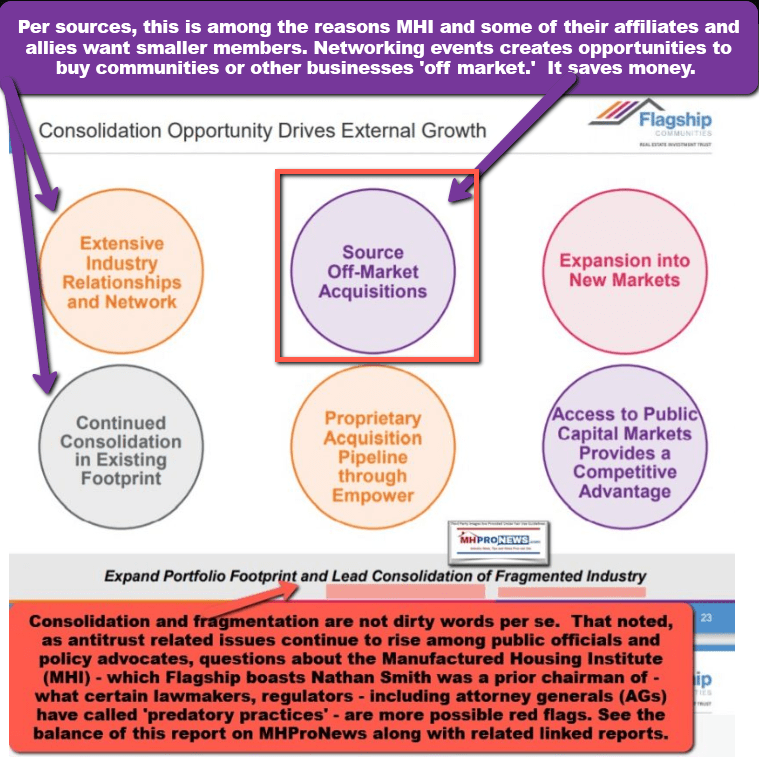

In 2002, prior to Berkshire Hathaway’s acquisition of Clayton Homes, there were 88 manufacturers scattered across the United States.38 Today, the number has fallen to less than half that.39 A report from the now-defunct Manufactured Home Merchandiser publication indicates that in 2003, Clayton was the third largest manufactured home fabricator40 in the United States, and at that time, the top twenty-five manufacturers accounted for 78% of all home production and sales.41 Today, Clayton, Skyline-Champion, and Cavco, the top three, account for some 80% market share combined.42 Clayton alone comprises about 51% of manufactured home production.43 A series of mergers and acquisitions has made this industry increasingly consolidated.

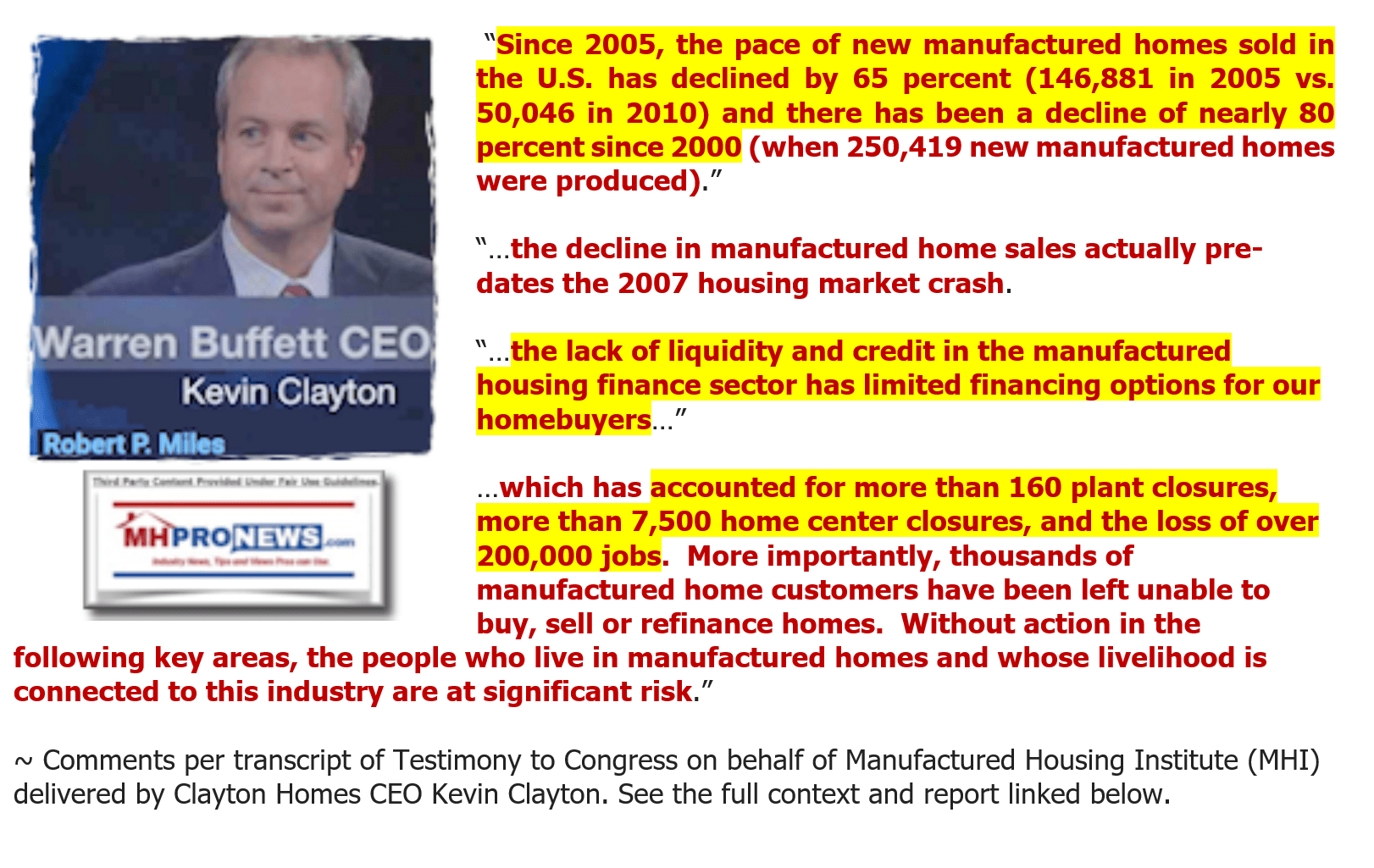

There was a brief increase in production and shipment numbers, apparently due largely to FEMA purchases in 2005 post-Katrina, but the numbers declined following that blip [ibid]. Those numbers nonetheless correlate with that acquisition.44 The United States, again, is undoubtedly in the midst of an affordable housing crisis, and manufactured homes account for 75% of all homes sold in the United States for less than $125,000.45 Puzzlingly, while profits for the three largest players in the industry have continued to grow, the industry has yet to come close to producing as many homes as it did before Berkshire Hathaway’s acquisition.46 To make matters more troubling, intentions, both stated and inferred-by-conduct, of the industry leaders is to increase profitability not by selling more homes, but by eliminating competition.

Lori Hough, one of the vice presidents of Clayton “competitor” Skyline Champion, stated in a shareholder conference call that her company was focused principally on mergers and acquisitions as its primary method of growth.47 Moreover, since 2009, a pivotal year in the industry, Clayton itself has gone on to acquire the following companies: Schult, Crest, Karsten, Golden West, Norris, Giles, Marlette, SE, Buccaneer, A and Cavalier Homes.48 Cavco, a third member of the industry’s “Big 3” has, over the same time span, acquired Destiny, Lexington, Fairmont, Chariot Eagle, Palm Harbor, A and Fleetwood Homes.49

Clayton’s conduct here could be construed as a potential violation of Section 2 of the Sherman Antitrust Act, which states in part: “Every person who shall monopolize, or attempt to monopolize, or combine or conspire with any other person or persons, to monopolize any part of the trade or commerce among the several States, or with foreign nations, shall be deemed guilty of a felony[.]” While monopoly status has yet to be attained, Clayton’s growth over the past 17 years has been meteoric: Clayton’s market share has gone from a paltry 13.9%51 to a commanding estimated 51%.52 The number of firms they and the two other industry leaders have either acquired, merged with, or squeezed out has pushed down the total number of competitors in production-sector of the industry virtually since its inception.

In addition to potentially constituting a violation of Section 2 of the Sherman Act, this may also constitute a separate violation of Section 18 of the Clayton act, which states:

“No person engaged in commerce or in any activity affecting commerce shall acquire, directly or indirectly, the whole or any part of the stock or other share capital and no person subject to the jurisdiction of the Federal Trade Commission shall acquire the whole or any part of the assets of another person engaged also in commerce or in any activity affecting commerce, where in any line of commerce or in any activity affecting commerce in any section of the country, the effect of such acquisition may be substantially to lessen competition, or to tend to create a monopoly.”53

Here, it would appear that Clayton Homes, Cavco Industries, and Skyline Champion are doing just that: In 2003, when Berkshire Hathaway purchased Clayton Homes, Champion was the largest manufactured home builder.54 Skyline was the fifth largest, and the two companies have now merged.55 Of the top twenty-five largest manufactured home builders in 2003, Clayton itself purchased or merged with Oakwood, the fourth largest,56 Cavalier, the seventh largest,57 Southern Energy, the ninth largest,58 and Golden West, the fifteenth largest.59 Cavco at the time was the twelfth largest,60 has since merged with or acquired Fleetwood Homes, which was previously the second largest,61 Palm Harbor, the sixth largest,62 and Fairmont, the tenth largest.63 What was previously a top ten has amalgamated into a top three. What the industry has presented as apotheosis is closer to apoptosis.

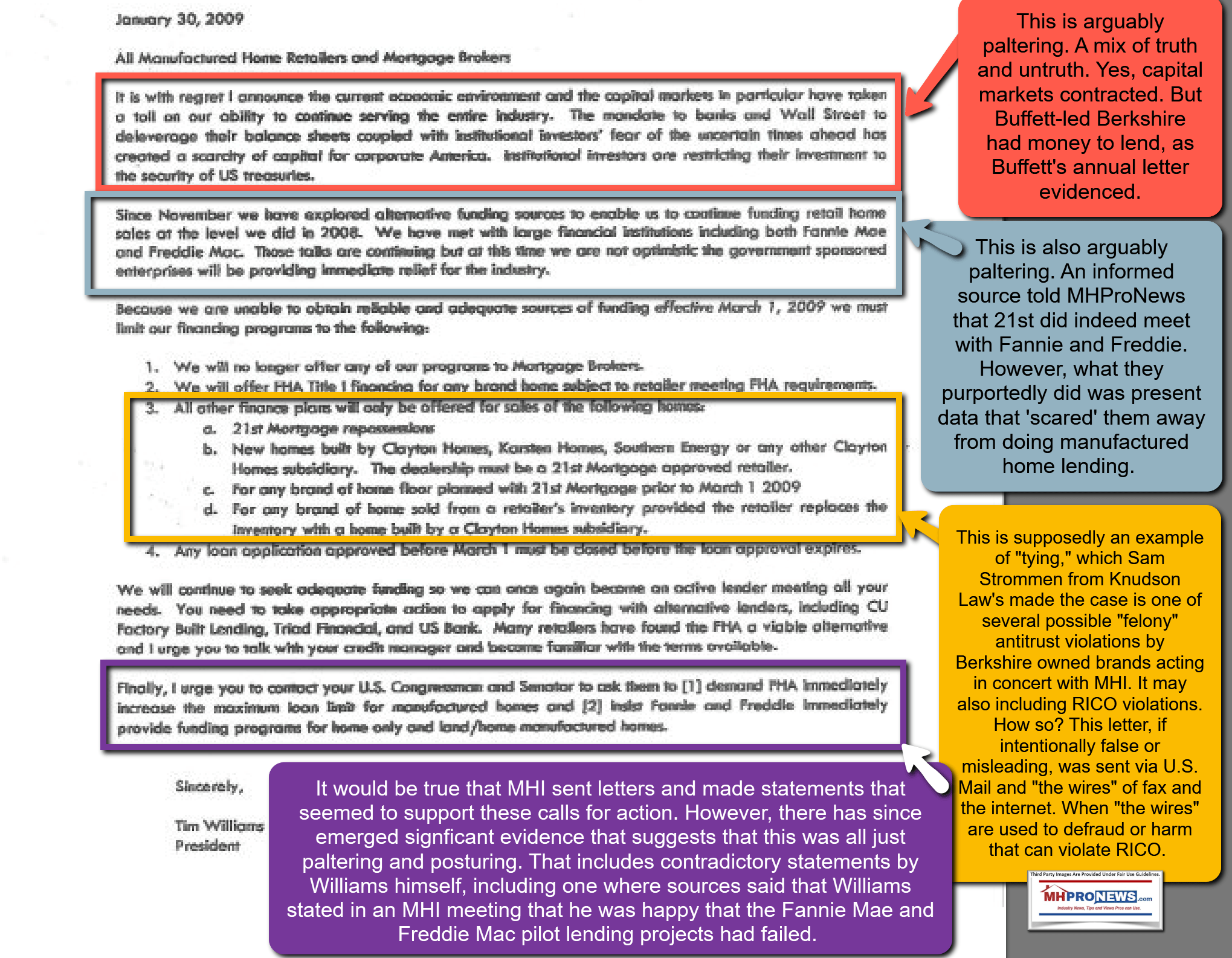

While a precise history of the industry’s mergers, acquisitions, and outright failure of competition is less than perfectly discernible, it is quite clear that the year 2009 had a devastating impact on competition. It was in this year that 21st Mortgage Corporation…, a Clayton Homes sister-brand and Berkshire Hathaway subsidiary that provides financing within the industry to independent retailers, sent out a letter to its retailers indicating that it was no longer capable of finding sufficient sources to sustain their then-current levels of reliable financing. As a result, financing through 21st Mortgage was no longer going to be offered to mortgage brokers.64 Furthermore, outside of FHA-insured loans, only 21st […Mortgage] repossessions and homes built by Clayton or one of its subsidiaries would be eligible [for 21st lending]—retailers also had to be approved.65 Prior to this letter being sent, there were still 61 total manufactured housing corporations in the United States.66 Within two years, twenty-one competitors either failed, or were acquired.67 The true content of the message was made manifest not by what it said, but rather the implied consequences: capitulate to Berkshire Hathaway, or fail.68

