manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

MHLivingNews has previously reported that the upward pressure monthly fees on homesites needs an influx of new homesites to mitigate that lack of supply.

This publication has also reported that more competitive financing would make a difference for numbers of current and potential affordable housing seekers and manufactured home owners.

The following is based on what is found on the RV/MH Hall of Fame website.

Ghorbani’s career has spanned over 5 decades. The RV/MH Hall of Fame said of their inductee Ghorbani that the “industry veteran with a background in structural engineering, he served first as chief of design services and then Director of the Supplier Division of the Mobile Homes Manufacturers Association. While in the land development division of MHMA, he is recognized as having, with his team, planned, designed and engineered over 200,000 residential sites for manufactured homes in less than 4 years. He also served as a Vice President of the Manufactured Housing Institute where he was the institute’s marketing representative in U.S. and international markets and he also produced and managed the association’s shows and conventions.

Ghorbani’s career has spanned over 5 decades. The RV/MH Hall of Fame said of their inductee Ghorbani that the “industry veteran with a background in structural engineering, he served first as chief of design services and then Director of the Supplier Division of the Mobile Homes Manufacturers Association. While in the land development division of MHMA, he is recognized as having, with his team, planned, designed and engineered over 200,000 residential sites for manufactured homes in less than 4 years. He also served as a Vice President of the Manufactured Housing Institute where he was the institute’s marketing representative in U.S. and international markets and he also produced and managed the association’s shows and conventions.

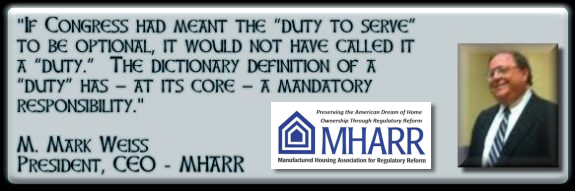

He is recognized as a long time champion of manufactured housing causes on both technical and policy issues. As the CEO of MHARR for the past 20 years, he has been instrumental in leading the way for improvement to the National Manufactured Housing Construction and Safety Act, (known as the HUD code) and was instrumental in the development and passage of the Manufactured Housing Improvement Act of 2000.”

With that context, MHLivingNews now presents the latest Q&A with Danny Ghorbani.

MHProNews Question:

“In our Q&A of March 9, 2020, you indicated that Fannie Mae and Freddie Mac are using various schemes to cover-up and get away with their ongoing evasion of the Duty to Serve (DTS) mandate established by the Housing and Economic Recovery Act of 2008 (HERA) which instructed them in specified ways to serve the HUD Code manufactured housing industry and its consumers. Can you elaborate on the “how and why” of what Fannie and Freddie are doing with respect to DTS?”

Danny Ghorbani Answer:

Danny Ghorbani Answer:

Addressing your question from a Fannie Mae and Freddie Mac decision-making and policy perspective, and without going too deeply into the weeds, the two Enterprises, quite simply, have been able to evade the full and proper implementation of the manufactured housing segment of the Duty to Serve the Underserved Markets (DTS) provision of the Housing and Economic Recovery Act of 2008 (HERA). They have done this — and continue to do so — by employing a series of creative schemes, excuses, delays, dodges and unholy alliances, resulting in ongoing defiance of the DTS law and its clear mandate. And while this is a sad commentary on the effectiveness of the manufactured housing industry’s post-production sector in the Nation’s Capital, as well as a dark chapter in the short history of their federal regulator, the Federal Housing Finance Agency (FHFA), one has to grudgingly admire the devious way in which Fannie and Freddie have gotten away with their ongoing charade. More on this later.

With this background, the basic question you now are asking is: “how and why Fannie and Freddie continue to get away with skirting this federal law and its clear mandate?” The “why” part of your question was mostly answered in our Q& A of March 9, 2020, although there are additional relevant observations later in this Q & A response. But the “how” part of your question is something different and new, which warrants further explanation and elaboration.

Having watched, studied and analyzed the Enterprises’ actions for nearly four decades, and having been involved, engaged-in and instrumental in the drafting and passage of the DTS law, it is my personal opinion that Fannie and Freddie, whether by chance or by design, or a combination of both, have initiated, perfected and ultimately exploited a three-pronged approach to their interpretation, implementation and handling of the DTS law. And when these three approaches overlap, as they have since 2008, they create a platform-of-operation and a comfort zone which allows them to defy the law and its mandate to satisfy their own view of manufactured housing (see, Q & A of March 9, 2020) while, at the same time, richly benefiting their favored clients at the expense of the industry’s small businesses and the moderate and lower income American consumers that they are supposed to serve.

