manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

“June is National Homeownership Month,” said Freddie Mac in a press release to MHLivingNews and other media outlets. “A shortage of affordable housing is making it harder for low- and moderate-income borrowers to buy homes. More than 22 million families have already turned to manufactured housing, and with good reason. Manufactured homes are a viable source for high-quality, modern, sustainable, energy-efficient and affordable homeownership.”

Fannie Mae and Freddie Mac are two independent ‘conventional lending’ giants in the mortgage field. This report will explore research published by Freddie Mac, which says “Freddie Mac is one of the largest investors in mortgage-related securities.”

This video by Freddie Mac celebrates manufactured housing as an important, although misunderstood, housing option.

Freddie Mac said this about some of the ‘common myths’ about manufactured homes.

•  Myth: “They’re unattractive and have limited design options.”

Myth: “They’re unattractive and have limited design options.”

• Fact: Manufactured homes have modern, energy-efficient, high-quality design options and custom home features comparable to site-built homes. They offer floor plans ranging from basic to elaborate, with vaulted or tray ceilings; fully-equipped, state-of-the-art kitchens; walk-in closets; and luxurious bathrooms. Exterior upgrade options include covered porches, higher roof pitch, decks and garages.

• Myth: “Manufactured homes are difficult to finance.”

• Fact: There are plenty of affordable financing options. Show your why manufactured housing is a viable option.

MHLivingNews Fact Check, Analysis and Added Insights

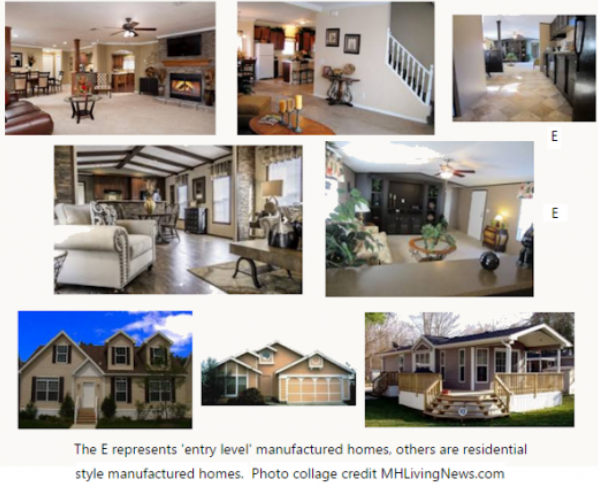

Let’s step back for a few moments from the Freddie Mac statement above and make these experience-based expert observations. There are a range of manufactured homes today.

As the image above reflects, new manufactured homes today range from ‘plain vanilla’ entry level manufactured homes to highly residential style manufactured homes.

Can it be more difficult to finance a manufactured home? Yes, there are times that it is so. In fact, Freddie Mac’s own report linked here makes it clear that only a handful of lenders dominate the manufactured housing lending marketplace. So, while manufactured housing can be financed ‘home only’ as well as ‘land-home’ or with mortgage style financing – the first option not being common with conventional housing – it is misleading if someone thinks that as many banks, finance companies or other lenders loan on manufactured homes.

Those numbers of competing lenders are limited. There are certainly far fewer lenders that finance manufactured housing than conventional housing. The Duty to Serve law was supposed to remedy that fact. Learn more about that in our report linked below.

Additionally, there are these comments and insights from the founding president and CEO of the Manufactured Housing Association for Regulatory Reform (MHARR), Danny Ghorbani, linked below.

That said, there are companies that specialize in manufactured home loans. Sometimes, local banks or finance companies make manufactured home loans, but often not.

· Other good options may be

· FHA (Title I and Title II loans),

· VA,

· USDA (Rural Housing) or

· state agency-based loans.

Note that VA and USDA (Rural Housing) loans can have down payments as low as zero for those who qualify.

