manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

Here’s a riddle for you.

Why would a federal agency and a nonprofit think tank, both dedicated to consumer protection, choose to pursue a course that is diametrically opposed to their mutual mission?

The Center for Enterprise Development (CFED) and the Consumer Financial Protection Bureau (CFPB) have staunchly supported manufactured housing as an important component of affordable housing for low- to moderate-income families.

Yet both have just as vigorously joined forces to oppose proposed reforms to the Dodd-Frank Act that would remove obstacles to manufactured home ownership for millions of Americans in these income brackets.

To borrow from Winston Churchill: It is a riddle wrapped in a mystery inside an enigma, but perhaps there is a key. That key may be conflict of interest.

It is perhaps the most rational explanation for an apparently willful disregard of known facts displayed by both organizations. It might also address the curious alternate universe CFED and some others inhabit, in which manufactured homes are revered, but the people who manufacture, sell and facilitate their purchase are the subject of an almost pathological hatred.

How do we know this?

We know the two have a favorable view of manufactured homes, from the CFED website and from the white paper CFPB produced in 2014.

Yet that same white paper demonized the MH industry, as has CFED’s Doug Ryan, a visible nonprofit mouthpiece on manufactured housing (MH).

A Matter of Greed?

In April, not long before the U.S. House of Representatives was to vote on the Dodd-Frank MH reforms, Ryan penned a blog for Rooflines under the headline: Article Reveals Manufactured Housing Industry’s Greed.

Ryan is a passionate voice, who indeed favors MH as a housing option; but the argument he advanced is that manufactured home loans that bear higher interest rates are “predatory,” and that this type of lending caused the mortgage meltdown of 2008.

To support this startling historic revisionism, Ryan points to the article cited in the headline, published by The Seattle Times in conjunction with the Center for Public Integrity.

The story, which is little more than a muddled takedown piece designed to paint Warren Buffett, his conglomerate, Berkshire Hathaway, and its MH subsidiaries, Clayton Homes and related lenders, as latter-day robber barons picking the carcasses of the poor.

In their zeal to relieve the leading emperors of MH of their clothes, the reporters displayed a tendency to mix apples with oranges and failed to grasp the most fundamental nuances of the MH industry or its financing.

The reporters might be excused for failing to do their homework — and for failing to disclose the fact that the sister of one of them is a lawyer whose clients are suing Clayton Homes, the focus of their piece.

![]()

Nor were they inclined to consider information from multiple sources — much of it brought to their attention by MHLivingNews, that attempted to set the record straight:

Fact: The MH industry and its lending practices had exactly zero to do with the sub-prime mortgage crisis that led to the housing meltdown of 2008.

Fact: Manufactured housing was never meant to be adversely impacted by the Dodd-Frank Act. Rep. Barney Frank, the co-sponsor of the legislation, said as much in a letter, now part of the congressional record.

Fact: The call for reform of Dodd-Frank is industry-wide and affects far more than Berkshire-Hathaway affiliates. Current CFPB regulations arguably impacts the entire MH industry.

Fact: Lenders are leaving the MH market due to the Dodd-Frank rules and those who remain often refuse to make loans under $20,000, citing the cost of origination and regulations, which makes loans under 20K unprofitable.

Fact: The inability to secure financing is driving down lower-cost MH values, leaving homeowners underwater — the same as happened in the site-built housing market.

Fact: Buyers with reasonable to good credit scores who are trying to purchase modest homes under that $20,000 threshold are being forced into personal, unsecured loans for as much as 36 percent interest.

When asked to comment on the information provided, The Seattle Times reporter responded with silence.

CFED’s Ryan, on the other hand, had already received substantial private tutoring on the fine points of MH financing from industry experts eager to educate the “pro-consumer” opposition about the real-life impact of the Dodd-Frank provisions they were seeking to reform.

MHLivingNews similarly asked Ryan for comment on the above facts and reports. The reply?

Silence.

Nor were we able to secure comment on the story of Eric Powell, a Louisiana man who fell victim to the unintended consequences of Dodd-Frank and was forced to choose between a 36-percent interest rate on a $9,500 personal loan — or give up his dream of home ownership.