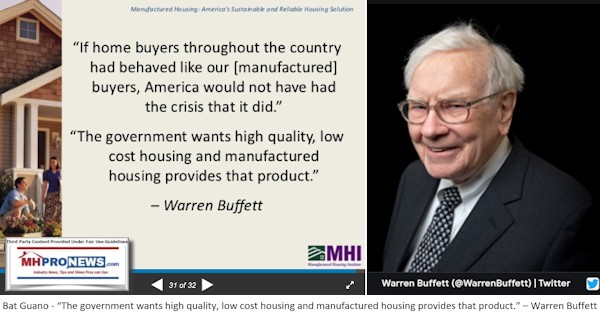

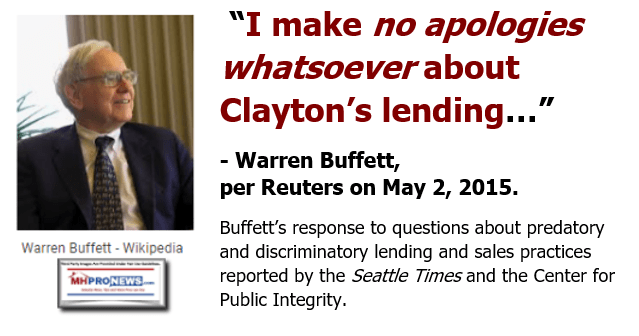

In public, Buffett boasted through a rictus that Clayton and its financing arm were performing a good deed, saying:

“Lenders other than Clayton have come and gone. With Berkshire’s backing, however, Clayton steadfastly financed home buyers throughout the panic days of 2008-2009. Indeed, during that period, Clayton used precious capital to finance dealers who did not sell our homes. The funds we supplied to Goldman Sachs and General Electric at that time produced headlines; the funds Berkshire quietly delivered to Clayton both made home ownership possible for thousands of families and kept many non-Clayton dealers alive.”69

As has become thematic throughout the course of this paper, however, it was what was left unsaid that was more telling: shortly after this, in the midst of the subprime lending crisis, Clayton and 21st switched course. While its Vanderbilt subsidiary always appears to have been a captive lender to Clayton, this was not the case for 21st.70

The [Tim Williams/21st] letter itself appears to be another clear violation of Section One of the Sherman Act, as well as Section Three of the Clayton Act, which prohibit what is colloquially called “tying.” This section of the Clayton Act states in relevant part:

“It shall be unlawful for any person engaged in commerce, in the course of such commerce, to lease or make a sale or contract for the sale of goods…on the agreement, or understanding that the lessee or purchaser thereof shall not use or deal in the goods…of a competitor or competitors of the lessor or seller, where the effect of such lease, sale, or contract for sale or such condition, agreement, or understanding may be to substantially lessen competition or tend to create a monopoly in the line of commerce.”71

Here, Clayton [Homes and their affiliated lending] have done exactly that: from 2009 going forward, outside of loans insured by the FHA, if a retailer was going to offer 21st Mortgage financing, that financing was only going to be available for homes built by its parent company. To elaborate, in Jefferson Parish Hospital District No. 2 v. Hyde,72 and Eastman Kodak Co. v. Image Technical Serves., Inc.,73 The Supreme Court has established four elements for identifying unlawful tying arrangements:

- Whether the seller is selling two separate products that may be tied together;7[4]

- The sale or lease of an item on the condition that the buyer make all his purchases of a separate tied product from the seller;7[5]

- The seller has the market power to tie the products, i.e. “the power to force the purchaser to do something he would not do in a competitive market”;7[6]and

- A “not insubstantial amount of interstate commerce in the tied market is affected.”[7]7

Let us examine each of these elements in a vacuum, and then as an aggregate. For element one: through 21st, Clayton is selling homes and mortgages for those home, which are two separate products (in traditional home buying, these are rarely, if ever, tied together). For element two: in the letter, 21st stated and followed through by choking off credit to retailer that did not sell Clayton homes, or for any homes the retailer sold that were not Clayton homes. For element three: the seller has inordinate market power to force retailers to accept the tying arrangement, whether they liked it or not. Finally, and most clearly, a not insubstantial amount of interstate commerce has been affected: Clayton, its subsidiaries, and its two chief competitors have functionally eradicated any serious, cognizable competitor from the industry. If the last element is met, that alone may be sufficient to constitute a per se violation of the Sherman and Clayton Acts.78

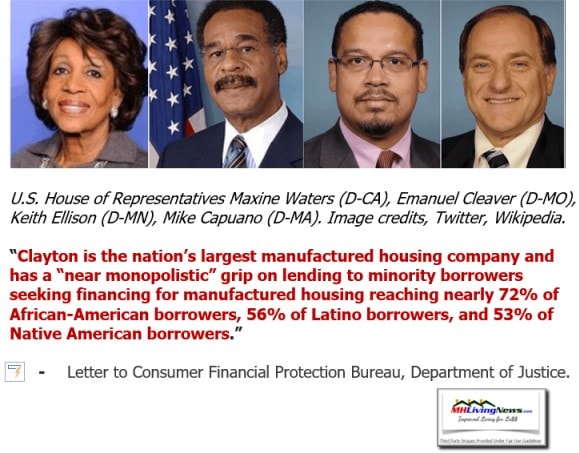

The record makes it clear: Clayton Homes and its subsidiaries, Vanderbilt and 21st, backed by Berkshire Hathaway capital, are the runaway giants in the chattel mortgage sector that dominates financing in the manufactured housing sector. Some reports indicate that they provide more financing in the manufactured housing industry by a factor of seven.79 In fact, the third largest financier in the industry is Wells Fargo.80 As it stands, 21st and Vanderbilt’s ultimate parent company, Berkshire Hathaway, is the fifth largest stakeholder in Wells Fargo.81 Prior to Berkshire Hathaway’s divestment of some 46% of its Wells Fargo shares, it was the single largest stakeholder.82 As recently as 2017, it held some 13% of Wells Fargo shares, far and away more than the next largest shareholder.83 There is even some indication that the loans Wells Fargo is making in this industry are themselves backed by Berkshire Hathaway.84 With such a suffocating control over the financial side of the industry, Berkshire Hathaway has enabled Clayton Homes to go from one of many in an industry with stiff competition to dominant force in a market it has not only vertically integrated, but is in the midst of horizontally integrating as well.

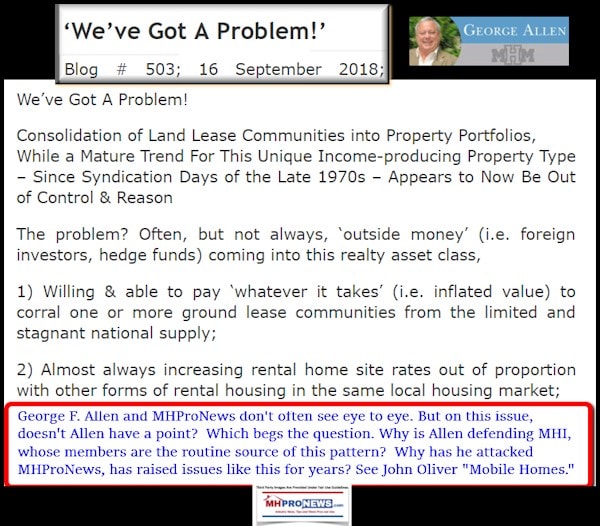

The expungement of competition has borne a demonstrably negative effect on consumers as well. Most Americans derive the majority of their net worth from the equity in their homes.85 As noted above, however, titling one’s manufactured home as a chattel not only restricts the availability of financing to usurious Berkshire Hathaway-backed loan, but chattel depreciation has a tendency to counteract the appreciation of the real property it sits on, if the consumer in fact owns both.86 In what is potentially another claim for tying under the Sherman and Clayton Acts, much like retailers, consumers are pushed to only finance through Clayton lenders.87 Other options, including traditional mortgages, may be obfuscated altogether.88 Former independent retailers have indicated they received kickbacks or discounts on their own financing for pressuring customers to take chattel mortgages through Clayton.89 Customers are [purportedly] often made to believe that it was either the best option available, or the only option available.90 This is despite the fact that some 93% of these loans have such high interest that Federal law requires additional disclosure.91 Industry consultants and experts believe that about 28% of these loans are in default.92 While courts have held that traditionally anticompetitive behavior may justify skirting antitrust law if there is an economic efficiency available to consumers,93 here, there is not.

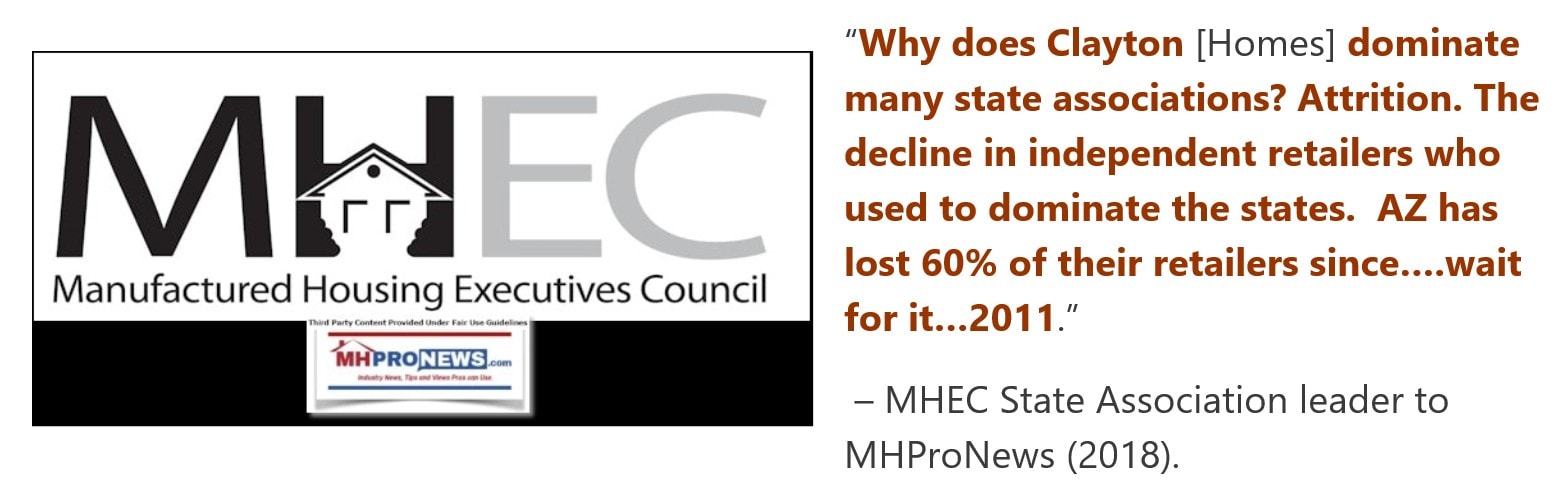

Berkshire Hathaway and its subsidiaries’ anticompetitive behavior is quite clearly injurious to consumer, but in this matter, they are not alone. It would appear that Cavco Industries and Skyline Champion are willing [de facto allies]. An additional [possible] antitrust violation, in the form of a conspiracy under Section 1 of the Sherman Act, would at this point seem [like a] fait accompli. This section declares: “Every contract, combination in the form of trust or otherwise, or conspiracy, in restraint of trade or commerce among the several States, or with foreign nations, is declared to be illegal.”94 However, this begs the question not of the method but the mode by which the three industry leaders are using to accomplish this. The answer to that would appear to be the industry trade association, the Manufactured Housing Institute. The Manufactured Housing Institute [MHI] acts not only as the public mouthpiece of the Big 3 manufacturers (in the name of the industry) but also appears to act directly on its behalf in its various lobbying endeavors.95