And what are the three prongs of this approach? They are:

1-The Government Sponsored Enterprises (GSEs) of Fannie Mae and Freddie Mac continuing home-financing (particularly chattel financing) discrimination against a class of American consumers who depend on today’s federally regulated manufactured housing (MH) as their principal and, in some cases, only source of homeownership;

2-Fannie’s and Freddie’s utter disregard for the well-established parity between the construction/manufacturing of today’s MH and all other types of single- family dwellings; and

3-The GSEs unholy alliance with — and green lights given to them by — unexpected quarters, which provide them with just enough cover to continue the unacceptable status quo.

Now, let’s delve a bit more into each of these three factors.

1- It is a well-known and long-established fact that the large majority of manufactured home (MH) purchasers are young couples, moderate and lower income consumers and elderly Americans. Fannie and Freddie have and continue to routinely question the credit-worthiness of these groups as an excuse for not securitizing MH loans. And their biggest excuse, of course, is that they do not have any relevant data available to justify their risk-taking in securitizing such loans – and particularly chattel loans. But this is nothing more than a bogus excuse, because they have had twelve years with the best available tools and an army of home-financing experts at their disposal to actually develop such data themselves. For them, this should be an easy task and something that would not take twelve years, with no end in sight. For example, in one of its countless number of comments on the implementation of DTS, the Manufactured Housing Association for Regulatory Reform (MHARR) provided Fannie, Freddie and FHFA with a suggested program that would start with a small but market-significant number of chattel loans which would vigorously be reviewed and evaluated periodically. If the results were satisfactory, they would then gradually increase the number of loans and continue with their close monitoring. Now, if MHARR could formulate a workable approach like this, why can’t Fannie Mae and Freddie Mac? Instead, Fannie and Freddie have wasted twelve years and all they have to show for it are meaningless, miniscule, dead-end “pilot programs” that have discouraged and driven away industry participation, and forced the consumers into very high-rate private chattel loans … something that DTS was supposed to change for the better, but has instead become worse. And if these private companies can earn profits on such high-rate loans, why can’t Fannie and Freddie, at the very least, start one lower-rate loan program, while still earning a profit? For the Enterprises, whose careless and unimaginative programs (remember sub-prime loan programs?) cost American taxpayers trillions of dollars and brought the world economy to near-collapse to worry about high risks and potential defaults on a miniscule number of manufactured housing loans is hypocrisy at best and pure discrimination against some 80% of manufactured home consumers at worst. Given Fannie and Freddie’s checkered history with the manufactured housing industry, one would have to conclude that it is the latter.

2- The DTS law and its mandate are clear, unambiguous and unwavering. Simply stated, with the DTS law Congress told Fannie and Freddie that they have miserably failed to serve the federally-regulated manufactured housing industry and consumers of affordable housing since they were created, and with the DTS mandate, they now have to start serving both — i.e., not site-built, or modular, or sectional, or any other type of single-family dwelling built in compliance with other types of building codes, but today’s quality, well-built and affordable manufactured homes constructed in full compliance with the HUD Code and regulated by the federal government. They must provide securitization programs that would enable finance companies to offer lower-rate loans for manufactured housing AS IS WHEN IT LEAVES THE FACTORY AND IS PURCHASED BY A HOME BUYER…as simple as that. But that is not good enough for Fannie and Freddie as they have decided to re-invent the wheel by demanding that the code and materials be substantially upgraded to the point that the bottom-line price of the home would make it prohibitively costly to the average consumer who would otherwise depend on a manufactured home for his or her homeownership. A very clever way of avoiding the securitization of mainstream manufactured housing loans, right? And to make matters worse, as if they are ashamed of the name “manufactured home,” or in an effort to look down at the product, or in an attempt to confuse homebuyers (or, possibly, a combination of all the above) they, with the help from some within the industry, have invented meaningless and unrelated names such as “High-End Initiative,” “MH Select,” “New Type” of home, “New Generation” of home, “New Class” of home, “Advantage Home,” “Choice Home” and the worst name of all, “Cross-ModTM home!!” (As an aside, the CrossModTM name appears to have been invented by a wannabe individual totally devoid of any and all knowledge, and without the slightest understanding of the rich heritage and history of this great industry…not to mention the difficult and cumbersome evolution that it has endured to get where it is today.) So, Fannie and Freddie must be educated to understand that when a manufactured home leaves the factory with that federal-seal-of-approval affixed to it, it is on par and in full parity with — and, in many cases superior to — any and all other single-family dwellings built to any other building code in the United States of America.

