manufacturedhomelivingnews.com Manufactured Home Living News

manufacturedhomelivingnews.com Manufactured Home Living News

Complex problems cited in the headline can be simplified by making this specific point. Affordable housing and income or wealth inequality are in several ways related issues. Home ownership is the most common form of wealth building in America. There are already good laws ‘on the books’ that make more affordable housing available. There are also good laws that make the financing of affordable housing more available.

If that is so – and that claim will be demonstrated in this article – then why is there an affordable housing crisis? Why has income or wealth inequality become so pronounced?

That can be explained with this snapshot too.

Good laws that MHLivingNews will examine and explain below have been largely sidelined and have gone under-enforced. That lack of enforcement of good laws has in turn resulted in increased housing costs and an in increased wealth inequality.

Because affordable housing has been limited, and homeownership opportunities have been unjustly limited, those that offer rental or other housing are paying more than would normally be the case. It is the law of supply and demand at work, but in a manner that allows a relatively few well-connected businesses in various markets to behave in increasingly problematic ways. Why? Because when supply has been limited, those that have housing assets can behave in more aggressive or so-called ‘predatory’ ways. If there were more supply, the opportunity to behave badly would be more limited by the marketplace.

Because a relatively small number of firms have been allowed to get away with such behavior for a time, they have profited more in the short run than they normally would have had their been more competition.

Summed up, applying a phrase used by political figures on both sides of the left-right divide have said, “the system is rigged.”

That snapshot, less than 330 words, provides the foundation for what follows. As we lay out the evidence and the details, keep good existing laws in mind as the solution.

The reason that applying good existing laws is useful is that good laws need to be brought to bear. Passing new laws takes time, and may or may not occur. Enforcing existing laws can be far more rapid.

Affordable Housing and Wealth Building…

HUD Secretary Ben Carson, M.D., has said several times the following. The average renting household has some $5000 in net worth. The typical homeowning family has an average net worth of some $200,000.

HUD Secretary Carson is hardly the first to make that kind of observation, but his raising the profile of the issue is useful. More home sustainable, affordable homeownership is a good idea. Several social benefits flow from homeownership, as factory-built homeowner the Reverend Donald Tye, Jr. – who is also an actively retired business professional – has explained.

Manufactured homes are the most proven form of affordable housing in America today, and have been for decades. They are also widely misunderstood. Let’s note that lawmakers on both sides of the political divide who have studied the industry have praised manufactured housing, and have done the research that demonstrates that it is the most proven form of affordable housing.

As to misunderstandings about manufactured homes, MHLivingNews has for years published articles and videos that are educational in nature. We have routinely cited third-party research and third-party comments by people who know that has debunked the key concerns. For example.

Two links, above and below, provide some illustrations of the volumes of research that demonstrates the manufactured housing is safer, more durable, and more energy saving than most believe – plus has strong consumer protections. Nonprofits, the federal government, and others with no direct ties to our industry have routinely come to surprisingly similar and positive conclusions.

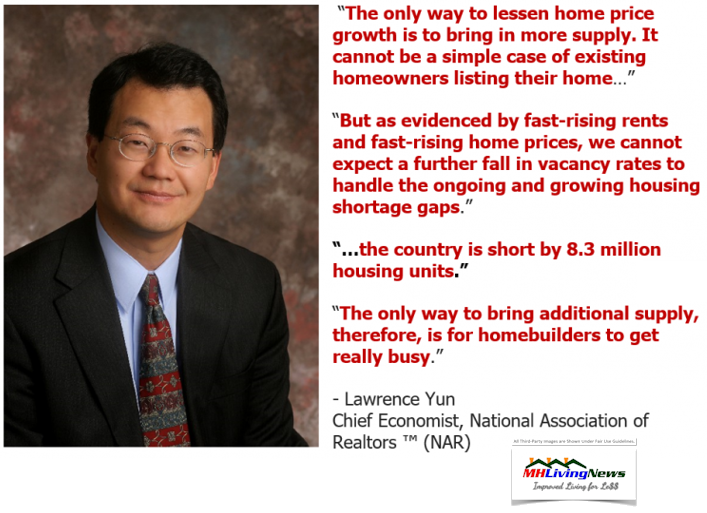

Let’s then note that the National Association of Realtors (NAR) Chief Economist Lawrence Yun, Ph.D., has said that the gap between housing needed and the housing being produced is in the millions of units.