What Powell’s story revealed is the stark reality that he, and those like him, face the choice of paying far higher interest rates to a non-MH lender, or of going on as renters. The Ryan/CFED plan for CFPB — the federal rule-maker — to stay the course, thus denies ownership opportunities in the name of defending Dodd-Frank, even when the reality of Powell and others clearly demonstrate their arguments are flawed.

CFPB policy impacts the value of perhaps 1.7 million (+/-) owners of pre-owned manufactured homes that might sell on financing terms under $20,000. Thus, CFED’s policy of lobbying Congress and the CFPB to make no changes in the law harms the very low-to-moderate income home owners the nonprofit group claims to champion as their alleged MH consumer advocate.

Further, it is precisely the lack of lending that harms resale values that The Seattle Times, et al argued was bad for manufactured homeowners. They fail to see the fact that conventional housing crashed like a rock when lending tightened in the wake of the 2008 housing/mortgage crisis. There are still millions with underwater conventional housing loans.

So why don’t Ryan and CFED admit their errors and support bi-partisan and industry-supported efforts to reform Dodd-Frank?

The Conflict

Perhaps the answer is found in the fact that CFED is receiving money from the CFPB and the federal government to develop educational programs. The question is: How much?

While admitting to MHLivingNews that CFED receives funds from CFPB and the federal government, Ryan denied the money had any influence on him or the organization’s lobbying activities.

Ryan would not provide details, stating the information was available in CFED’s annual reports and the nonprofit’s Form 990.

However, these did not supply a breakout of government versus non-government funds, or for what programs and purposes these grants and contracts – collectively totaling millions of dollars – were made. Repeated requests for specifics were dodged, and the specifics of how much, from which sources have gone unanswered.

If there is nothing to hide, why are Ryan and CFED hiding it? This is supposed to be public information, readily available upon request.

Contacts at CFPB, the federal agency, were also asked about this topic. At first, their response indicated they would provide the information sought.

Then, after follow ups, more silence. No data was given, no more replies. One of the original CFPB staff members contacted by MHLivingNews has since left the organization, according to an auto-response on that staffer’s previous CFPB email address.

It Stinks, But It’s Legal?

Let’s be clear that non-profit experts MHLivingNews contacted about this issue agree that, based on what we know at this time, CFED has likely not violated any laws. Ryan stated the same.

Let’s also be clear that, while federal tax laws allow nonprofits to engage in some legislative lobbying activities, there are spending limits to ensure that “no substantial part of the activities” may be used for “carrying on propaganda, or otherwise attempting, to influence legislation.”

According to its most recent federal tax return, CFED appears to be skating below the dollar ceiling in terms of what IRS defines as “significant” lobbying expenditures.

But that doesn’t change the fact that the nonprofit is lobbying Congress and the CFPB, when as much as a third or more of its income comes from the federal government. It stinks of conflict of interest, one non-profit expert told us, but it is likely not illegal.

Can You Spell Ironic?

Ryan has routinely demanded more and more data from industry lenders. But when the shoe is on the other foot, and information is being requested from CFED that may reveal a motive as to why they are fighting so hard to stop Dodd-Frank reforms that demonstrably would benefit MH owners and potential buyers — silence? Is that irony, hubris, embarrassment?

Or might the key to this riddle be conflict of interest?

There seems enough of that to go around — from the reporter whose lawyer/sister is suing the Warren Buffett affiliated MH company he has cast in unflattering light, to the nonprofit that receives federal money and then lobbies federal law- and policy-makers.

And then there is CFPB — the agency created by the Dodd-Frank act and empowered by that same law with the unprecedented ability to create rules and regulations without congressional oversight.

The reforms sought by the MH industry — which was never meant to be so impacted by Dodd-Frank in the first place — call for a re-evaluation of the agency’s unfettered powers, and the approval of Congress.

Small wonder the Consumer Financial Protection Bureau is not fond of the proposed Dodd-Frank reforms. Things are fine and dandy for them just the way they are.

The True Advocates for MH Home Owners?

Upon close inspection, both CFED’s and CFPB’s mantle as so-called “consumer advocates” is as tattered as their arguments opposing reasonable changes to Dodd-Frank sought by manufactured housing lenders and others in the industry.