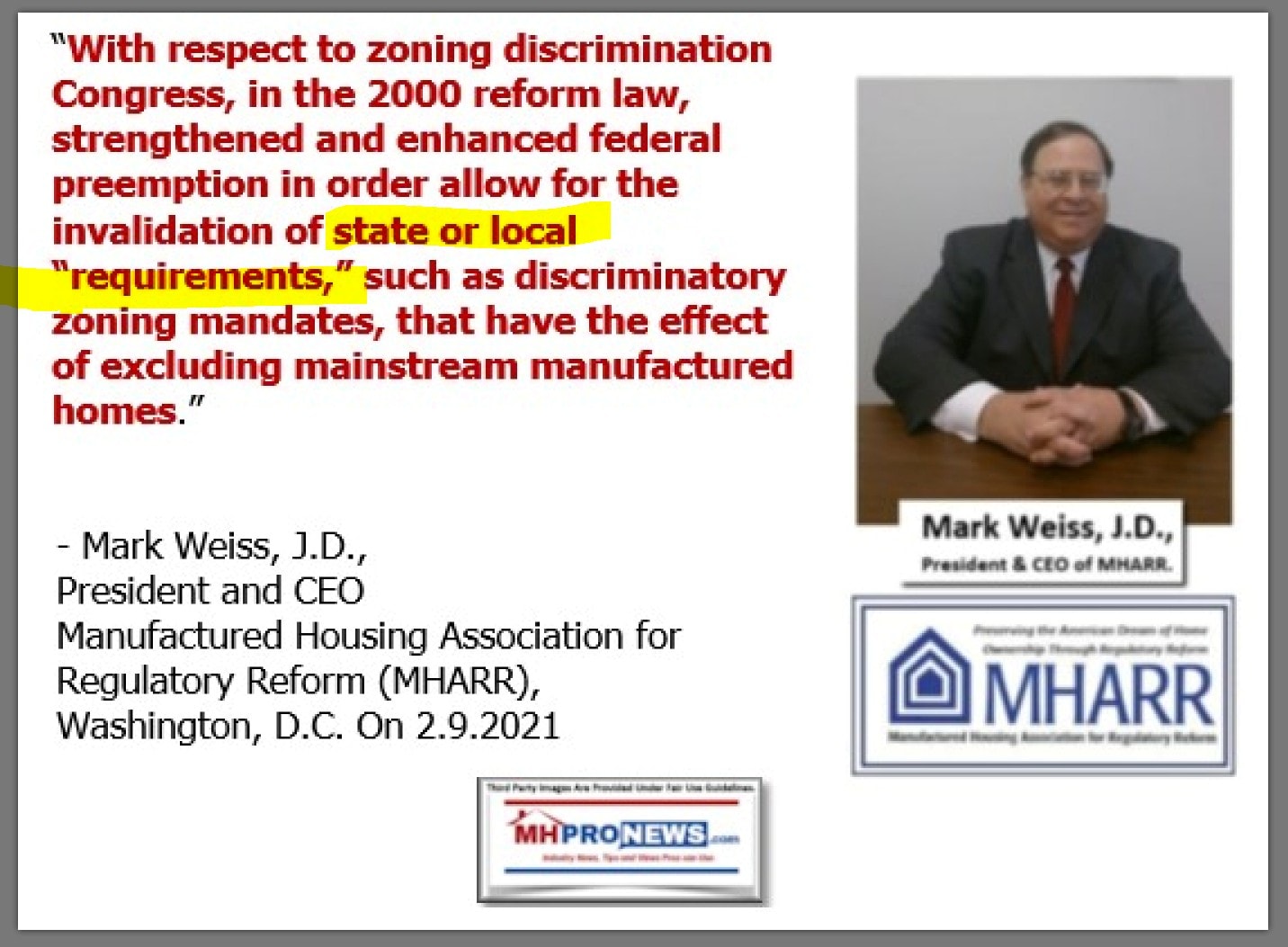

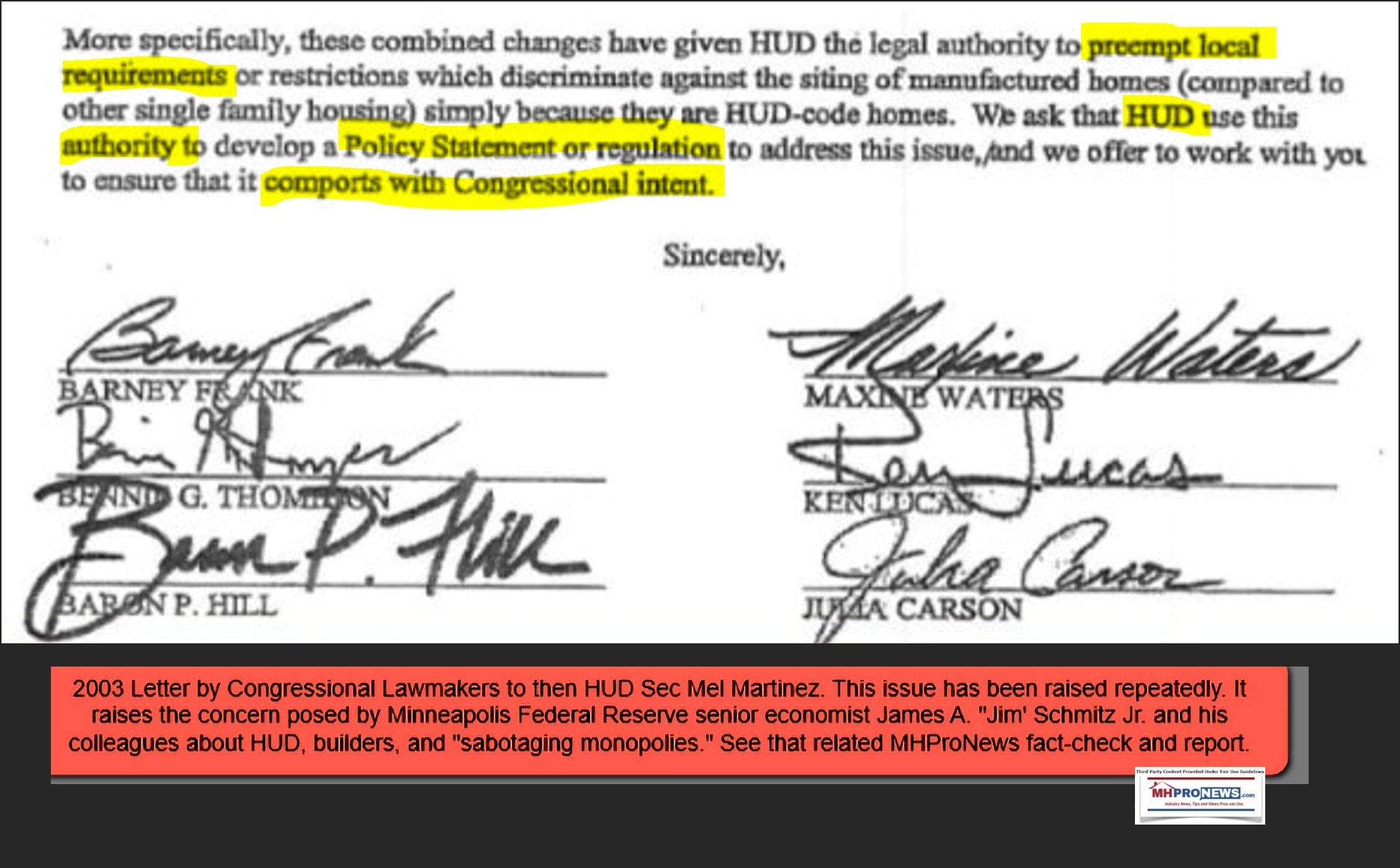

In the year 2000, Congress passed the Manufactured Housing Improvement Act.96 This act authorized “enhanced preemption,” which superseded all state and municipal standards, allowing manufacturers to deliver and install manufactured homes in separate jurisdictions provided they meet HUD standards.97 In 2008, the Federal Housing Financing Authority [FHFA], under the authority of the Housing and Economic Recovery Act of 2008, implemented an expanded Duty to Serve regulation, requiring Fannie Mae and Freddie Mac to facilitate home financing for very low-, low-, and moderate-income families.98 It should follow logically, then, that it should be cheaper and easier for residents of any state to finance and acquire a manufactured home. Unfortunately, this is not the case.

There may be no greater indicator of collusion by the industry Big 3 through the MHI than HUD’s ongoing failure to implement enhanced preemption and for the [FHFA to compel the] GSEs to follow through on the Duty to Serve mandate. To call this ongoing failure a coincidence is a risible proposition: promotion of these runs contrary to the Big 3—and Clayton’s—interests in particular. The stated purpose of the GSEs is to securitize mortgages by purchasing them from lenders, packaging them together, and selling them as mortgage backed securities to investors. By alleviating lenders of the burden of having their capital tied up in loans that tend to amortize over periods of decades, liquidity—and thus allocable credit—is freed up, making credit cheap and lending competitive.

Clayton Homes [and their affiliated lenders] would suffer a detriment if [the] GSEs were to re-enter the chattel mortgage industry: it [apparently] does not need nor want capital from a large pool of investors, it accesses the capital through its parent company, Berkshire Hathaway.100 If GSEs undertook their Duty to Serve, it is hardly speculative to assert that Clayton—and Berkshire Hathaway’s—bottom lines would suffer, both from a new volume of competitors entering the market, as well as lower interest rates from more competitive lending. Accordingly, there is evidence to suggest that MHI has lobbied against any efforts that would threaten to disrupt the profitable and vertically integrated complex Clayton has developed.101 In fact, as recently as 2012, when major reforms were last announced, objections by the MHI led to manufactured housing being exempted.102