Yun, as you see in the quotation above, also noted that builders have to get busy to close that gap. Only more construction will make more affordable housing available. Note that it was Yun, per Scholastica Cororaton to MHLivingNews, who asked her to study manufactured housing to see how it could be a solution for the affordable housing crisis. The logic behind that seems obvious. Conventional housing builders aren’t keeping up, and their prices are not as affordable as manufactured homes.

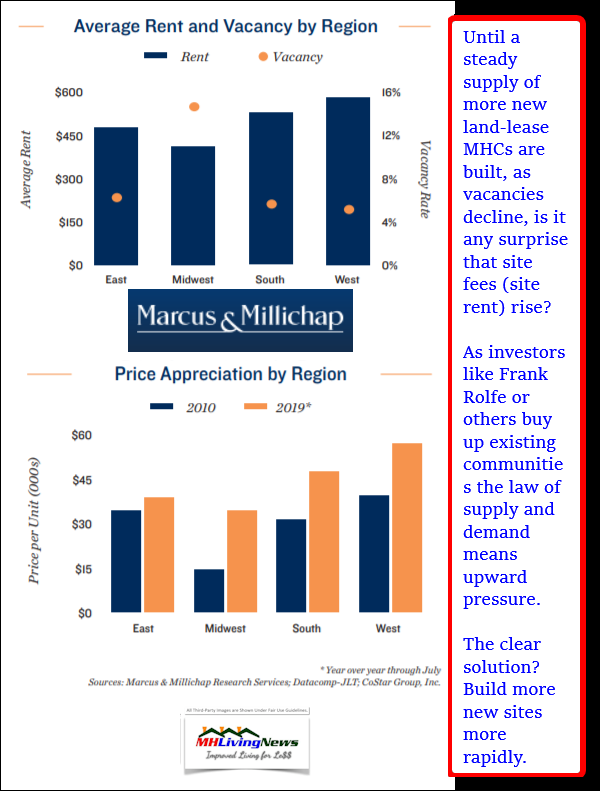

Only more supply will reduce the pressure on ever rising housing prices, per multiple sources as well as the logic of the law of supply and demand. Too few housing options in turn fuels higher rents too. That is true for conventional housing and manufactured homes sited in land-lease communities too. There is a need for more new manufactured home sites. The reverse of that factoid is this. Unless more sites are built, then inevitably as demand rises, site fees will rise. That understood, is it any surprise that people like Frank Rolfe are urging that no new communities be developed? If that became the rule, or if too few new sites are developed, it is inevitable that land-lease community rates will continue to be pushed up by those who are consolidating that part of the industry.

With that brief backdrop, let’s look at the first good law that makes manufactured housing a solution for potentially millions in the affordable housing crisis.

What are the Good Laws that Need to be Enforced?

This will be taken in three bite sized steps.

- What the law is regarding affordable manufactured homes and why Congress took the action that they did.

- What lending options Congress has provided for in order to make all housing, including manufactured homes, more accessible for lower to middle income buyers.

- Why smaller businesses can often prove to be better in manufactured housing. Yes, there are laws that protect that ideal, as will also be outlined further below.

The First Good Law That Already Exists…

The date was April 13, 2000, and the then pending legislation for the Manufactured Housing Improvement Act (MHIA) of 2000 included the following words. Keep in mind that prices and some data has changed but adjust for inflation and the principles still apply.

“Presently, over 19 million Americans live in approximately 9 million manufactured homes. According to the Department of Commerce, the average cost of a new manufactured home in 1998 was $43,800 (excluding land) compared with $136,425 (excluding land) for a new site-built home, thus extending home ownership to Americans who may otherwise be unable to purchase their own home. The median income for a manufactured homeowner was $24,500 in 1996 and according to Mr. Rutherford Brice, who testified on behalf of the American Association of Retired Persons (AARP), “44 percent of the manufactured home owners are aged 50 and above.”

“Presently, over 19 million Americans live in approximately 9 million manufactured homes. According to the Department of Commerce, the average cost of a new manufactured home in 1998 was $43,800 (excluding land) compared with $136,425 (excluding land) for a new site-built home, thus extending home ownership to Americans who may otherwise be unable to purchase their own home. The median income for a manufactured homeowner was $24,500 in 1996 and according to Mr. Rutherford Brice, who testified on behalf of the American Association of Retired Persons (AARP), “44 percent of the manufactured home owners are aged 50 and above.”