3- One of the main reasons that Fannie and Freddie have been able to yank-around the manufactured housing industry and consumers with a perceived legitimacy for their dodging and evading all these years, is due to their alliance with — and a green light given to them by — a segment of the industry and their regulators (i.e., the Manufactured Housing Institute (MHI) and FHFA).While MHI was a loyal and integral partner with MHARR and the rest of the industry and consumer coalition during the drafting and passage of the DTS law, it went off the reservation (as it did with the landmark Manufactured Housing Improvement Act of 2000 reform law) when it came to the full and proper implementation of the DTS law. I have been around this industry and Washington, DC long enough to know for a fact that Fannie and Freddie would have not been able to do what they have done with this industry and its consumers all these years had it not been for the wink and nod given to Fannie Mae and Freddie Mac by MHI, and their half-hearted support for DTS.

To be sure, and according to the available information, MHI has had its limitations and shortcomings in pulling their punches, often saying one thing publicly, but doing something different privately, going along to get along, as one, or two, or possibly three of their largest conglomerate members are the only companies utilizing Fannie and Freddie’s wild-goose-chase securitization programs — or should I say “pilot programs” or whatever is the name of the latest program that they offer these days.

I am not aware of any small businesses in this industry using a Fannie or Freddie program. Furthermore, MHI’s membership includes two of the largest finance conglomerates that provide higher-rate chattel loans and have no incentive at all to support the full and proper implementation of DTS that would attract competition from smaller companies which would utilize DTS to support lower-rate chattel loans. (Incidentally, here is another major set-back for the post-production sector of the industry when there is no independent, national collective association to represent their views and interests on critical matters such as this.)

As for the green light that FHFA has given to Fannie and Freddie to continue their evasion of and failure to fully and properly implement the DTS law, there are several words that would perfectly describe FHFA’s action or lack thereof prior to the arrival of its current Director, Mark Calabria and his team. Unfortunately, none of those words are pleasant enough to be listed here, thus we’ll spare them. Since Director Calabria’s arrival at FHFA, though, and given the fact that I personally have known and worked with this gentleman for nearly three decades with positive results, I use the word “disappointing” to describe FHFA’s efforts to regulate and fully and properly implement the DTS law. I say this because Director Calabria is a trusted and serious federal government regulator. He and his team have a large reservoir of credibility with our industry, and with me, personally. They were quite helpful and indeed instrumental in the passage of the landmark 2000 reform law. They respect and admire this industry for the quality homes that it builds and the affordable homeownership opportunities it offers to moderate and lower-income consumers. They, along with other relevant agencies, have an aggressive mandate and the full protection of President Trump and Congress to increase and expand the supply of affordable housing for American consumers — a huge undertaking that rightfully must start with affordable HUD Code manufactured housing. Why is it, then, that after nearly two years in charge of FHFA he has not been able to reign-in the renegade Fannie Mae and Freddie Mac, and fully and properly implement the DTS law for the benefit of consumers and the industry’s small businesses? Thus, my disappointment at the continuing green light that FHFA is seemingly providing to these Enterprises along with the perceived legitimacy that allows them to continue with their evasion. Although I don’t hold my breath, it is obvious that drastic decisions must be made by FHFA to end the unacceptable status quo and put the vital DTS mandate back on track.

The proverbial ball is clearly in FHFA’s court, to use its full power and authority to put an end to the nonsense and evasion that Fannie and Freddie have gotten away with for 12-plus years (and counting) regarding DTS.

##

Supporting Evidence?

The reply to the question posed by MHLivingNews is that of Danny Ghorbani. Objective thinkers should ask themselves, is there evidence for Ghorbani’s assertions?

The short answer is yes. Just a few examples will serve to prove that point.