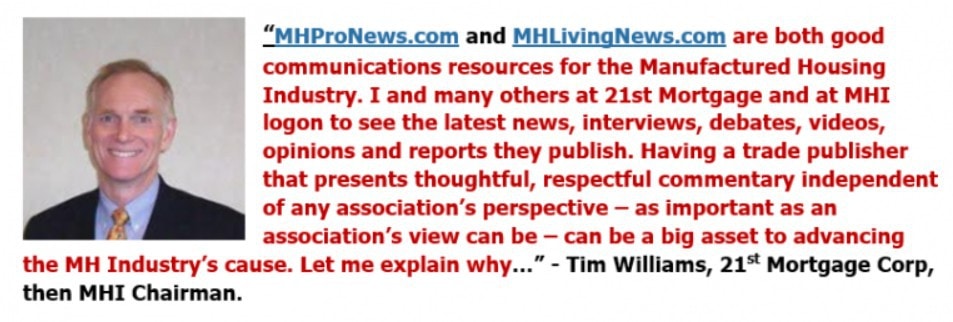

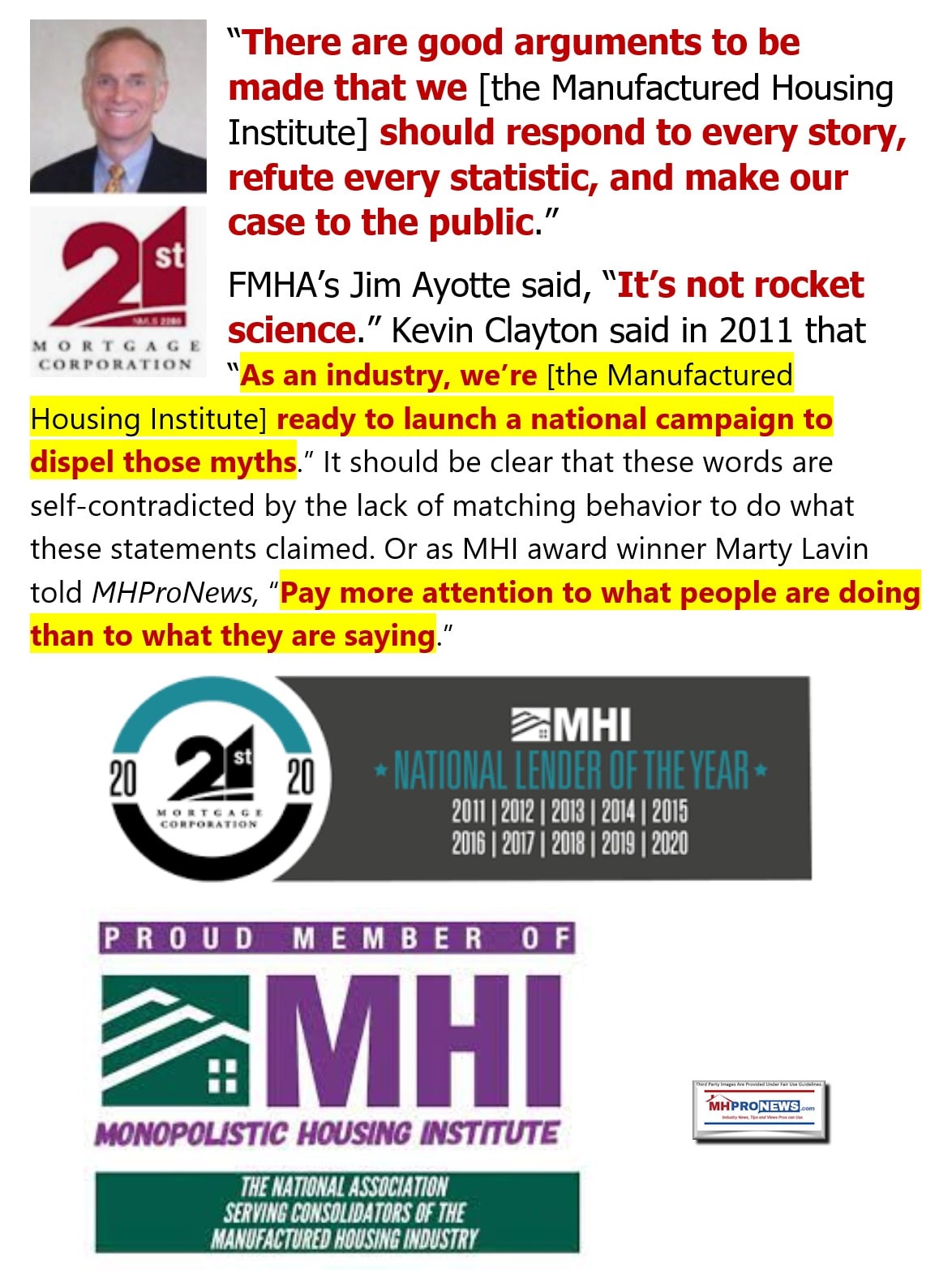

After exiting the manufactured housing market in the early 2000s, the two GSEs have yet to return in any meaningful sense.103 There are indications that the GSEs have securitized [only a limited number of manufactured home loans] in the industry since their departure after the aforementioned subprime lending crisis that occurred in the late 1990s.104 The MHVillage’s [MHInsider], which serves as an unofficial trade publication for the Manufactured Housing Institute, has heralded in several of its recent issues that the MHI has made great inroads with the GSEs, particularly in their implementation of the MHAdvantage and Choice Home programs. However, for the two GSEs to securitize these loans, the price range must be between $200,000-$250,000, and they must be titled as real property, [nor are] and they available to homes that will be placed in land lease communities. With a broader view of the industry in mind, these programs essentially serve no one, and certainly do not fall within the scope of the GSEs’ Duty to Serve mandate. In the same issue, Tim Williams, the same gentlemen from 21st Mortgage [and former MHI Chairman] who authored the letter that may be a violation of tying mentioned above, stated that they (Manufactured Housing Institute members) “are better suited to serve communities than GSEs.”109

Furthermore, while MHI claims to represent the industry as a whole, a look at the incestuous nature of the Big 3 and MHI make it clear whose interests are actually being represented: currently, half of the MHI executive [committee board members] are former employees of Clayton Homes.110 As mentioned above, MHI (and MHInsider) has touted programs such as MHAdvantage and ChoiceHomes.111 However, these programs benefit a single new, trademarked class of manufactured housing: CrossMod™ homes.112 A cross-reference on the U.S. Patent Office’s website indicates that MHI is the holder of the CrossMod trademark.113 The only manufacturers (in principal) able to produce—and thus take advantage of programs such as MHAdvantage and ChoiceHomes are [essentially] MHI members.114 It would appear that MHI’s lobbying efforts are done less to serve the industry as a whole, but rather to keep competitors—and consumers—from accessing competitive rates on lending if the Duty to Serve were properly implemented.

MHI’s relationship with HUD and the GSEs is no secret: most recent issues of MHVillage[’s MHInsider] touts some form of progress.115 And yet, only a few loans for this new class of home have been securitized by GSEs.116 MHIs lobbying of the FHFA, or for that matter HUD, seems to invariably result in in policies that either benefit the Big 3, or at the very least, mitigate detriment. The outcome of these lobbying efforts is stultifying at best, and an abject failure at worst.

For as heavily as MHI has promoted CrossMod™ homes, sales appear to be stagnant, particularly when demand in the sector remains focused on traditional manufactured housing.117 This begs the question: when lobbying [FHFA on the Duty to Serve], was MHI acting in good-faith? The U.S. Supreme Court has held in Eastern Railroad Presidents’ Conference v. Noerr Motor Freight Inc.,118 and United Mineworkers v. Pennington119 that the use of governmental processes such as lobbying or litigating by private [enterprise] is covered by the First Amendment right to free expression and the right to petition. That right extends even if the use of said processes is done to achieve an anti-competitive purpose that would otherwise be unlawful under antitrust law. The famous Noerr-Pennington doctrine is not without exceptions, however. In California Motor Transport Co. v. Trucking Unlimited, the Court identified that there is a “sham” exception to the doctrine’s protections.112 While the Court has never elucidated what exactly constitutes a sham, it is essentially an attempt to disguise the anticompetitive, purely business-related behavior as political—antitrust legislation is designed, after all, to regulate the sphere of business alone.

The Federal Trade Commission published a guide for regulators in 2006 that serves to elaborate on what is—and is not—protected by the Noerr-Pennington doctrine.123 The document outlines three activities that constitute a sham within the Noerr-Pennington context: filings that seek only a ministerial response,124 misrepresentations,125 and repetitive petitioning.126 Of these, MHI’s behavior, if indeed done to mislead or defraud the government, most closely resembles the misrepresentation exception. The deciding factor as to whether misrepresentations are afforded Noerr protection is if they are done to achieve a specific political outcome, even if that outcome is anticompetitive, or if there is an abuse of the process itself to hinder competition.127 In its Union Oil Co. of Cal. (Unocal) opinion, the FTC identified three elements for a petitioning or lobbying effort to lose Noerr protection: the representation must be (1) deliberate,128 (2) subject to factual verification,129 and (3) central to the legitimacy of the affected governmental proceeding.130

The author of this paper submits that the MHI’s conduct in obfuscation judicious decision-making by the [FHFA and HUD] constitutes a conspiracy to restrain trade under Section 1 of the Sherman Act, and by virtue of the misrepresentative nature of the conduct, should not be afforded Noerr protection. The intent of the MHI to influence [FHFA and] HUD to act in a particular way, or omit to act in a certain way, would be protected—however, the chief misrepresentation is that lobbying efforts are representative of an industry and not a select few companies. The data supplied to governmental officials is likely erroneous,131 and the attempts by the MHI to obtain governmental intercession on the industry’s behalf is likely a ruse.

Under Noerr, if obtaining securitization of loans for CrossMod™ homes is in fact MHI’s desired political outcome, its lobbying efforts to support that would be protected under the First Amendment. However, this would appear to be a strategy not dissimilar to the old cup-and-ball trick: a misdirection by MHI at the behest of its principal benefactors—the Big 3—an act of skillful subterfuge to misdirect the government in one area, allowing the Big 3 to engage in anticompetitive in another area unabated. This is supported by more than simple inference: industry leaders have lauded GSEs failure,132 sales of CrossMod™ homes remain far below that of traditional manufactured homes,133 and that seemingly every time reform in the industry or intrusion by GSEs is proposed, in nearly the same breath it vanishes.

The manufactur[ing] and lending sectors of the industry are rife with potential antitrust violations, from the Sherman Act, to the Clayton Act, to potential violations of the Noerr-Pennington Doctrine. It is clear that the Federal Trade Commission and United States Department of Justice should investigate these companies. The American consumer can ill-afford to pretermit manufactured housing as a viable option in the midst of an affordable housing crisis. Traditional site-built homes have continued to increase in price since the mid-2000s subprime mortgage crisis, and industry experts are predicting that the joblessness caused by the COVID-19 pandemic will fuel a second foreclosure crisis in America. Clayton Homes, et al. have gotten demonstrably more profitable. Why has manufacturing yet to cross the 100,000 unit threshold, much less come anywhere close to its most recent 1998 peak? ##

—————————————————————————-

[Editor’s Note: The footnotes by Strommen from the above are as shown below.

Note that the two … above reflects edits on apparent typos on Berkshire Hathaway (BRK) owned

21st’s corporate name 21st Mortgage Corporation.]

2 U.S. Consumer Financial and Protection Bureau, Manufactured-Housing Consumer Finance in the United States (2014), available at https://files.consumerfinance.gov/f/201409_cfpb_report_manufactured-housing.pdf.

3 Id., at 6.

4 Industry Trends & Statistics, MHInsider (July 2020), at 38, available at https://www.mhvillage.com/pro/print/july-august-2019/.

5 Rupert Neale, America’s Trailer Parks: The Residents May Be Poor but the Owners Are Getting Rich, The Guardian, May 3, 2015, available at https://www.theguardian.com/lifeandstyle/2015/may/03/owning-trailer-parks-mobile-home-university-investment.

6 Rana Foroohar, Why Big Investors Are Buying Up American Trailer Parks, Financial Times, Feb. 7, 2020, available at https://www.ft.com/content/3c87eb24-47a8-11ea-aee2-9ddbdc86190d.

7 CFPB, supra note 2, at 21.

8 Id.

9 Id.

[10]0 Id. see Figure 1: Manufactured Housing Share of Occupied-Housing Units, by State. [11] Id., see Figure 3: Head-of-Household Age Distribution. [12] Id., see Table 3: Selected Family Financial Characteristics by Type of Housing. [13] Id., see Table 2: Highest Level of Educational Attainment by Residents Ages 25 or Older in Owner-Occupied Households. [14] Id., at 6. [15] Id. at 23. [16] Id. [17] Id. at 10. [18] Jeff Ostrowski, 30-Year Interest Rates, Nov. 9, 2020, available at https://www.bankrate.com/mortgages/rates/30-year-rates-for-monday-november-9-2020/. [19] J.B. Maverick, The Most Important Factors that Affect Mortgage Rates, Jun. 25, 2019, available at https://www.investopedia.com/mortgage/mortgage-rates/factors-affect-mortgage-rates/20 CFPB, supra note 2, at 6.

21 Id. at 24.

22 Id.

23 CFPB, supra note 16.

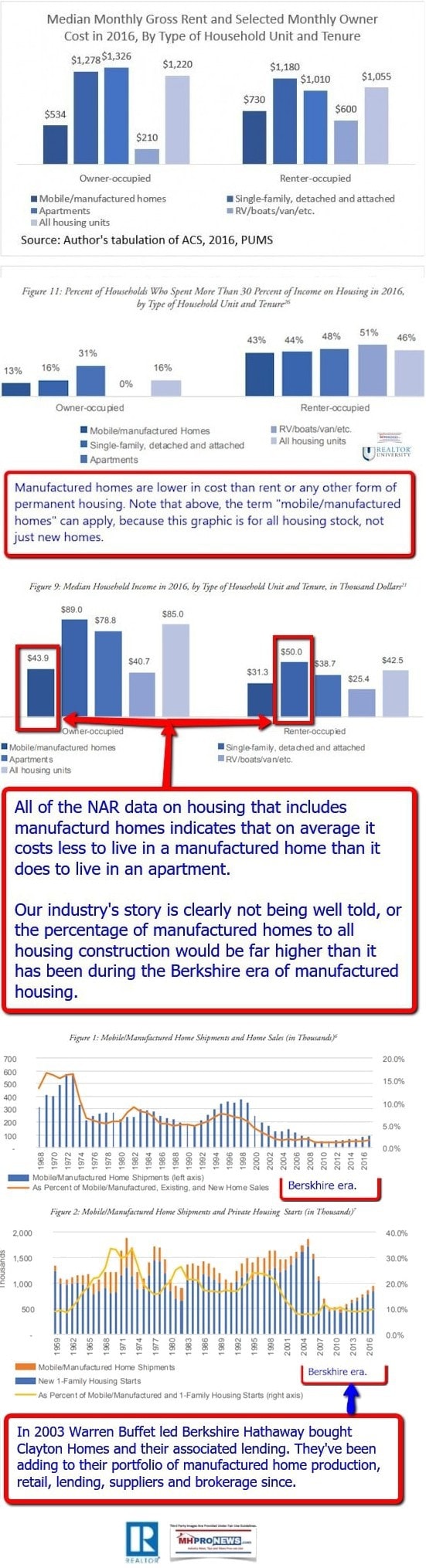

24 See graphic download linked here: https://www.manufacturedhomepronews.com/wp-content/uploads/2020/11/ManufacturedHousingMarketDataProductionShipmentsComparisonsToConventionalHousingRentalsNationalAssocRealtorsScholasticaGayCororatonMHProNewsInfographic.jpg

25 CFPB, supra note 3, at 26.

26 MHVillage, supra note 4.

27 CFPB, supra note 3, at 26.

28 Id.

29 Id. at 28.

30 Id. at 6.

31 Id. at 37.

32 Id.

33 The prevailing public narrative is that Mr. Buffett sought ought Clayton, but this is subject to dispute. The Berkshire Hathaway acquisition of Clayton Homes for $12.50 a share was met with a shareholder lawsuit. Investors thought the industry had already hit its nadir and was in the process of rebounding, rendering the offer from Berkshire Hathaway too low. It was alleged that a local bank under-valued the company, and that independent advisors pegged the worth between $15.80 and $17.20 a share. It was subsequently alleged that the Claytons’ were “speaking out of both sides of their mouths,” telling Berkshire Hathaway the positive position of both the company and the industry, all-the-while telling investors how bad things were. See Jennifer Reingold, The Ballad of Clayton Homes, Fast Company, Jan 01, 2004, available at https://www.fastcompany.com/48214/ballad-clayton-homes.