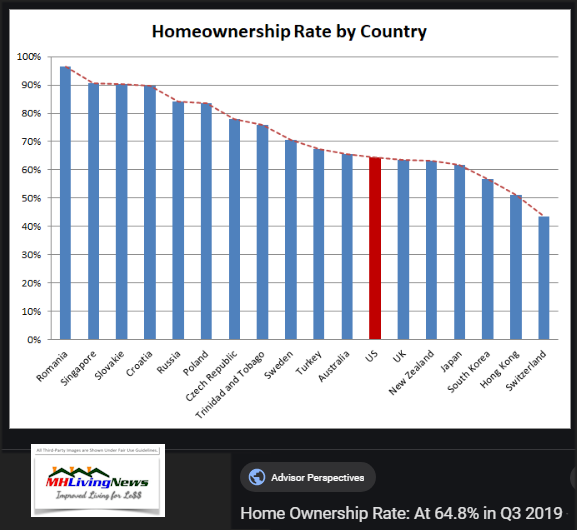

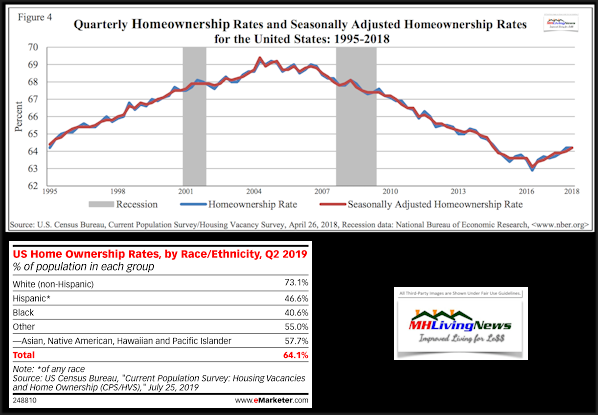

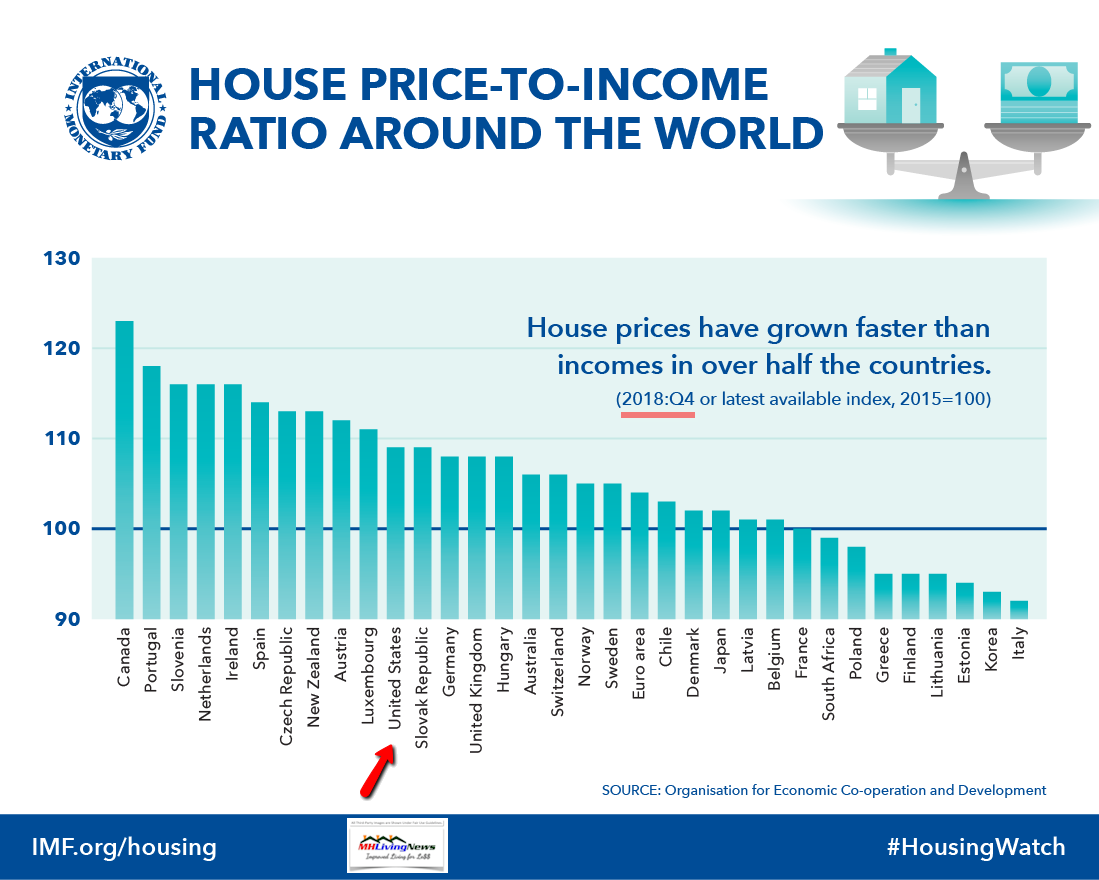

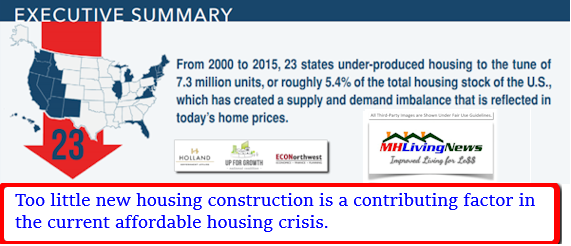

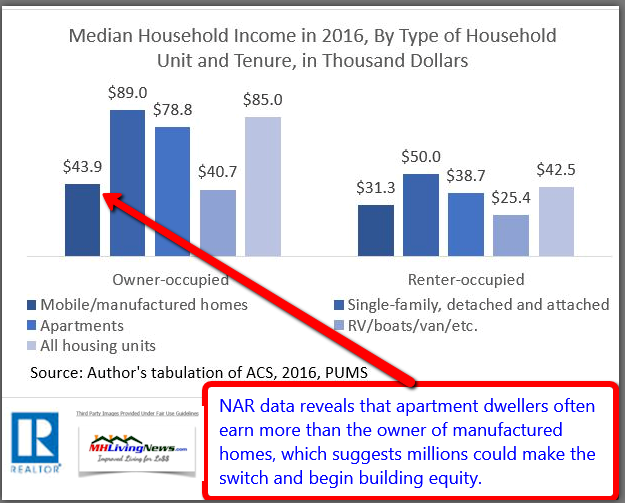

More recent data to round out that context is found in the infographic below.

That segue completed, let’s pivot back to the language from the then-pending MHIA 2000. This comes from a “R E P O R T OF THE COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS UNITED STATES SENATE to accompany S. 1452, ordered to be printed on April 13, 2000.” That report is linked here as a download.

That said in part as shown.

“PURPOSE AND SUMMARY OF NEED FOR LEGISLATION

The purpose of this legislation [the Manufactured Housing Improvement Act of 2000, or MHIA] is to set up a process to update manufactured housing safety and