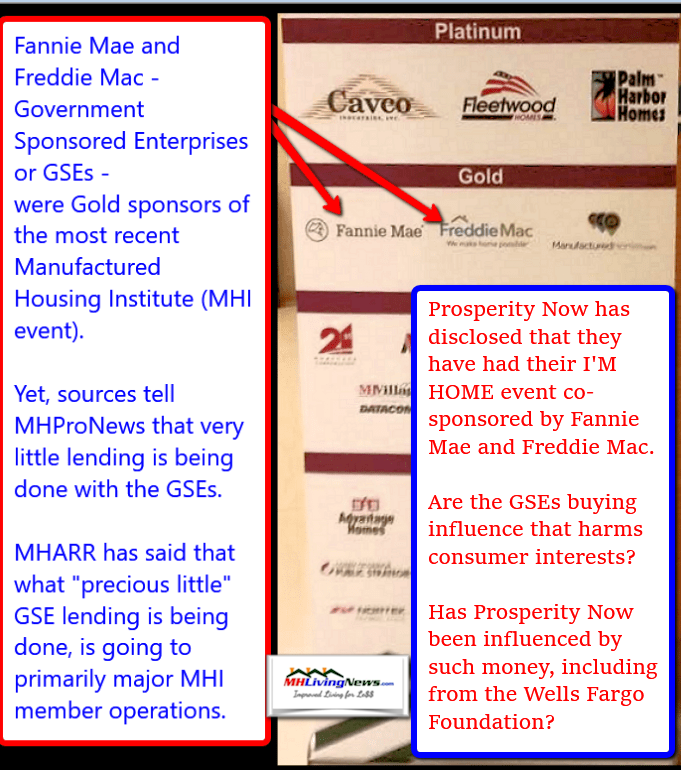

- Fannie, Freddie, MHI and a others involved have refused to release the minutes of closed door discussions that resulted in the “new class of homes” that was dubbed in 2019 as “CrossModTM homes” by MHI.

- David Dworkin, President and CEO of the National Housing Conference said in formal comments to the federal government the following, which was quite in keeping with Ghorbani’s assertion. It should be noted that Dworkin served as a vice president for a GSE, so one might presume that he knew what he was talking about. Furthermore, Dworkin arguably did a better job of arguing for more from the GSEs than MHI’s Lesli Gooch did, see that comparison of their respective remarks at the link here.

- MHI has had as event sponsors Fannie Mae and Freddie Mac. That smacks of collusion that points to the very concerns raised by Ghorbani in his response. After all, why would Fannie and Freddie need to sponsor MHI to curry favor, if the GSEs were sincere in their intention of robustly supporting all HUD Code manufactured homes?

- MHProNews and MHLivingNews has done several reports that all tend to support the concerns raised by Ghorbani.

- Donna Feir, Ph.D., and research economist studied this issue and was troubled by what she found, citing the Seattle Times expose that pointed a finger at Clayton Homes and their associated Berkshire Hathaway lenders of Vanderbilt Mortgage and Finance (VMF) and 21st Mortgage Corporation.

- There is a prima facie case to be made that since Triad Financial Services, Credit Human and other lower rate manufactured housing “home only,” personal property or chattel loan lenders are successfully making such loans at lower rates that 21st or VMF. Years of sustained lending by Triad and Credit Human – who have reportedly provided the GSEs with their data – is sufficient evidence for Fannie and Freddie to issue and securitize the loans that DTS mandates.

Those are sufficient examples to make Ghorbani’s statements come to life. It should be noted that Ghorbani – as is true of others quoted, interviewed or otherwise cited here and on MHProNews – had no idea of what our analysis of his comments would be. He’ll be reading these words for the first time along with thousands of other industry professionals.

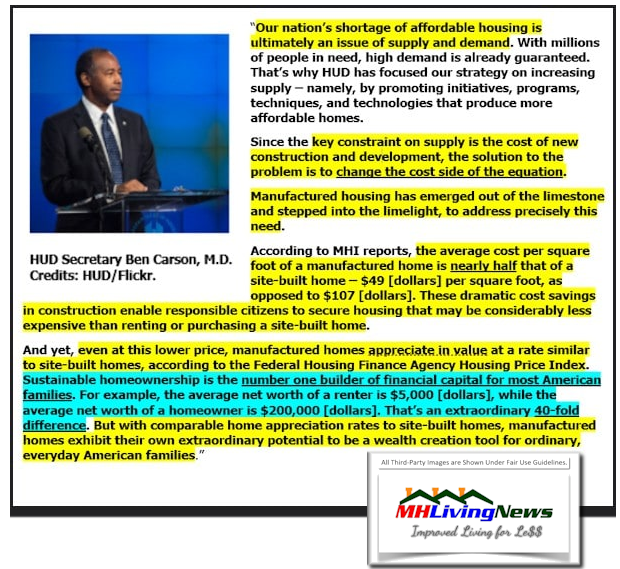

The above supports the statements made by HUD Secretary Carson as well.

The industry is struggling from what several sources say are forces inside manufactured housing that have thwarted good laws that already exist. More on that is found in the linked reports that follow the byline and notices. Ghorbani and the Manufactured Housing Association for Regulatory Reform has been a consistent leader in that fight for the full and proper implementation of good laws that exist in good measure to the work he and his colleagues have done over the years.

Consumers who have experienced manufactured homes routinely like or love their homes. It is tragic that so much evidence exists that much of the industry’s problems arguably originate from corrupt practices within the industry.

By exposing what is wrong and focusing on what is right the evolution of the solution could achieve its ultimate success. “We Provide, You Decide.” © (Affordable housing, manufactured homes, lifestyle news, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.)

(See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHLivingNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com. This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.