34 Financial Times, supra note 6.

35 Id.

36 Id.

37 This quote and variations are found in abundance. It has also been repeated by Clayton CEO and namesake Kevin Clayton on a number of occasions. Mr. Clayton’s reasons for favoring this strategy, and perhaps targeting Berkshire Hathaway (supra note 33) will become clear later in the paper. See Tae Kim, Warren Buffett Believes This Is ‘the Most Important Thing’ to Find in a Business, CNBC, May 7, 2018, available at https://www.cnbc.com/2018/05/07/warren-buffett-believes-this-is-the-most-important-thing-to-find-in-a-business.html.

38 CPFB, supra note 3, at 39.

39 This is taken from the 2014 CFPB report. More recent data is not currently available. Id.

40 A huge debt of gratitude is owed by the author of this paper to the author of the article linked. L. A. “Tony” Kovach, Clayton Homes, Skyline Champion, Cavco Industries, Other Leading HUD Code Manufactured Housing Industry Market Share Data, Jun 24, 2020, MHProNews, available at https://www.manufacturedhomepronews.com/clayton-homes-skyline-champion-cavco-industries-other-leading-hud-code-manufactured-housing-industry-market-share-data/.

41 Id.

42 Id.

43 As Mr. Kovach duly noted, the discrepancies between the market share reported both by Clayton Homes itself, as well as the official figures presented by the Manufactured Housing Institute. This speaks to a level of potential collusion that will be addressed below. [Kovach cited Statistical Surveys, an independent research firm, for the most accurate known market-share data.] Id.

44 See https://www.manufacturedhomepronews.com/manufactured-housing-comparisons-data-sets-vs-existing-and-new-single-family-housing-sales-rvs-auto-facts-potent-insights-for-mh-professionals-investors and https://www.manufacturedhomelivingnews.com/affordable-housing-needed-corporate-corruption-and-manufactured-homes-time-to-get-federal-officials-fully-involved.

45 Jennifer Brown and Kevin Simpson, Mobile Home Parks Move from Mom-and-Pop to Corporate, Sept. 16, 2019, Associated Press, available at https://apnews.com/article/de31aa729f514f48b934bf23ebd3f641.

46 See Figure 1. L. A. “Tony” Kovach, Prima Facie Cases Against Manufactured Housing Institute, Richard A. ‘Dick’ Jennison, Tim Williams, 21st Mortgage, Kevin Clayton, Tom Hodges – Clayton Homes, Et Al, MHProNews, Jan 7, 2020, available at https://www.manufacturedhomepronews.com/masthead/prima-facie-cases-against-manufactured-housing-institute-richard-a-dick-jennison-tim-williams-21st-mortgage-kevin-clayton-tom-hodges-clayton-homes-et-al/.

47 Motley Fool Transcribers, Skyline Champion Corp (SKY) Q3 2020 Earnings Call Transcript, Jan 29, 2020 available at https://www.fool.com/earnings/call-transcripts/2020/01/29/skyline-champion-corp-sky-q3-2020-earnings-call-tr.aspx.

48 MHProNews, supra note 46.

49 It is also worth noting that Cavco Chairman and CEO Joe Stegmayer and Cavco under under investigation by the securities and exchange commission. Source for data may be found supra note 46, information on the Cavco investigation may be retrieved here https://sec.report/Document/0000278166-20-000066/.

50 15 U.S.C. § 2.

51 MHProNews, supra note 40.

52 Id.

[53] Within the ascribed meaning and definition of the Act, “person” includes “corporation.” 15 U.S.C. § 18.

54 It is important to note that it is unclear how the companies in the following footnotes came together, if by merger, acquisition, or some combination of both. MHProNews, supra note 46.

55 Id.

56 Id.

57 Id.

58 Id.

59 Id.

60 Id.

61 Id.

62 Id.

63 Id.

64 MHProNews, supra note 40.

65 This is retrieved from MHProNews, supra note 40, but also corroborated by the CFPB study mentioned, supra note 3 at 14.

66 L. A. “Tony” Kovach, Bridging Gap$, Affordable Housing Solution Yields Higher Pay, More Wealth, But Corrupt, Rigged Billionaire’s Moat is Barrier, MHLivingNews, (article undated), available at https://www.manufacturedhomelivingnews.com/bridging-gap-affordable-housing-solution-yields-higher-pay-more-wealth-but-corrupt-rigged-billionaires-moat-is-barrier/.

67 It would also appear this is a separate violation of 15 U.S.C. § 14 infra note 71. Id.

68 While it is outside the scope of this paper to explore or analyze at length, it has been alleged that this may constitute a predicate offense of the Racketeer Influenced and Corrupt Organizations Act, 18 U.S.C. § 1961.

69 Warrant Buffett, Annual Shareholder Letter, 2015, at 17, Feb. 27, 2016, available at https://www.berkshirehathaway.com/letters/2015ltr.pdf.

70 Moody’s Assesses Vanderbilt Mortgage and Finance, Inc. as ‘Average’ Originator of Residential Conventional Manufactured Home Loans, Feb. 28, 2011, available at https://www.moodys.com/research/Moodys-Assesses-Vanderbilt-Mortgage-and-Finance-Inc-as-Average-Originator–PR_214886.

71 15 U.S.C. § 14.

72 Jefferson Parish Hosp. Dist. No. 2 v. Hyde, 466 U.S. 2.

73 Eastman Kodak Co. v. Image Tech. Servs., 504 U.S. 45.

74 Id. at 462.

75 Id. at 488.

76 Id.

77 Supra note 72, at 8.

78 Id. at 23.

79 Kori Hale, Warren Buffett’s Exploitative Mobile Home Investment, Forbes, Apr. 18, 2019, available at https://www.forbes.com/sites/korihale/2019/04/18/warren-buffets-exploitative-mobile-home-investment/?sh=2c33848b1507.

80 Daniel Wagner & Mike Baker, Warren Buffett’s Mobile Home Empire Preys on the Poor, Center for Public Integrity, Apr. 6, 2015, available at https://publicintegrity.org/inequality-poverty-opportunity/warren-buffetts-mobile-home-empire-preys-on-the-poor/.

81 Wells Fargo & Company (WFC) Top Institutional Holders, Nov. 3, 2020, available at https://finance.yahoo.com/quote/WFC/holders?p=WFC.

82 Theron Mohamed, Warren Buffett’s Berkshire Hathaway Cuts Wells Fargo Stake to 17-year Low, Business Insider, Sep. 7, 2020, available at https://markets.businessinsider.com/news/stocks/warren-buffett-berkshire-hathaway-cuts-wells-fargo-stake-17-years-2020-9-1029566739.

83 Id.

84 Get source.

85 Scott Burns, Americans Love Their Homes – Maybe Too Much, Dallas Morning News, Nov. 13, 2020, available at https://www.dallasnews.com/business/personal-finance/2020/11/13/americans-love-their-homes-maybe-a-little-too-much/.

86 CFPB supra note 3, at 25.

87 CPI, supra note 80.

88 Id.

89 This article cites an interview with Kevin Carroll, a former owner of a Clayton-affiliated dealership who described receiving discounts on his own business loan, which was financed by Clayton Homes, for steering customers to work only with 21st Mortgage. Id.

90 Id.

91 Ninety-nine percent of these loans also had such high interest as to warrant placement in the Federal Government’s “higher-priced mortgage loan” (HPML) status required under 12 U.S.C. § 2801. Id.

92 This figure is highly disputed. Warren Buffett alleged this rate was a mere 3%, but that figure is measuring the total number of failed loans Clayton originated in a single year, not the total number of defaulted loans in the portfolio. See Mike Baker & David Wagner, Buffett’s Mobile-Home Company He Controls Made Record Profits Last Year While Foreclosing on More Than 8,000 Customers, Seattle Times, Feb. 29, 2016, available at https://www.seattletimes.com/seattle-news/times-watchdog/buffetts-mobile-home-empire-makes-record-profits-while-foreclosing-on-8444-homes/.

93 Rothery Storage & Van Co. v. Atlas Van Lines, Inc., 792 F.2d 210.

94 15 U.S.C. § 1.

95 Also note the progressive increase in money spent by the MHI on lobbying efforts after Berkshire Hathaway’s acquisition of Clayton Homes in 2003. Client Profile: Manufactured Housing Institute, Center for Responsive Politics, Nov. 12, 2020, available at https://www.opensecrets.org/federal-lobbying/clients/summary?cycle=2020&id=D000000458.

96 42 U.S.C. § 5401.

97 Id.

98 12 U.S.C. § 4565

99 Gerald Lins, Marie Picard, & Thomas Lemke, Mortgage Backed Securities, 2013.

100 Doug Ryan, Time to End the Monopoly Over Manufactured Housing, American Banker, Feb. 23, 2016, available at https://www.americanbanker.com/opinion/time-to-end-the-monopoly-over-manufactured-housing.

101 Juliet Eilperin, A Once Obscure Office at HUD is the Subject of an Unusually Intense Lobbying Effort, Washington Post, May 1, 2018, available at https://www.washingtonpost.com/politics/a-once-obscure-office-at-hud-is-the-subject-of-unusually-intense-lobbying-effort/2018/04/30/3dfc7ba0-3841-11e8-acd5-35eac230e514_story.html.

102 CPI, supra note 80.

103 CFPB, supra note 28.

105 There is substantial overlap between MHI directors and MHInsider magazine editors. Supra note 4, at 28.

106 Id.

107 Bear in mind that only 14% of loans for manufactured homes are titled as real property, even though a far larger number may be eligible. Id.

108 Id.

109 Id. at 56.

110 Note that, beyond the Chairman and Treasurer, another 5 board seats are held by Big 3 members, with the rest constituted mostly of state-level affiliate directors or REIT representatives. Manufactured Housing Institute, MHI Board of Directors, Nov. 12, 2020, available at https://www.manufacturedhousing.org/board-of-directors/.

111 Supra note 4.

112 Id.

113 U.S. Trademark Application Serial No. 88/497,913 (filed Feb. 7, 2019).

115 MHVillage, supra note 4. See also: https://www.mhvillage.com/pro/print/ for online sources of print editions.

116 Renan Cunha, Manufactured Housing Securitization, Duke Journal of Economics, Oct. 14, 2016, available at https://sites.duke.edu/djepapers/files/2016/10/renan-cunha-dje.pdf.

117 Id. at 6.

118 Eastern Railroad Presidents Conference v. Noerr Motor Freight, Inc., 365 U.S. 127 (1961).

119 United Mine Workers v. Pennington, 381 U.S. 657.

120 Id.

121 Id.

122 California Motor Transport Co. v. Trucking Unlimited, 1971 U.S. LEXIS 1810

123 FTC, Enforcement Perspective on the Noerr-Pennington Doctrine, 2006, available at https://www.ftc.gov/sites/default/files/documents/reports/ftc-staff-report-concerning-enforcement-perspectives-noerr-pennington-doctrine/p013518enfperspectnoerr-penningtondoctrine.pdf.

124 Id. at 4.

125 Id. at 4.

126 Id. at 4.

127 Id. at 22.

128 Id. at 25.

129 Id. at 25.

130 Id. at 25.

131 L. A. “Tony” Kovach, FHFA, GSEs—High Cost to Minorities, All Americans—Due to Asserted Failures to Follow Duty to Serve Affordable Housing, Existing Federal Laws, Manufactured Home Living News, Dec. 11, 2019, available at https://www.manufacturedhomelivingnews.com/fhfa-gses-high-cost-to-minorities-all-americans-due-to-asserted-failures-to-follow-duty-to-serve-affordable-housing-existing-federal-laws/.

###

Note: the graphics, additional statements, and links below are provided by MHLivingNews and were not in the original report by Strommen, above. That noted, these illustrate several of Strommen’s points. For instance, the Doug Ryan CFED/Prosperity Now illustrated quotation and others items below are all added by MHLivingNews.