construction standards on a timely basis. The ’74 Act created the Federal manufactured housing program under the authority of the Department of Housing and Urban Development (HUD). Currently, the program is a division of the Office of Consumer and Regulatory Affairs and has no full-time director. The program’s staff has been reduced from 35 full-time employees in 1984 to eight professional employees today. Meanwhile, manufactured housing has become one of the fastest growing segments of the housing industry, growing by 100 percent over the last decade and now accounting for one in every four new single-family home starts.”

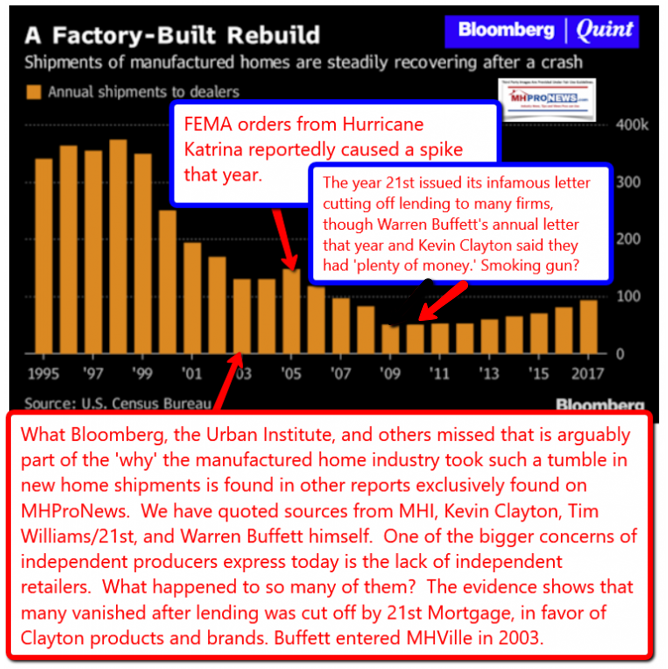

At the time that was written, the industry had roughly doubled in size in a decade, but it has since slid backward. We’ll look at that part of the narrative more later.