It seems that the true advocates for an estimated 1.7 million households — the buyers and sellers in the below-$20,000 price range — are the MH associations and companies, along with these noteworthy groups:

National Association of Realtors, Mortgage Bankers Association, National Organization of African Americans in Housing, National Association of Federal Credit Unions, national Association of Mortgage Bankers (NAMB), National Association of Mortgage Professionals, and the California Association of Mortgage Professionals.

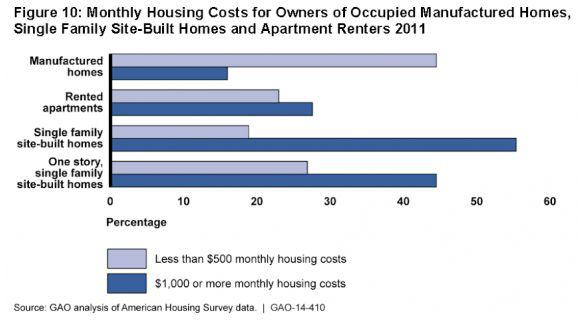

As we’ve reported numerous times, the math for manufactured homes is pretty simple: How much down and how much a month?

When those payments on MH are often less than rent, as the Government Accounting Office (GAO) report published last summer demonstrated, why deny the free market opportunities to create home ownership made possible by good businesses willing to risk their own money?

Private MH lenders are loaning money when the ability to repay has been demonstrated. Where is the threat to consumer interests in saving buyers money vs. renting with no hope of equity?

Eric Powell’s story reveals that those leading the fighting to reform Dodd-Frank are doing so to achieve just what the bill’s name states; The Preserving Access to Manufactured Housing Act (S 682/HR 650).

Had Powell not been able to secure financing to buy his modest home, his monthly rent payments would have been double what it ultimately cost him to enter the realm of MH homeownership.

That’s true even at interest rates higher than CFED and its federal partner like. Perhaps the next riddle is will CFPB and CFED change course and support industry sought changes that are good for consumers in light of these facts? ##

Disclosure

It should be noted that our sister publication, MHProNews, has received modest advertising revenues from industry companies and lenders, including 21st Mortgage. But the bulk of our parent operation’s revenues are from non-ad services. Our position on these issues has been consistent and fact-based — and are pro-consumer and pro-business.

References, Sources and Footnotes

- Dodd-Frank and Manufactured Home Financing – the Place where Good Intentions and Unintended Consequences Collide, linked here. The article demonstrates that MH lenders are about 2/3 lower in interest rate than the kind of financing Eric Powell was forced into, due to policies supported CFED and enforced by the CFPB. The nuances of MH lending are reviewed in terms that make sense, and which undercut the false arguments advanced by Doug Ryan et al. MH lending experts are quoted in this article, as is Doug Ryan.

2) Don Glisson Jr., Chairman and CEO of Triad Financial Services, on his company’s experiences and reasons for supporting reforms of the Dodd-Frank Act to correct problems created for manufactured housing lending by current CFPB policies., linked here.

- Sam Landy, JD, UMH Properties CEO, and other lenders who have been pushed out of the market by current CFPB policies. It is noteworthy that the facts Landy and others present undercut Doug Ryan led CFED arguments and vividly proves that CFPB polices are costing untold thousands annually access to home ownership. See article and video, linked here. It must be noted that ManufacturedHomeLivingNews has contacted every major and some regional MH lenders. All favor changes to current CFPB regulations, so this is not a Berkshire-Hathaway/Warren Buffett issue.

4) Alan Amy, a veteran MH retailer, estimates that current regulations are depressing MH sales by about 30% a year. If so, the practical impact is that 20,000 more homes could be sold a year at the current pace and 20,000 new good-pay jobs” that would otherwise be created in the construction of manufactured housing. Amy’s comment came as part of a broader video interview, linked here.

5) The Integrity of Clayton Homes and the Politics of “Investigative Journalism,” published by Professor Lawrence A. Cunningham, JD. Cunningham’s arguments have yet to refuted by The Seattle Times et al. Article linked here.

6)One must also question why Daniel Wagner and Mike Baker, writing in the Seattle Times articles done in tandem with the Center for Public Integrity, used outdated and inaccurate terminology when referencing modern manufactured homes, improperly calling them ‘mobile homes.’ For a better understanding of the terminology and why-it-matters, see the article linked below.

Evolutionary! From Trailer House to Mobile Home to Today’s Manufactured Home

###