Additional Information, more MHLivingNews Analysis, and Commentary

One of several marks of good research is that it stands up to scrutiny. Another is that good research stands up to the test of time. A few examples will serve to make the point.

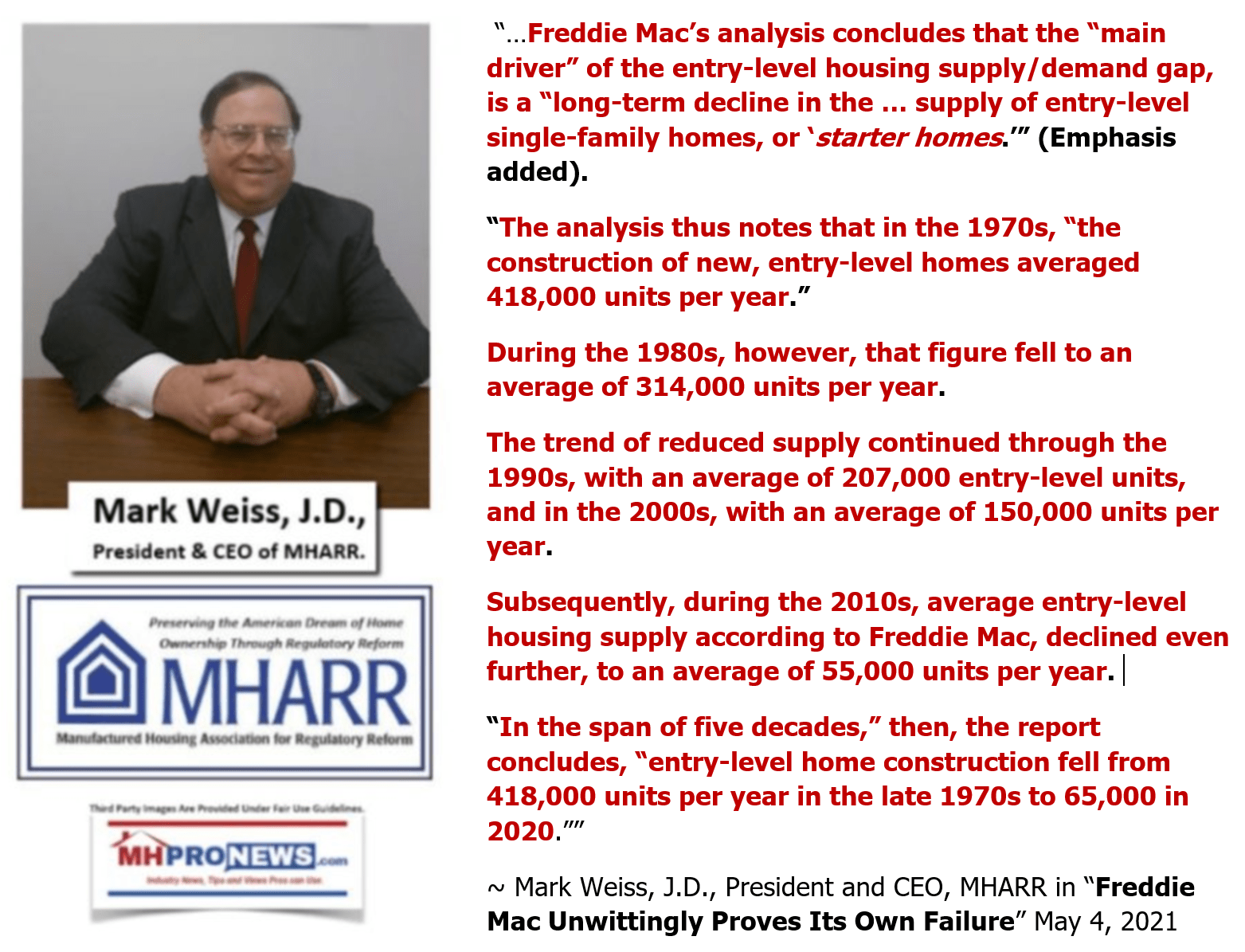

- Strommen did not directly cite Mark Weiss, J.D. Nor did he directly reference in the narrative in his report above the Manufactured Housing Association for Regulatory Reform (MHARR). But as the pull quote above – one of dozens possible like it – exemplifies, Strommen’s observations line up with longtime manufactured housing veteran Weiss’ and MHARR on that GSE topic. Something similar could be said about MHARR’s thinking on HUD and enhanced preemption.

- Strommen did not directly mention James A. “Jim” Schmitz Jr., David Fettig, et al and their Minneapolis Federal Reserve related antitrust research that specifically cites evidence-based examples involving manufactured housing. But what Schmitz and Fettig, or for that matter Strommen each describe, while their respective research stand uniquely apart, they also tend to support each other’s evidence-based allegations that manufactured housing is being “sabotaged.”

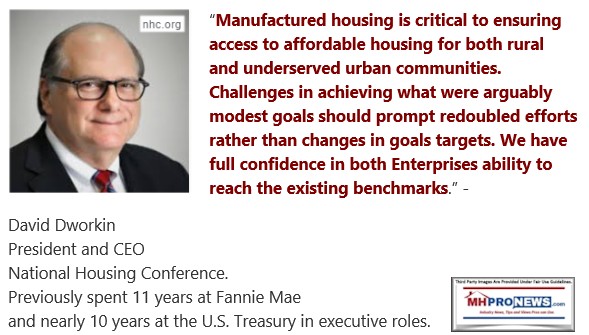

- David Dworkin, President and CEO of the National Housing Conference (NHC), was not directly quoted by Strommen. But that pull quote from Dworkin above also serves to buttress his evidence-based and well reasoned claims.

- Strommen did cite Doug Ryan with CFED which was rebranded later as Prosperity Now. Ryan has attended numbers of MHI meetings. His pull quote and illustrations above certainly line up with Strommen’s thesis. Ryan/Prosperity Now has at times agreed with MHI et al, but at other times has lined up against them.

When Strommen contacted MHProNews about this research project, he stated that he had contacted several industry professionals. Per Strommen, this writer was the only one that responded to his inquiry. Apparently, there is a lack of interest from others who may have ties to MHI to talk about the monopolization of manufactured housing?

It is unclear what sparked Strommen’s initial interest in this topic. That said, his views are supported by others beyond MHLivingNews and/or MHProNews, as those bullets and pull illustrated pull quotes make clear. Robin Harding, a self-declared longtime Buffett admirer explains the moat in a manner that supports Strommen’s contentions. Strommen mentions the Buffett moat method numerous times.

That Buffett point about moats, as Strommen aptly noted, is part of a key concept that is used by Clayton Homes. It has been stated by Kevin Clayton himself.

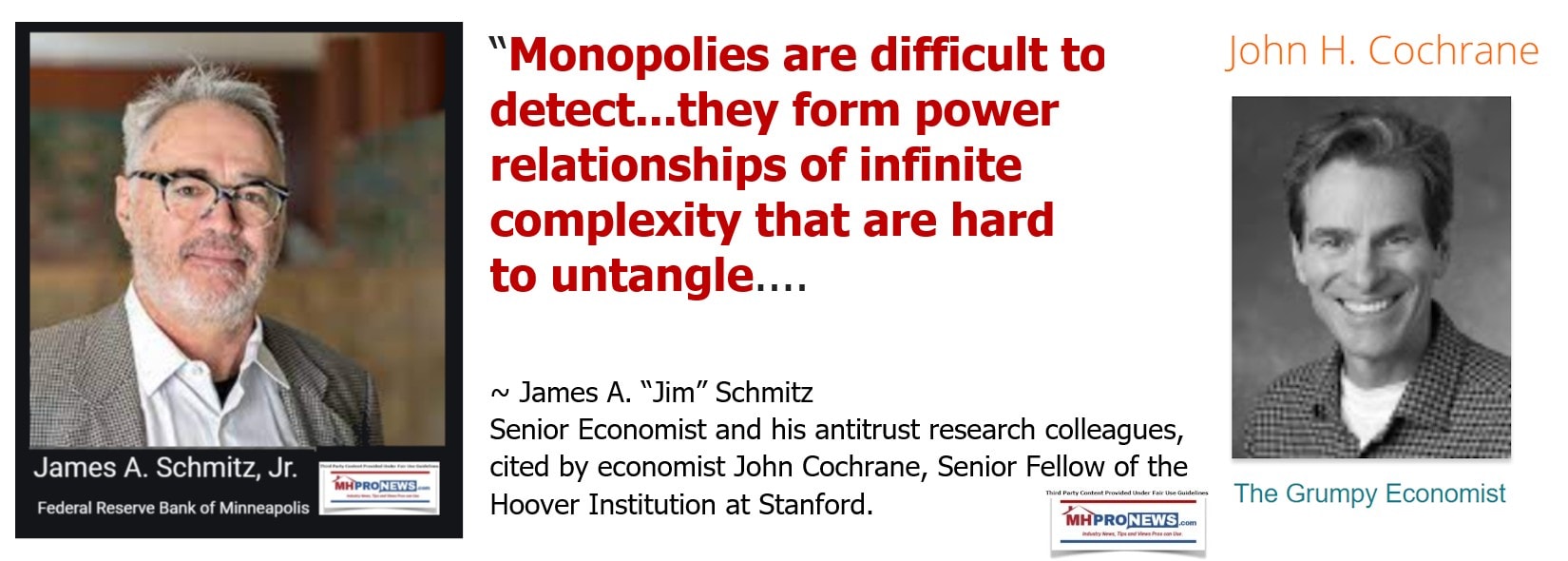

One might wonder. How is it possible to have such a widespread scandal hiding in plain sight? First, it is arguably obscured. It becomes evident only when the relevant facts are pulled together, as Strommen has done. Who says? In part, Schmitz and Fettig who in their independent research said that sabotaging monopolies are complex and are often obscured. Another economist, John H. Cochrane who has studied their research into sabotaging monopoly involving manufactured housing cited this point.

Beyond Schmitz, Fettig, Mark Wright, Cochrane and others involved or who have favorably referenced that research into manufactured housing being ‘sabotaged’ in a manner that has “created the U.S. Housing Crisis,” MHARR’s CEO Weiss cited Freddie Mac’s own data to prove the point from a different direction.

Award-winning Alan Amy, without naming names, generically explains in this video clip posted below that the billionaires are buying up manufactured housing. Amy says it is because manufactured homes are the future of affordable housing.

Numbers of more examples could be given that this issue has been commented on directly and/or obliquely. But to take a different look at how such a widespread scheme to sabotage a market could continue on for years, a simple point can be made. This is not the first time that a ‘hiding in plain sight’ scheme has existed that escaped regulators for years. The sad reality is that the scandals involving manufactured housing, while unique in several respects is not the first or the last example of how much, but not all, in mainstream media and numbers of public officials have ignored the evidence and brewing corporate scandals – often for years. A dozen 21st century examples are shown in the report linked below. When examples of growing and yet long overlooked 21st scandals like Enron, Madoff, and WorldCom are considered, it is absolutely plausible that something sinister can be hiding in plain sight in already misunderstood manufactured housing.

Restated, it is absolutely believable that public officials have ignored and/or missed such scandals because there are a dozen cases cited as examples in the report linked below of often similar or even far greater size and scope.

That quick survey following Strommen’s thesis is sufficient to make the following points and intermediate summary.

In no specific order of importance:

- There are other researchers, inside and outside of manufactured housing, who have made similar claims to those argued in Strommen’s case. Some Strommen cited, others he did not. But in the instances shown, the evidence supports Strommen’s contention.

- MHLivingNews specifically asked other third-party researchers as well as a law professor what their reaction was to Strommen’s case? They routinely felt it was compelling, well evidenced, and thoughtfully presented.

- The harm to thousands of previously profitable businesses and millions of consumers caused by these practices are difficult to understate. Thus, Strommen’s subtitle fits: “A Rube Goldberg Machine of Human Suffering.”

- Thus, Schmitz and his colleagues have made the sabotage monopoly case on manufactured housing along with other aspects of the U.S. economy. While the subject matter of the harm caused by monopoly power, that may work through oligopolies or other methods, is becoming more widely known, it is hardly a secret.

- Both President Donald J. Trump while in office, and the current White House resident Joe Biden have made specific and sometimes extensive remarks on the harm caused by a lack of authentic competition.

- For those who may wonder how something of this size and scope can be hidden, Schmitz, Fettig and Cochrane have explained that is a common feature of such schemes. Additionally, the history of regulators is often sadly one of them missing the mark until a problem was so large as to be difficult to ignore further.

These points are noted for several reasons. First, MHLivingNews/MHProNews has offered several times for Berkshire Hathaway, Clayton Homes, 21st Mortgage Corporation, the Manufactured Housing Institute (MHI) to respond to this legal report. Federal regulators have been asked to respond too. Two of several such examples are linked below.