But that brief excerpt from the Senate sheds light that this law was designed approaching 2 decades ago to provide more affordable housing, as well as to provide more consumer protections. The Senate – after reports and expert testimony by consumer, industry, and other experts and advocates – passed a law that made more affordable housing possible.

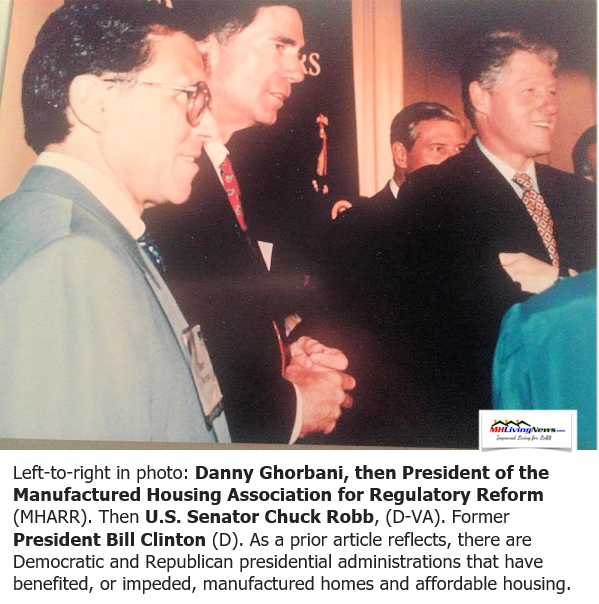

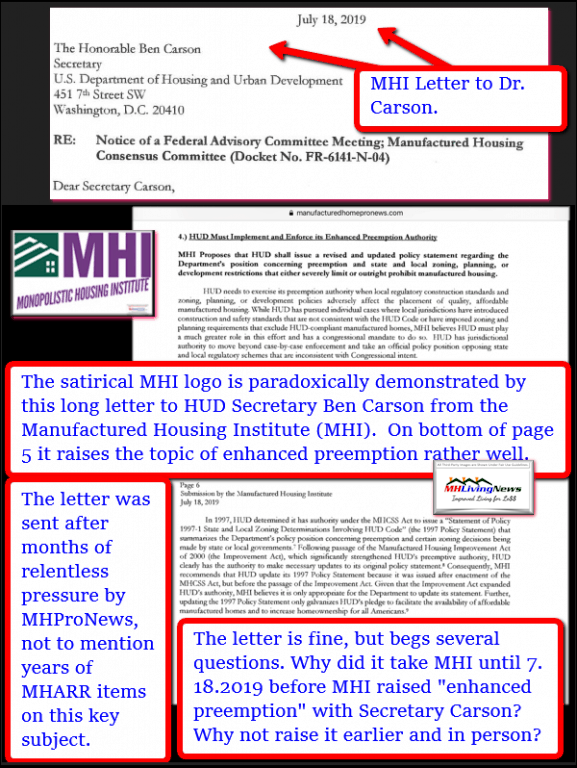

Mark Weiss, J.D., who is now president and CEO of the Manufactured Housing Association for Regulatory Reform (MHARR), was involved in the process of passing that law. At the time, it was Danny Ghorbani who headed up the organization, and his photo with then President Bill Clinton who signed the popular bi-partisan measure into law is as shown.

Weiss arguably understands the law far better than most because of his history, focus, legal background, and involvement. Here is what he said about the MHIA and why the enhanced preemption provision is important.

More on the MHIA and enhanced preemption later, but let’s pivot now to the second set of good laws.

The Second Set of Good Laws As Manufactured Home Living News has previously reported, there are several federal – and state – laws that provide good financing options for HUD Code manufactured homes. Some of those laws date back to the mobile home era, meaning they have existed for over 40 years. A partial list of the kinds of financing possible include the following.

· FHA Title I (home only, personal property loans – also known as ‘chattel loans.’) These can be used in many situations, including those where a manufactured home is going into an FHA accepted site where the land is being leased. That may include manufactured home communities. Check on current loan amounts and terms, but they may be as low as 5 percent down. Thus, on a $60,000 home, for a similar amount to a deposit and first months rental payment on a house, someone who qualifies could be buying a manufactured home.

· FHA Title II: these are loans that are ‘land home’ packages, which allow a borrower to finance a new HUD Code manufactured home with the appropriate utility, foundation, and other requirements met. Note that FHA Title I and Title II are usually made by approved lenders, and the federal government guarantees the lion-share of the loan in the case of default. A similar principle applies to some other federal loans. FHA Loans are loans can be as low as some 3.5 percent down. Land and home can be financed as a package.

