manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

Let’s begin with what will be to some a surprising point. Not everyone is ready for homeownership. Renting is useful for some, in specific circumstances, at least for a given period of time.

That said, as a rule-of-thumb, anytime someone can own a home, it is wise to do so.

Why?

Because whether you rent the house or are buying it, you are paying someone to own it. Since you are paying for it, that ‘someone’ might as well be you.

One more thought before diving into the what it takes to get a loan insights.

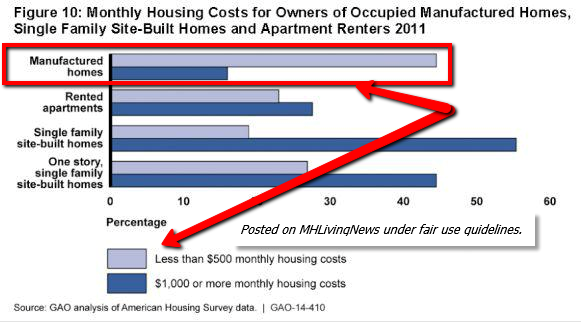

If you are buying an existing house, one that is previously owned, and especially one that’s a number of years old, you must think in terms of maintenance and upkeep. The older the house, the more likely there will be repair costs coming. An advantage to buying a new manufactured home is that it is new, comes with a warranty, saves you money up front, saves on utilities over millions of existing homes, and for several years you can expect to have low-to-no maintenance costs.

With those facts in mind, let’s dive into the main elements of getting a home loan.

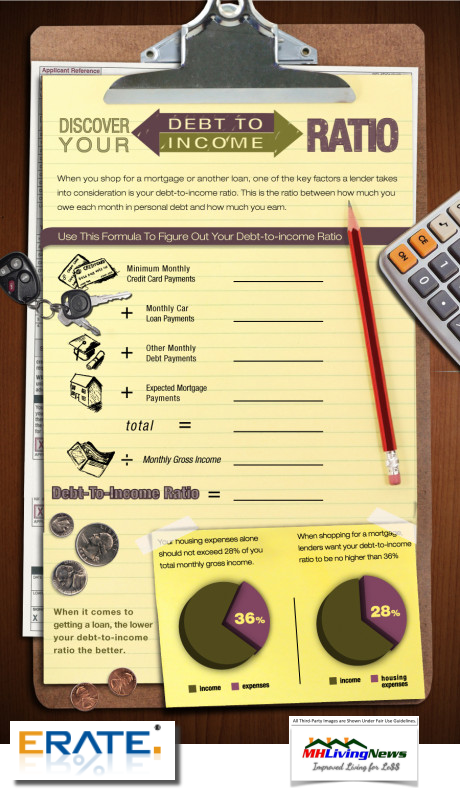

Key Elements to Financing a Home – Income, Debt-to-Income, FICO and Down Payments

Whether you rent or buy, you have a move in cost – think of that move-in-money like a ‘down payment’ – and monthly payments. Depending on the lender, loan type, location, and credit score – the down payment on a loan can be from zero to 20 percent or more.

Your DTI – Debt to Income Ratio – can be thought of as the Housing DTI and the Total DTI.

Note that Housing DTI is sometimes called “Front-end DTI,” while the total DTI is sometimes referred to as “Back-end DTI.”

Housing Ratio or “Front-End Ratio” Includes

A lender will add up your estimated monthly payment on a residence, along with all the other direct costs associated with that home. Those direct costs of housing DTI usually include the following items:

- Site fees in a land-lease community, land/Improvements costs (if new construction) and/or HOA (Home Owners Association) fees. Plus,

- property taxes,

- mortgage insurance, and

- homeowner’s insurance.

Total Debt Ratio or “Back-End Ratio” Includes

Beyond the Housing DTI, a lender will calcuate all of your other monthly commitments. Beyond the housing DTI, there are:

- monthly credit card payments,

- car payments,

- estimated utilities,

- student loan payments,

- alimony,

- child support, etc.

According to Zillow, with the following types of loans, a borrower must be at or below these DTI levels in order to qualify for a loan.

- FHA limits are currently 31/43, though these can be higher with justification from the lender.

- VA limits are only calculated with one DTI of 41.

- USDA – also known as Rural Development – loan limits are 29/41.

Understanding the Elements of a Credit or FICO Score

The FICO score is virtually synonymous with your credit score. The term FICO is an acronym for Fair Isaac Corporation, which says it was the first company to offer a credit-risk model with a score. The term FICO is so common that its become like the word Xerox or Kleenex, the brand names for copy machines or tissues.

The FICO score is important-to-essential in obtaining financing on a manufactured home, or any other kind of housing loan made by a conventional or government backed loan. There are other kinds of loans in manufactured housing, with a very common one being the ‘chattel,’ personal-property or ‘home-only’ loan. While home-only loans are usually at a higher interest rate, because the cost of a manufactured home is so much lower, the overall cost for owning a manufactured home is still generally less expensive than renting or any other kind of permeant housing purchase.

The CNBC infographic gives you a good sense of the elements of building a good credit score.

We’re including a video with some manufactured home lenders, for a very specific reason. Two of the lenders in this video talk about how surprised and impressed they are with the qualify of manufactured homes.

The more you know, the more likely you are to see why HUD Secretary Ben Carson said that modern manufactured homes are “amazing.” ## (Home buying and financing tips, news, analysis and commentary.)

Related Report:

How Can You Avoid the “Hidden Costs” of Buying A House? Just the Facts!

(Third party images, content, are provided under fair use guidelines.)

By L. A. “Tony” Kovach, publisher, industry expert, and consultant.

By L. A. “Tony” Kovach, publisher, industry expert, and consultant.

Tony is the award-winning managing member of LifeStyle Factory Homes, LLC, the parent company to MHLivingNews and MHProNews.com.