FHFA has responded, though in an arguably problematic manner. In the case of Berkshire, Clayton, 21st, MHI et al – instead of responding directly themselves – they have instead deployed at various times a surrogate to attempt to make their defense for them. That method has several possible advantages for those who stand accused by Strommen and others. One is that if the surrogate fails, it may not reflect back on them.

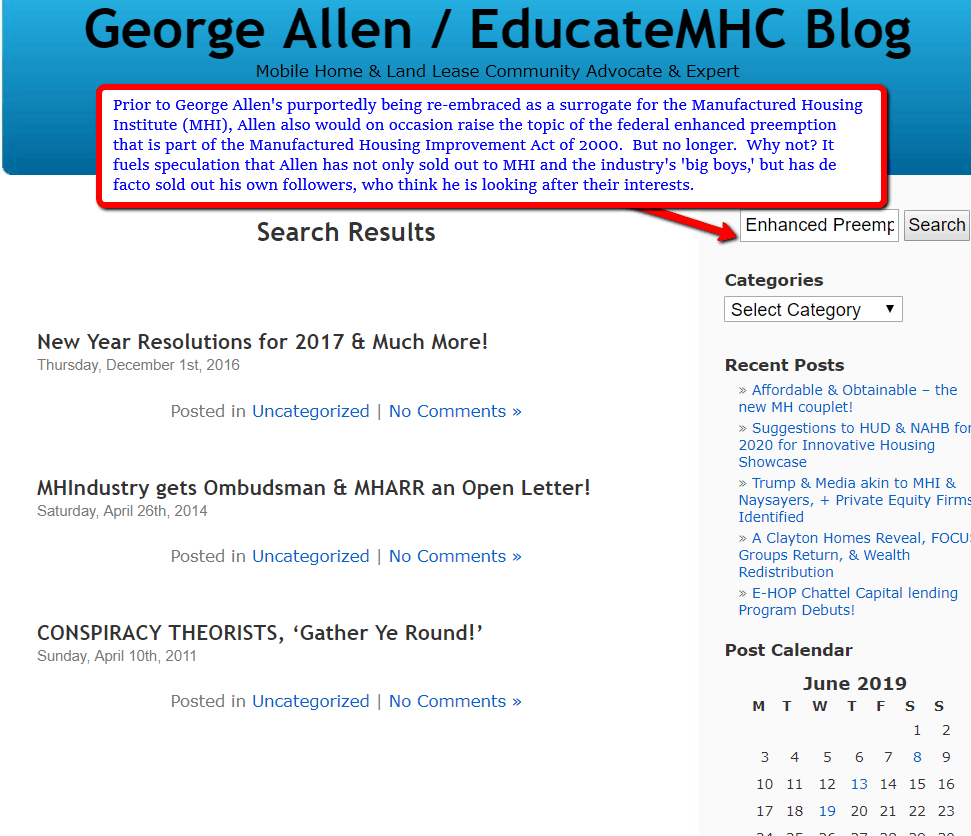

Among the documented part-time surrogates for MHI and their dominating brands is retired Marine officer George F. Allen. Allen has his own credibility issues, which will be explored further below. But let’s first look at how Allen weigh in for them in his own words.

Here below is what Allen said, with the typos in the original. Note that Allen ducks most of the meat of the evidence, and focuses on cheap shots. Allen is reportedly a routine reader of MHProNews, but it took a month for him to publish what follows. Allen uses a method that award winning journalist Sharyl Attkisson has referred to as the smear. He begins by asking, who is Samuel Strommen? Oddly, that question was answered in the original report and is exemplified in the illustrated quotes as shown. Those were published days or weeks before Allen’s missive. Allen, in short, is part of the Rube Goldberg smoke machine that works only on those unwilling or unable to take the time to see the original report and see the facts for themselves. The photo of Allen is not in the original, but was added by MHLivingNews for illustration purposes. It has been used by Allen himself. Allen published this on his blog on March 19, 2021. That’s almost 7 weeks after Strommen’s original was published on MHProNews on February 1, 2021. The illustration below created by MHProNews that clearly references Knudson Law was first posted on February 4, 2021.

II.

II.

Monopolization of the American Manufactured Home Industry

Here’s how the publisher of MHPro News introduced this controversial topic. “Samuel Strommen of the Knudson School of Law (a.k.a. USD Law) provided…(a) copy of his research paper that focused on Warren Buffett-led Berkshire Hathaway, Clayton Homes, their related lending, other Manufactured Housing Institute (‘MHI’) members, MHI itself, and the industry’s Real Estate Investment Trust (‘REITs’) sector.” Who is Samuel Strommen?

Precise title of this typescript? ‘The Monopolization of the American Manufactured Home Industry and the Formation of REITs: a Rube Goldberg Machine of Human Suffering.’

Now, don’t go and get all excited about this 17 page report with its’ ballyhooed 131 footnotes – if you can even find it online. An interesting ‘read’ sure, but not, in my opinion, of academic quality or much use to our industry and realty asset class.

First off, no record of Samuel Strommen being at the Knudson School of Law (a.k.a. USD Law), past or present. So, no idea as to what, if any, academic or manufactured housing credentials this individual possesses. I was thinking professor; now thinking law student, if that.

There’s passing mention of REITs in the report title, plus what you read in the introductory remark above – but no mention, beyond “increasingly consolidating landlords”, (that I read) in the report proper. A near total disconnect! Hint. This awkward wording suggests the identity of the real writer. Otherwise, the phrase would have been better penned as “landlords increasingly consolidating…”

Then there’s this salacious opinion appearing in the four sentences Introduction. “… (manufactured housing) the only form of residence in the United States that carries its’ own pejorative connotation, ‘trailer trash’.” Really? And I (you) should want to read further into this insulting screed?

“The aim of this paper is thus: to expose a number of antitrust violations – both blatant and subtle – in the form of the increasing monopolization of the manufacturing, financing, and the increasingly consolidating landlords, and to call for reforms within this industry.” And that’s pretty much what the writer does, except for NO further mention of, as pointed out earlier, ‘increasingly consolidating landlords’. Wonder why? Though there is mention of “25-30% of all manufactured homes are situated in manufactured home communities (commonly referred to…as ‘trailer parks’).”Called such by whom? Three paragraphs later, the writer refers to this unique, income-producing property type, properly, as a ‘land-lease community’. So, obviously, he has no expertise in the nature and use of manufactured housing trade terminology.

An error? “…production of manufactured homes hit its’ apex (i.e. highest point. GFA) over twenty years ago, with a maximum production of some 375,000 units in 1998.” NOT! That was simply a renascence year for the industry. Its true acme year was 1973 (25 years earlier) when 579,940 new ‘mobile homes’ were shipped nationwide! Perhaps that’s the ‘diff’; ‘mobile homes’ vs. manufactured homes shipped.

Earlier, I made reference to 131 footnotes in this report. Interestingly, the following observation is presented sans documentation: “While claims that Berkshire Hathaway vis-à-vis Clayton Homes have (sic) violated American antitrust law have (sic) not been litigated in court, ample evidence that violations are taking place are myriad.” (‘myriad = 10,000 times’. GFA) What evidence? Where’s ‘the footnote’ when one needs it?

Now here’re some interesting word choices: “What was previously a top ten (manufacturers) has amalgamated (‘consolidated) into a top three. What the industry has presented as apotheosis is closer to apoptosis.” (i.e. from ‘glorified’ to ‘self-destruction’). And this, “In public, Buffett boasted through a rictus (‘gaping grin’) that Clayton and its financing arm were performing a good deed….” These elitist word choices are what lead me to think (maybe) a law student is penning this rough document.

One of the most telling – and to me, helpful, sentences in the entire report, is this: “Clayton Homes (and their affiliated lenders) would suffer a detriment if (the) GSEs were to re-enter the chattel mortgage industry.” Really? And here I believed it was the two GSEs (and FHFA) who were digging in and dragging their heels when it came to implementing aggressive Duty to Serve (‘DTS’) plans and programs in favor of manufactured housing finance. So, which is it?

True or False? “…currently , half of the MHI executive (committee board members) are former employees of Clayton Homes.”

The report ends with the same question I’ve been posing for months. “Why has manufacturing yet to cross the 100,000 unit threshold, much less come anywhere close to its’ most recent 1998 peak?” While I criticize much of the content of the report, I do support this question!

‘A Rube Goldberg of human suffering’ is the subtitle of this research report. Personally, I don’t think the writer, professor, student, or whoever he/she is, addressed this salient point.” ##

— End of Allen’s March 19, 2021 comments on Strommen’s thesis. —

Note: Ironically Allen made a key admission. Why has manufactured

housing not crossed the 100,000 unit threshold? Strommen’s thesis

answers much of that question. Strommen’s linked information, and items

linked or shown herein, answer other aspects of that revealing point.

Unpacking Allen’s MHI and major brand defending/deflecting smear commentary.

As to Allen’s red herring style question: who is Samuel Strommen?

Strommen is hardly a ghost. Allen apparently did not do a proper Google search on Strommen. Nor did Allen apparently engage in journalism 101 by emailing or calling USD’s Knudson Law. A simple call or message would have answered that. It is precisely what our publication did to confirm who Strommen was. It is also how MHProNews determined what his academic colleagues thought of Strommen and his research, which were positive.

What follows is one of several references beyond MHProNews and MHLivingNews to Strommen found online.

Per then South Dakota U.S. Senator John Thune, he had the following entered into the Congressional Record on 8.5.2021

[Congressional Record Volume 155, Number 121 (Wednesday, August 5, 2009)][Senate][Page S8863]From the Congressional Record Online through the Government Publishing Office [www.gpo.gov]

RECOGNIZING SAMUEL STROMMEN

Mr. THUNE. Mr. President, today I recognize Samuel Strommen, an intern in my Rapid City, SD, office, for all of the hard work he has done for me, my staff, and the State of South Dakota over the past several weeks. Sam is a graduate of Stevens High School in Rapid City, SD. Currently he is attending the University of Arizona, where he is majoring in political science. He is a hard worker who has been dedicated to getting the most out of his internship experience. I would like to extend my sincere thanks and appreciation to Sam for all of the fine work he has done and wish him continued success in the years to come. ##

For those who grasp internships with a U.S. Senator, you don’t get the gig, much less public praise like that, unless you have done something right.

But there is more that Allen has apparently missed linked to Strommen beyond MHLivingNews and MHProNews. These appear to be references to this specific thesis.

Habitat Forward: “Sam Strommen with Knudson Law did a research report a few weeks ago on that and related issues.”

Rotary Mornington Peninsula website: “a few favourites to start: Sam Strommen with Knudson Law did a research report a few weeks ago on that and related issues.”

MPO2Play references Strommen and others on these issues regarding monopolization of manufactured housing: “Commentary, Data, moat, castle and moat, sabotaging monopolies, Samuel Sam Strommen Knudson Law, James Schmitz, John Cochrane, Mark Weiss, Lesli Gooch…”

There are others. But those are sufficient to make the point that Allen, who did not post that attempted critique of Strommen on his blog until some 7 weeks after the original report by Strommen was published on MHProNews. Allen clearly missed journalistically sound and obvious opportunities to shed a balanced, accurate, and what essentially becomes a positive light about the credibility of Knudson’s Strommen and his research work.

That noted, and perhaps more important, is that Allen apparently forgot or hopes others won’t recall that he himself has made allegations much like Strommen’s.

Strommen is an apparent industry outsider, who did research on an important topic. By contrast, Allen is an industry insider, who has had a testy-at-times, but long-standing relationship with MHI and their National Communities Council (NCC). Allen has said so himself numerous times.

Here’s what Allen didn’t say in his smear effort to distract from the meat of Strommen’s well-documented contentions.

Thus, once an informed reader or industry professional has the additional details shown and linked herein, Allen’s attack of Strommen falls apart. For those who grasp debating methods, honest and otherwise, Allen has deployed some of the 6 Ds of Duck, Dodge, Dismiss, Distract, Detract, and Defame. These are tactics used when someone has no useful rationale to deploy. Restated, like it or not, realize it or not, Allen’s apparently attempted smear of Strommen serves to instead remind informed readers that he is contradicting himself from days gone by.