· VA (Veterans Administration) loans are similar to FHA Title II, but can be as low as zero down. See a related report linked here.

· USDA or “Rural Development” loans. These have income and other requirements, as do the others that have federal guarantees, but must be in an area defined as ‘rural.’ American Financing says that at this time “Generally speaking, any rural community with a population below 35,000 is a sweet spot for finding a USDA loan eligible property.” USDA or Rural Development home loans can be as low as zero down payment.

· There are often first-time homebuyers and other state based programs, make sure you check that option out. Note that first time qualifications need not mean you’ve never owned a home previously, it is often defined to mean that you haven’t owned a home in the last few years. Again, check on the plan details with an approved lender or agency.

· Last point for now for manufactured housing lending is the law that we’ll spend more time on for this report. It was the “Duty to Serve” (DTS) provision of the Housing and Economic Recovery Act (HERA) of 2008. Over a decade has passed since HERA 2008 was passed into law and signed by then-president George W. Bush. Yet the Duty to Serve manufactured housing – which is a mandate for Fannie Mae, Freddie Mac – which are called “Government Sponsored Enterprises” (GSEs) and are supervised by the Federal Housing Finance Agency (FHFA) – is still barely enforced. More on that later below.

Third Types of Good Existing Laws

We periodically mention the importance of antitrust or ‘anti-monopoly’ laws on MHLivingNews, and even more so on our Manufactured Home Pro News (MHProNews) sister site. The reason is simple. Historically, monopolies were feared in America, and with good reason. From early in our nation’s founding, efforts to limit or outlaw monopolistic practices existed. The report below is one of several that goes into some detail, noting that it begins with a salute to veterans.

There are other laws that are also on the books that can protect consumers and smaller businesses. They include, but are not limited to:

· Laws prohibiting deceptive trade practices or misleading advertising.

· Laws that prohibit racketeering and other corrupt practices (RICO).

· Laws that prohibit a misuse of the U.S. Mail, as well as phones or internet (“the wires”).

But there are other laws, state and federal, that give consumer protections on a range of issues.

Why These Good Laws Matter?

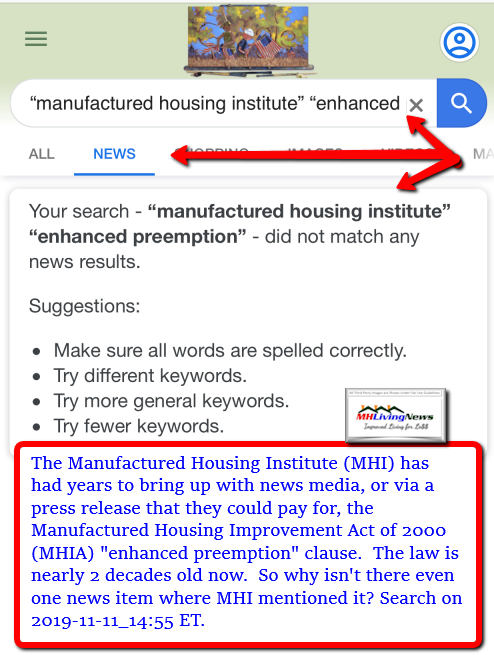

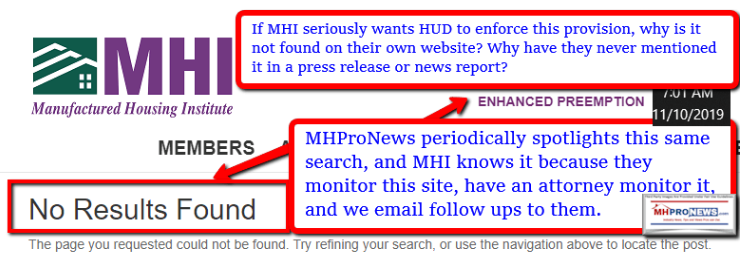

Wittingly or not, policy makers, advocates and others often talk about passing legislation to deal with current or emerging problems. But in many cases, the laws necessary already exist, as the outline above reflects. The Manufactured Housing Institute (MHI) claims to advocate for all aspects of manufactured homes and factory-built housing. If so, then one would think that they would be actively advocating for the enforcement of these good existing laws, right? But as reports linked herein and some sample screen captures of Google searches done today reflect, MHI purportedly postures things to their members, when what they claim may be almost invisible online.