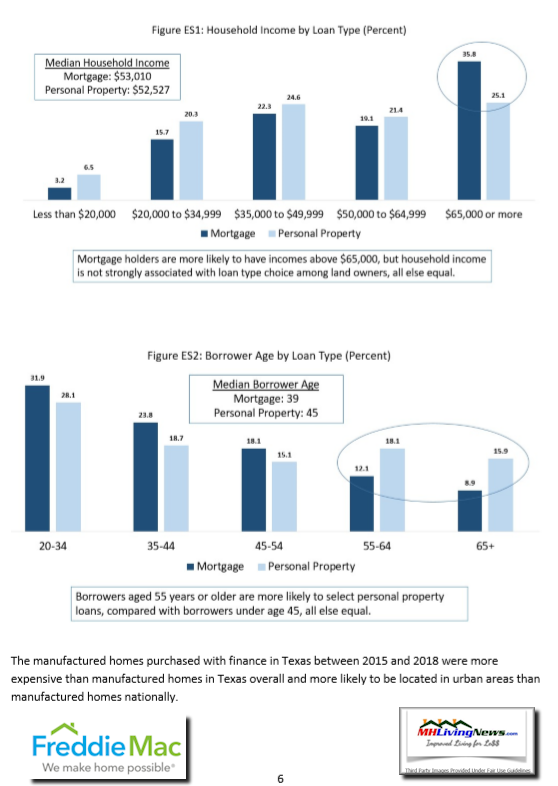

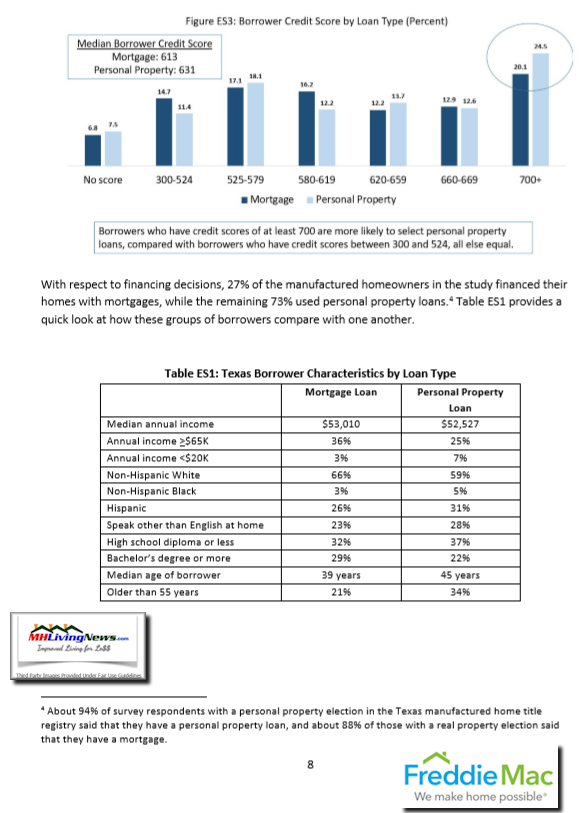

The Freddie Mac report bears more examination, which we may do in the weeks ahead. But a few screen capture from their third-party commissioned research makes it clear that manufactured home owners in Texas, where the study was done, are often college educated.

The graphic below indicates the correlation between credit scores, income, and manufactured home loans by type.

The incomes of Texans who purchased a manufactured home buyers could often support the purchase of a conventional house, but they still chose to buy a manufactured home. Why?

The likely answer is more home for the money, or a newer home for the money. For those who want a ‘greener’ place to call home, manufactured homes are a good option for that reason too. See what the engineer interviewed in the video in the report linked below had to say.

https://www.manufacturedhomelivingnews.com/engineered-homes-egreen-homes-vs-manufactured-homes/

Before you buy any kind of housing, you want to carefully do your homework. Try not to rush a housing decision. Do research on the company you are thinking about buying from.

Frankly, Freddie Mac and Fannie Mae are not doing nearly the lending in manufactured housing that they should be. Who says? The Manufactured Housing Association for Regulatory Reform (MHARR), among others.

Those who do their homework routinely end up as satisfied manufactured homeowners.

As closing thoughts, a few words about personal property – home only or ‘chattel lending’ – vs. mortgage loans. Mortgage loan rates are routinely lower than personal property loans. That said, because closing costs or routinely lower on home-only lending and the amount of money being financed is also routinely lower, the total cost and the monthly payments are both routinely lower for a new manufactured home than a new conventional house of the same size. The difference in price will be substantial. The difference in payment may be smaller, if the loan term is shorter. But the total cost (purchase price plus financing costs) will be less.

“Manufactured homes are distinct from mobile homes, trailers and tiny homes in that they are constructed to meet codes and standards established under the National Manufactured Housing Construction and Safety Standards Act of 1974.” That statement by Freddie Mac is true, but it fails to mention the upgrades to the code from the Manufactured Housing Improvement Act (MHIA) of 2000. Ongoing improvements to manufactured homes are routine, as with conventional housing. Learn more from the report linked below.

Manufactured homes can save time, money, and can be a proven path for building equity and wealth.

There are no perfect forms of housing. But for millions, as Freddie Mac correctly pointed out, manufactured home living has been a fine choice. There are millionaires, even a couple of known billionaires, movie stars, performers and other notables that own or have owned a manufactured home. That alone speaks volumes, doesn’t it?

To learn more about the facts on manufactured home living – the good, the bad, and the ugly – see some of the articles linked below. Or go to the home page or search tool to surf the MHLivingNews website.

That’s it for this installment of “News through the lens of manufactured homes and factory-built housing,” © where “We Provide, You Decide.” © (Affordable housing, manufactured homes, lifestyle news, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.)

(See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHLivingNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com. This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.