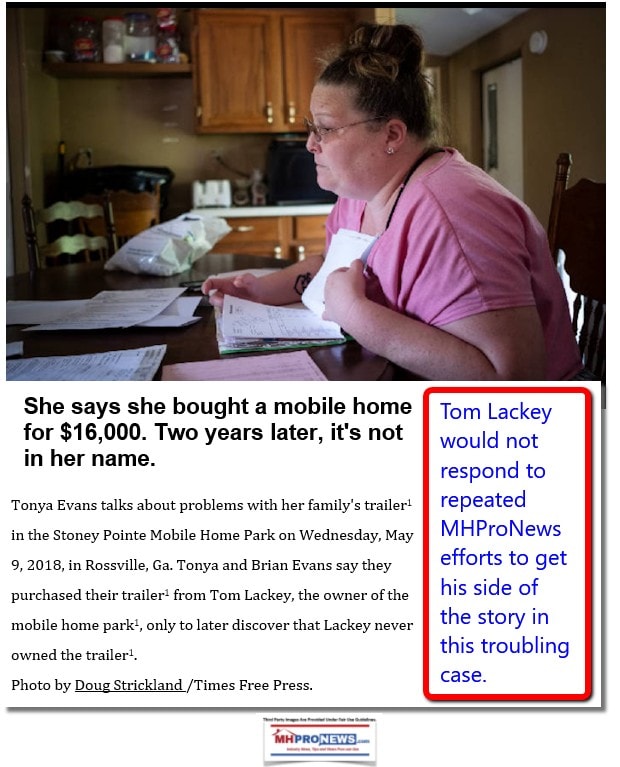

To dot the i and use the Allen method on Allen, it can be noted that he is also a defender of an apparent disciple and colleague of his in group known as SECO. His disciple, Tom Lackey, ran afoul of the legal authorities in Georgia. A mainstream news report documented from the link below Allen’s attempts to defend and deflect from claim of illegal behavior that he himself has ‘taught’ in his ‘classes.’

Speaking of classes, Strommen’s report specifically states it is a research report. One more (cheap) shot-and-a-miss by Allen.

Besides our own contact with Strommen, Knudson Law said they are not allowed to comment on a specific report and its author, such as this one. That noted, off the record, as noted, a law professor indicated that the report is well presented and legally grounded. As was noted above, other attorneys have been engaged on the issues raised by Strommen. Not one thought the report was lacking evidence or sound reason.

Restated, for thinking people able to read-between the lines, Allen has done Strommen a favor. If Allen’s “over the target” reactions on behalf of MHI are the best defense (via attempts at mud-slinging) that MHI can mount on behalf of Clayton, 21st, et al, it is a sadly lacking defense indeed.

But in fairness to Allen, there have been other examples of surrogates for MHI and their dominating brands who periodically attempt something similar. Some examples from 2021 are linked below.

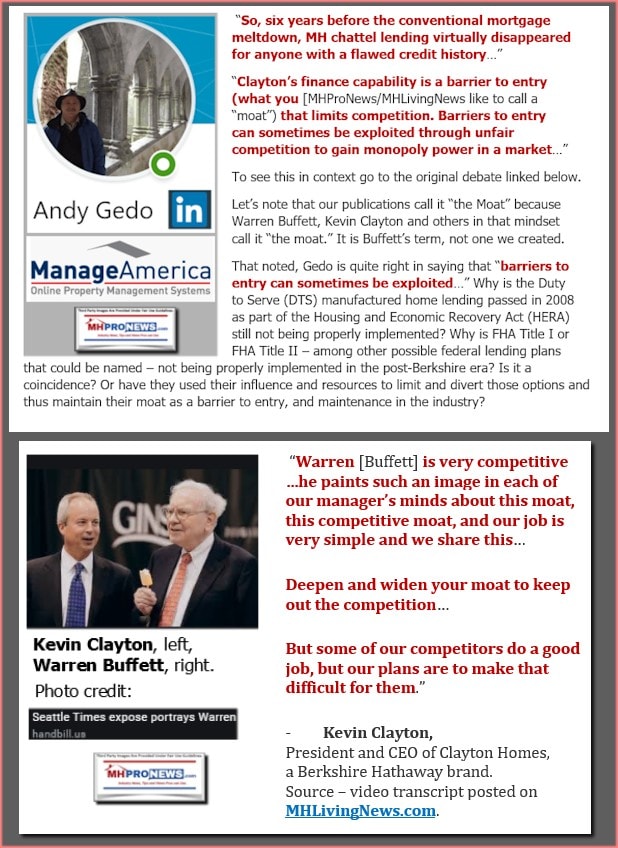

Somewhat in contrast to the above attempts to defend MHI and their major brands is this example. About 2 years prior to Strommen’s sobering case, an apparently more objective supporter of MHI and their dominating brands attempted to debate online concerns like those Strommen cited. Andy Gedo, after making several useful statements and admissions, finally conceded.

Let’s do another interim summary.

- Entirely separate from Strommen are the evidence-based arguments made by James A. Jim Schmitz Jr and David Fettig, and other researchers who have served or still serve at the Minneapolis Federal Reserve. Coming at the issue of the ‘sabotaging’ of manufactured housing from a very different way, their conclusions largely support those of Strommen.

- The defenders of MHI and their dominating brands periodically attempt a 6Ds style of defense. For those who grasp debaters tactics and logical fallacies, when carefully considered in the light of known facts and sound reasoning, their claims fall apart.

- The principles, when directly asked, have not yet attempted a defense.

- As Strommen cited in his report above, the prima facie case for remains effectively unchallenged.

But there are other accusers of MHI, even if they may not all think of themselves as such. Each of these pull quotes illustrates claims that Strommen made.

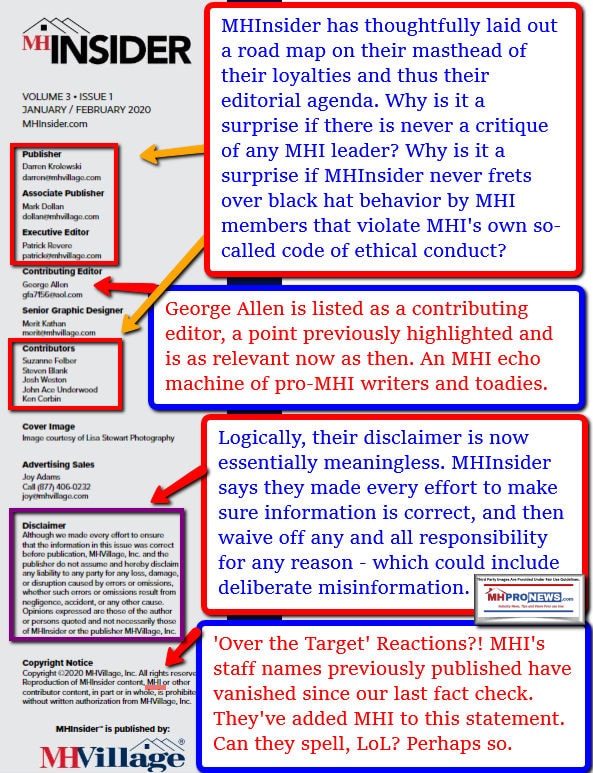

Last but not least about Allen and MHI. As has been documented previously, connecting the dots for Allen as surrogate of MHI is not difficult. In fact, this point was made by Strommen. That MHI has used MHVillage owned MHInsider as a de facto house organ. They are joined at the hip, as the MHInsider masthead below illustrates. Allen himself is listed as a contributing editor.

Now, having dispatched Allen, and the other known contrary arguments presented, let’s pivot back to Strommen’s thesis. Because some of his key claims merit illustration to document his points about the monopolization of U.S. manufactured housing.

As noted, several attorneys versed in antitrust law have told MHProNews that Strommen’s evidence is on point and well-reasoned. Some of the evidence Strommen mentioned will be shown below, albeit it with illustrations to explain to a lay person what it means.

It must be noted that when MHProNews/MHLivingNews began doing such reports exposing the problems inside of our industry a few years ago, MHI supporting brands and MHI itself stopped being a sponsor. Thinly veiled and other threats were made. But ironically, they previously praised our work and the accuracy of our reporting.

It can not be overlooked or go unmentioned that since Strommen’s report, several new developments have occurred. All of them tend to directly support his contentions. Some examples of that are shown below. Included are clear evidence from Warren Buffett and his allies own words that they had in mind to divert financing away from manufactured homes. That’s a key part of this moat method, as Strommen aptly noted.

That pattern of delaying and diverting lower cost and better financing options has several impacts that both harms consumers but also benefits the moat-builders and consolidators. The CFPB, without directly addressing these controversies, issued a recent report that supports the concerns published and linked herein.

Also in the not to be missed category for those who want to understand the role that MHI plans in this scheme is the report linked below. It documents how MHI has once more deliberately misled its own independent members. When asked to respond to these allegations, people like Allen and Ayotte were apparently trotted out. Both of those ‘deflection’ attempts were addressed further above.

Summing Up and Conclusion

Books could be written, and perhaps someday will be, about the consolidation of manufactured housing by apparently unethical and illegal methods. Beyond sources like those shown, there are dozens and dozens of reports and articles that have documented various facets of this vexing picture that Sam Strommen illustrated and unpacked quite well.

MHI surrogate Allen mocked Strommen for not explaining what a Rube Goldberg machine was. That was done for him and those who would not take the 30 seconds needed to Google that colorful and aptly applied phrase’s meaning.

The complexity of the picture is intentional, says Schmitz and his colleagues. It is part of how a conspiracy of this sort can hide in plain sight. Once a few basics are understood, it should be apparent that manufactured housing is wildly underperforming during an affordable housing crisis. That crisis is harming millions, and is costing taxpayers tens of billions annually. Mark Weiss at MHARR, who has been battling these forces from inside the industry for approaching twenty years can sum the issues up via the pull quotes below.

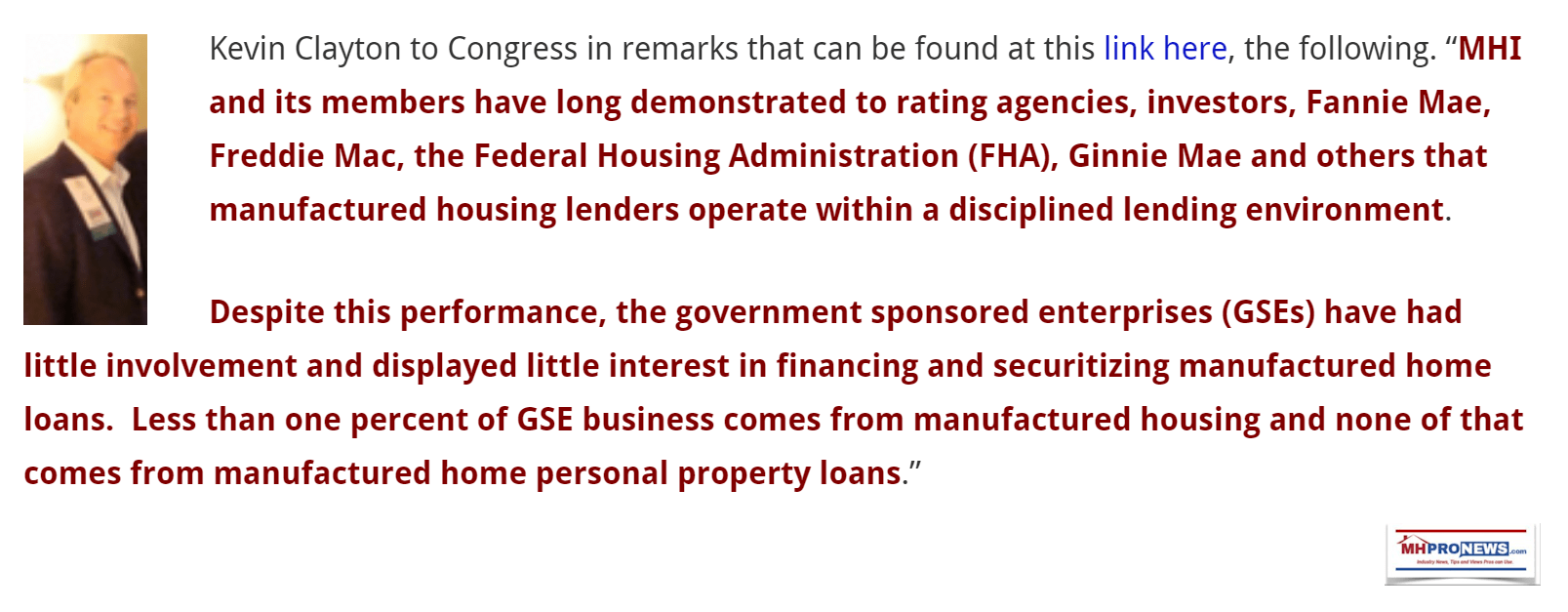

So that it is crystal clear, the facts are largely not in dispute. Kevin Clayton made the point to Congress in these words.

One more summary before the conclusion may place this report by Strommen and others into sharp focus. In no particular order of importance.

- A). There is well documented affordable housing crisis.

- B). The runaway most proven form of affordable housing are HUD Code manufactured homes.

- C). Paradoxically, the Congress has passed the laws necessary to make more affordable manufactured homes available some 13 and 21 years ago. Yes, the laws needed were passed and signed into law by widely bipartisan groups of lawmakers. One bill was signed by a Republican another a Democrat.

- D). On paper, MHI, MHARR, and several state associations are seemingly on the same page. But upon closer examination, the issues raised by Strommen with respect to MHI being part of the problem instead of part of the solution come into focus. The purpose for posturing as opposed to performance by MHI is for the apparent purpose of fostering consolidation.