Which begs the question. If they are serious about advocating for good existing laws, as MHARR is, then why are MHI’s efforts so invisible?

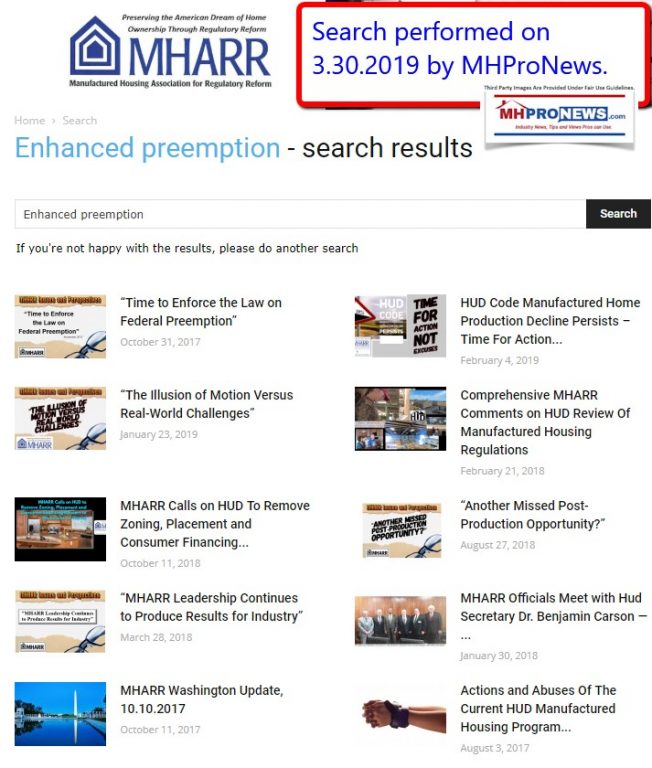

To clarify the point, some Google and website searches will make the point. MHARR’s website has many articles that deal with the Manufactured Housing Improvement Act of 2000 (MHIA) and specifically the topic of enhanced preemption. See the first screen capture above. By contrast, MHI’s own website has no results for a similar search on the date shown.

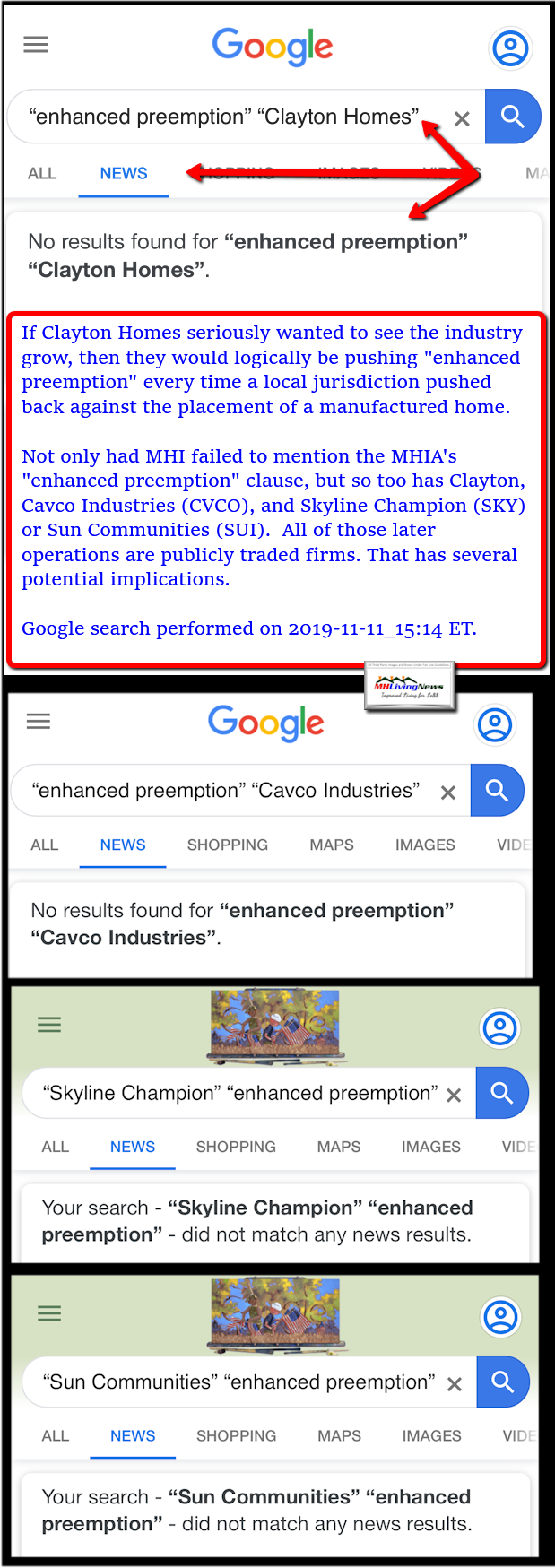

But it isn’t only MHI, some of their larger members are also mum on the topic of enhanced federal preemption.

There are several reasons why this matters, but a pair of dramatic examples are the kinds of reports spotlighted above and below.

MHLivingNews could make similar points with other negative mainstream media news about other firms that are MHI members or are otherwise connected to them. But that is enough to make this point. While they have sent HUD Secretary Carson a letter that asks him to enforce this federal law, and the letter is overall okay, where is the backup action to support that letter?

Why – if MHI and their larger members are serious about making more affordable housing available – oh why is it so difficult to find evidence online of something that MHI, Clayton Homes, Cavco Industries, Skyline Champion, or Sun Communities have said that even mentions enhanced federal preemption? The logical answers are found in reports with analysis like the next two.

By limiting growth, there are several indirect benefits for certain ‘big boy’ members. Nor is it purely speculative, because now exiting MHI President Richard ‘Dick’ Jennison said on camera that the industry should be thinking about slow growth.

That isn’t an odd comment by Jennison, that’s nuts during an affordable housing crisis when one thinks about Dr. Yun’s comments above.

That and the article linked below and further down following the byline and notices are enough to make these points.

There is an apparent charade underway that MHARR has called the “Illusion of Motion.” MHI and certain major firms posture to their members and stockholders support of these good laws. But when closely examined, there is little backup evidence, as the Google searches above reflect. Why does that matter?

Because what is arguably at play is a slow-motion monopolization of the marketplace. Monopolization is occurring in part by NOT enforcing good laws. There are also reason to believe that some federal officials, as well as those in the GSEs, are colluding with MHI and/or larger companies to limit, re-direct, or otherwise ‘hide’ the benefits of these good laws. That concern is the subject of other reports linked from this one.

Smaller firms often pay better attention to their customers, and won’t do the kinds of problematic behaviors that larger firms – which are ironically often MHI connected – engage in.

By kicking up bad news about manufactured housing, they also make it more difficult for smaller firms to succeed. Thus, despite those years of solid, positive research linked further above, Zillow’s research reveals that interest in manufactured housing declined during the two years of the research shown.

Those headwinds should not exist if MHI was truly trying to promote the industry’s growth. Either MHI and these larger firms are massively incompetent, or they are arguably executing a plan that has several reasons to believe violate one or more federal laws, all to the harm of smaller businesses, some shareholders, and also manufactured home owners and possible affordable housing consumers.

Summing Up

Good existing laws are already on the books that could benefit smaller manufactured home industry companies, residents of manufactured home communities facing stiff site fee increases, and those renters that would desire and benefit from home ownership. More homeownership could benefit millions.

There are lots of proposals by perhaps well indented people, but at the end of the day, enforcing good existing laws is the fastest surest path to more lower and middle class wealth, and lower housing costs too. See the related reports above and below, that come to similar conclusions.

Some create a costume or illusion of respectability. Examples are found linked from this report, dig deeper into those or others found here by the hundreds to learn more. Thanks for making our sister site and this the manufactured housing industry’s largest and runaway most-read combination of sources for manufactured home news, fact-checks and analysis where “We Provide, You Decide.” © (Manufactured homes, lifestyle news, reports, fact-checks, analysis, and commentary. Third-party images or content are provided under fair use guidelines for media.)

(See Related Reports, further below. Text/image boxes often are hot-linked to other reports that can be access by clicking on them.)

By L.A. “Tony” Kovach – for MHLivingNews.com.

Tony earned a journalism scholarship and earned numerous awards in history and in manufactured housing. For example, he earned the prestigious Lottinville Award in history from the University of Oklahoma, where he studied history and business management. He’s a managing member and co-founder of LifeStyle Factory Homes, LLC, the parent company to MHProNews, and MHLivingNews.com. This article reflects the LLC’s and/or the writer’s position, and may or may not reflect the views of sponsors or supporters.

Connect on LinkedIn: http://www.linkedin.com/in/latonykovach

Related References:

The text/image boxes below are linked to other reports, which can be accessed by clicking on them.

\